Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition] - CPA Pilot

Multistate Tax Planning

Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]

CPA Pilot

May 11, 2026·17 min read

Have you ever thought why the Washington B&O tax requires a different CPA review approach?

Washington B&O tax requires a different CPA review process because it is imposed on gross income from business activity, not on the net income. A client can have low margins, high operating costs, or even a weak profit year and still owe B&O tax if Washington taxable gross receipts exist.

TL;DR – Washington B&O Tax 2026

Washington B&O Tax Overview:

Based on gross receipts, not net income.

CPAs should review revenue streams, apply classifications, and ensure proper sourcing.

Economic nexus triggers filing requirements for out-of-state businesses with over $100K in receipts.

2026 B&O Tax Rates:

Retailing: 0.471%, increasing to 0.5% in 2027.

Wholesaling & Manufacturing: 0.484%, increasing to 0.5% in 2027.

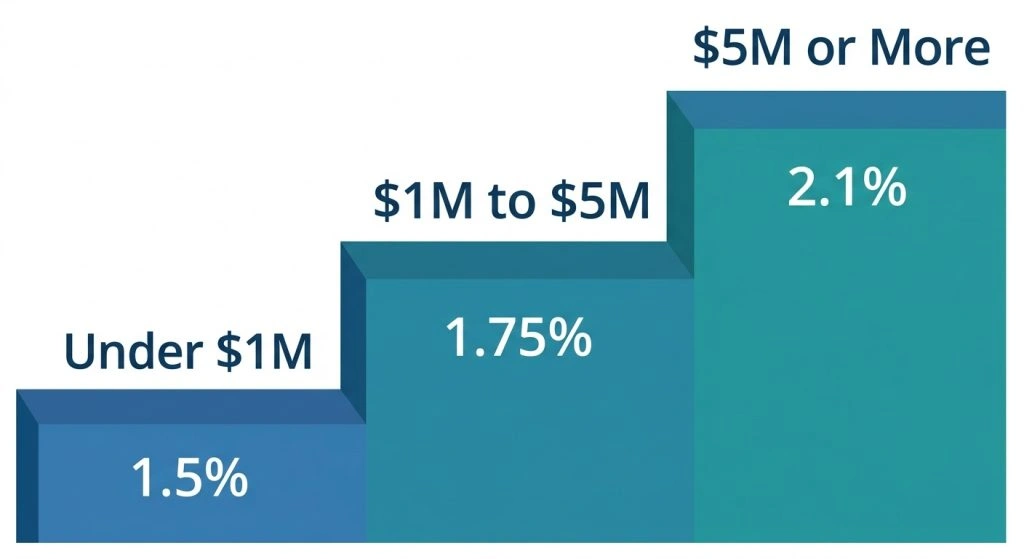

Service: 1.5% under $1M, 1.75% for $1M-$5M, 2.1% over $5M.

Real estate commissions: 1.5%, effective 2025.

B&O Surcharge:

A 0.5% surcharge applies to businesses with taxable income of $250M+.

Exemptions for financial institutions, certain manufacturing, and timber-related income.

Small Business B&O Credit:

Reduces B&O tax liability for eligible small businesses.

Review required for correct classification and filing frequency.

Filing Frequency & Deadlines:

Monthly, quarterly, or annual filing depending on business receipts.

Check for local tax obligations, especially in cities like Seattle.

CPA Review Checklist:

Identify receipts, apply correct classifications, and check for applicable credits and exemptions.

Ensure proper sourcing and local tax review.

This changes the starting point for the review. For federal income tax, the CPA usually looks at income after deductions, entity treatment, and taxable income. For Washington B&O, the first question is different: what activity generated the receipt, where is it sourced, and which classification applies?

For CPA files, the review should answer:

What revenue streams does the client have?

Which Washington B&O classification applies to each activity?

Did the client exceed Washington’s economic nexus threshold?

Does the client qualify for the small business B&O credit?

Is more than one taxable activity being performed on the same product?

Does the client have separate city B&O or local business tax obligations?

Is the service-rate tier affected by affiliated-group gross income?

This is also why Washington B&O can catch out-of-state clients off guard. Physical presence is not always required, and gross receipts can create filing exposure.

For a broader context on how state-level tax rules can differ from federal tax assumptions, check out our guide on federal vs state tax differences.

How Washington B&O Tax Operates as a Gross Receipts Tax

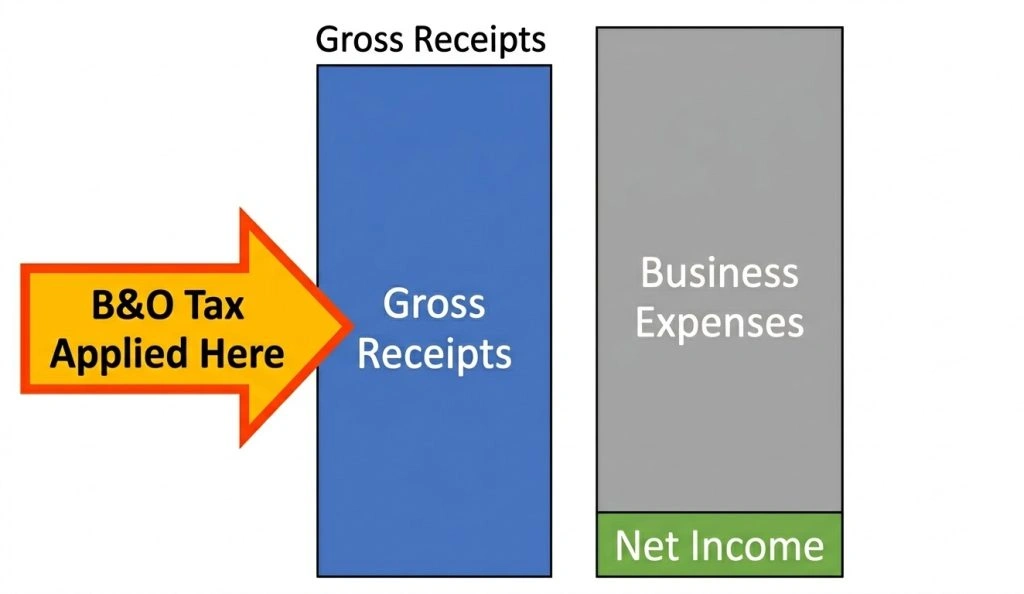

Unlike federal income tax, Washington B&O tax is applied to the gross revenue line, not the profit remaining after expenses.

Washington generally relies on the B&O tax rather than a broad-based corporate income tax. Instead, the B&O tax applies to business activity and is measured by gross receipts, gross income, or the value of products, depending on the classification. DOR describes the state B&O tax as a gross receipts tax measured on the value of products, gross proceeds of sale, or gross income of the business.

That means normal business expenses do not reduce the B&O base. Payroll, rent, materials, subcontractor costs, software subscriptions, insurance, and other operating expenses may matter elsewhere in the client’s tax file. Still, they do not reduce Washington B&O in the same way income-tax deductions reduce federal taxable income.

Example: A professional services firm has $900,000 in gross receipts sourced to or attributed to Washington and $760,000 in expenses. The B&O review does not start with the $140,000 net result. It starts with the $900,000 of gross receipts and then asks which classification and sourcing rules apply.

For CPAs, this creates a recurring review pattern:

Washington B&O rates depend on the activity classification, not simply on the client’s entity type. An LLC, S corporation, C corporation, partnership, or sole proprietorship can face the same B&O classification if the same business activity is performed.

The Service and Other Activities rate increases as business or affiliated group income crosses specific thresholds.

For CPA review, the classification table should be treated as a starting point.

B&O Classification

Current Rate

CPA Review Note

Retailing

0.471%

Review whether receipts involve retail sales or retail services; scheduled to increase to 0.5% on January 1, 2027. (Source)

Wholesaling

0.484%

Confirm resale documentation and wholesale treatment; scheduled to increase to 0.5% on January 1, 2027.(Source)

Manufacturing

0.484%

Review MATC, where products are also sold; scheduled to increase to 0.5% on January 1, 2027.(Source)

Service and Other Activities

1.5% under $1 million; 1.75% from $1 million to $4,999,999.99; 2.1% at $5 million or more

Tier is based on the affiliated group’s prior calendar year taxable income from this classification.(Source)

Real Estate Commissions

1.5%

Commissions from real estate sales are no longer reported under Service and Other Activities starting in 2025. Non-commission income from real estate firms, such as property management or desk fees, may still fall under Service and Other Activities.(Source).

Payment card processing

3.1%

New classification; effective January 1, 2026.(Source)

The Washington DOR’s Service and Other Activities rate notice states that, effective October 1, 2025, the classification uses rates of 1.5%, 1.75%, and 2.1% based on prior calendar year taxable income under the affiliated-group framework. The same notice lists exceptions for hospitals and select advanced computing businesses that continue to use the 1.5% rate. (Source)

The current DOR service-rate structure uses three tiers, and the rate determination may depend on the affiliated group’s gross income from the Service and Other Activities classification under the Washington law change. Because of that, CPAs should avoid reviewing a service entity in isolation when related or affiliated service businesses may affect the applicable tier.grantthornton+1

The gap between classifications is material. Service income may face a higher rate than retailing, wholesaling, or manufacturing income, so a mixed-activity client should not default all receipts into Service and Other Activities without support.

A Clean CPA Workpaper should show:

Classification selected

Revenue assigned to each classification

Rate applied

Source used for classification support

Affiliated-group review, where applicable

Exception review, if applicable

Reviewer note for mixed-activity clients

How Does the Service and Other Activities Tier Change Affect CPA Workpapers?

CPAs should document the basis for the service-rate tier chosen and retain support for the prior-year facts used in the review. The workpaper should show the applicable tier, any affiliated-group consideration, and the source relied on for the conclusion.

A practical workpaper should include:

Prior calendar year taxable income from the Service and Other Activities classification.

Affiliated-group considerations, where applicable.

Applicable rate tier.

Whether any DOR-listed exception applies.

Source citation used for the rate conclusion.

Example: A consulting firm with $6.2 million in current-year Washington service receipts should not automatically apply a rate based only on its standalone current-year receipts. The CPA should review the prior calendar year taxable income from the Service and Other Activities classification and determine whether affiliated-group facts affect the rate tier.

Washington B&O Surcharge for High-Grossing Businesses

Beginning January 1, 2026, Washington imposes a 0.5% surcharge on certain businesses with Washington taxable income of $250 million or more.

The surcharge applies to taxable income above the threshold. Current SB 6346 materials indicate the surcharge is now set to expire on January 1, 2028, and the bill contains a potential legal challenge risk that could affect related provisions. (Source)

The DOR-level exemptions and exclusions are specific, so CPAs should not rely on a simplified paraphrase. The surcharge does not apply to income already subject to the financial institution surcharge, income already subject to the advanced computing surcharge, income taxed under the manufacturing B&O classification, including wholesale and retail sales of manufactured goods, retail sales of exempt food and food ingredients, retail sales of prescription drugs, or income subject to preferential timber or wood product tax treatment.

For CPA review, the key questions are:

Does the client have Washington taxable income of $250 million or more?

Does any income fall into an exempt or excluded category?

Is the surcharge calculation based only on income above the threshold?

Does the client already face another surcharge regime that removes the amount from this calculation?

This issue should be reviewed separately from the standard B&O rate table because it affects only very large taxpayers and can materially change the Washington tax profile for 2026 through 2028. (Source)

How does the Washington Small Business B&O Credit Work?

The Washington small business B&O credit can reduce B&O tax for taxpayers with lower B&O liability, but it should not be treated as a simple flat annual cap. The Department of Revenue provides Small Business Credit tables by reporting period, including monthly, quarterly, and annual tables. (Source)

DOR also states that the credit varies depending on the total amount of B&O tax due for all classifications after the business takes other available B&O tax credits.

For CPA review, the question is not just whether the client is small. The preparer should check the client’s assigned reporting frequency, total B&O tax after other credits, activity mix, and the applicable DOR credit table.

Review points:

Is the taxpayer a monthly, quarterly, or annual filer?

Which DOR small business credit table applies?

What is the B&O tax due before the credit?

Are other B&O credits applied first?

Does the classification mix affect the credit calculation?

Is the credit calculated correctly through My DOR?

The credit can materially reduce tax due for low-liability taxpayers, but it does not correct a wrong classification, missed nexus, unsupported sourcing, or a local filing issue.

Washington B&O Filing Deadlines and Frequency Overview

Washington B&O tax is reported through the state excise tax return system. Filing frequency may be monthly, quarterly, or annual, depending on the taxpayer’s assigned status and expected tax liability.

The Washington DOR lists the general due dates clearly:

Filing Frequency

General Due Date

CPA Review Point

Monthly

25th day of the following month

Watch growing clients and businesses with changing liability

Quarterly

End of the month after quarter-end

Do not use the monthly due-date rule for quarterly filers

Annual

April 15

Confirm the correct annual due date in the client file

A client’s filing frequency can change as revenue grows or tax liability changes. CPAs should save DOR filing-frequency notices in the client file and review them when a business grows from lower receipts to higher Washington activity.

Economic Nexus Rules for Out-of-State Businesses under Washington B&O Tax

Out-of-state businesses trigger a filing requirement once Washington-sourced gross receipts exceed the economic threshold.

Out-of-state businesses can have Washington B&O filing exposure even without an office, warehouse, employee, or physical location in the state.

Washington DOR states that, starting January 1, 2020, a business must register to report B&O tax and collect or submit applicable sales tax if it has physical presence nexus, more than $100,000 in combined gross receipts sourced or attributed to Washington, or is organized or commercially domiciled in Washington. (Source)

The Impact of Apportionment on Washington B&O Tax Liability

Washington service receipts may need to be sourced or apportioned based on where the customer receives the benefit of the service, not simply where the work is performed. CPAs should focus on whether the activity is apportionable, how receipts are sourced under the applicable Washington rule, and whether the records support the method used.

A review file should identify:

Customer location.

Where the customer receives the benefit of the service.

Gross receipts sourced or attributed to Washington.

Non-Washington receipts.

Classification tied to each receipt stream.

Method used to support the sourcing position.

Records supporting the allocation.

This can prevent overpayment. A national service provider may have a Washington nexus but still needs to source only the Washington portion of apportionable receipts to Washington.

Avoid framing apportionment as a loophole. It is a documentation issue, and the CPA needs support for the sourcing position used on the return.

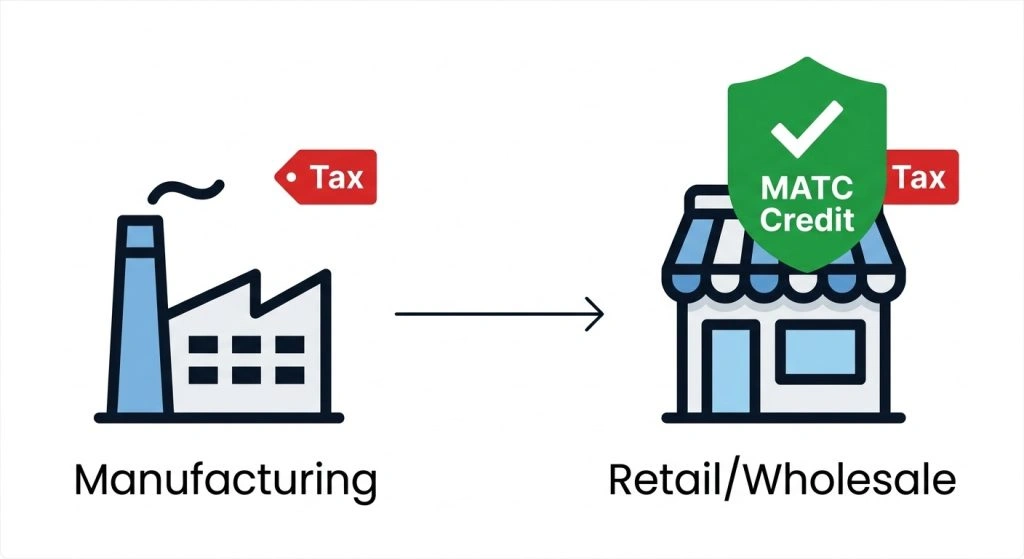

How the Multiple Activities Tax Credit Helps Prevent Double Taxation

The Multiple Activities Tax Credit (MATC) ensures that businesses are not taxed twice on the same product across different activities.

The Multiple Activities Tax Credit, or MATC, can apply when a business performs more than one taxable activity on the same product. Washington DOR explains that when a business performs more than one taxable activity for the same product, it may take an MATC so that tax is not paid twice on the same amount.

This is not limited to one simple manufacturing-and-wholesale fact pattern. The broader principle is that two or more taxable activities may exist for the same product, and the credit may prevent double taxation when the requirements are met.

CPA review should check:

Is the same product involved?

Whether two or more taxable activities were reported?

Which classifications apply?

The taxable amount under each classification.

The tax is computed under each activity.

The credit calculation.

Whether Schedule C support is included?

Do the records support the claim?

The safer filing approach is usually to report the activities correctly and claim the MATC where allowed, rather than omitting a taxable activity from the return.

Key Review Points for CPAs in Washington B&O Tax Filing

Washington B&O review should be handled as a workflow, not a one-line rate lookup. The strongest review files usually separate receipts, classifications, sourcing, credits, affiliated-group considerations, and local obligations before the return is finalized.

1. Classification Split

Mixed-activity clients should be reviewed by revenue stream. Service, retailing, wholesaling, manufacturing, real estate commissions, software, digital products, licensing, repairs, installation, and professional services may require separate treatment.

The main risk is placing too much revenue into Service and Other Activities without reviewing whether another classification applies to part of the activity.

2. Service-Tier Review

For Service and Other Activities, check the prior calendar year taxable income from the Service and Other Activities classification. Consider affiliated-group gross income where applicable. Do not apply a current-year rate without documenting the basis for the tier.

The review should also note whether any DOR-listed exception applies.

3. Washington Gross Receipts Review

Out-of-state clients should be reviewed for gross receipts sourced or attributed to Washington. The $100,000 threshold can create registration and filing exposure even without physical presence.

4. Small Business Credit

The small business credit should be reviewed using the applicable DOR table for the client’s reporting frequency. Avoid estimating the credit from a simple annual cap unless the specific table supports the calculation.

5. MATC

If the client performs multiple taxable activities on the same product, review MATC eligibility and Schedule C Support.

6. Local Business Tax

Check Seattle separately and review other cities based on the client’s activity. Do not assume state registration covers local obligations.

Common Washington B&O Classification Mistakes to Avoid

Washington B&O mistakes often happen because the preparer treats B&O as one tax line instead of an activity-based classification system.

Mistake #1: Reporting All Revenue Under Service and Other Activities

Service and Other Activities can become the default classification when a client has mixed receipts. That can create overpayment if some revenue belongs under retailing, wholesaling, manufacturing, real estate commissions, or another classification.

Mistake #2: Applying the Old Flat Service Rate

Service-rate review changed after October 1, 2025. CPAs should check prior calendar year taxable income from the Service and Other Activities classification and consider affiliated-group facts where applicable before applying the current rate.grantthornton+1

Mistake #3: Missing Washington Nexus for Remote Clients

Out-of-state businesses can trigger B&O filing obligations if they exceed $100,000 in combined gross receipts sourced or attributed to Washington.

Mistake #4: Treating State Filing as Local Filing

Washington state B&O and Seattle B&O are separate. Seattle’s 2026 rules should be reviewed independently from the state return.

Mistake #5: Missing MATC Support

If a taxpayer performs more than one taxable activity on the same product, MATC may apply, but the credit should be documented. DOR lists MATC as one of the major B&O credits and describes credits as amounts subtracted from B&O tax due on the excise tax return.

A client with multistate service receipts may need sourcing and receipts-factor support. The review should not assume every receipt is assigned to Washington without checking the activity, customer location, and supporting records.

Comprehensive Washington B&O Tax Review Checklist for CPAs

Use this checklist before filing or advising a Washington client.

Client Activity Review

Identify each revenue stream.

Separate service, retailing, wholesaling, manufacturing, real estate commissions,

software, digital product, and other activity revenue.

Confirm whether any revenue was placed into Service and Other Activities by default.

Rate Review

Confirm the current classification.

Review prior calendar year taxable income from the Service and Other Activities classification.

Consider affiliated-group gross income where applicable.

Confirm the correct service-rate tier.

Review whether any DOR-listed exception applies.

Nexus Review

Calculate gross receipts sourced to or attributed to Washington.

Check whether the client crossed $100,000 in the current or prior year.

Review physical presence, commercial domicile, or organization in Washington.

Credit Review

Check small business credit eligibility using the correct DOR table.

Review MATC where two or more taxable activities apply to the same product.

Confirm Schedule C support where MATC is claimed.

Local Review

Check Seattle separately.

Review other city or local business tax obligations based on client facts.

Confirm whether a local business license is required.

Documentation Review

Save DOR source links.

Keep classification support.

Document sourcing and apportionment method.

Keep revenue schedules by state and activity.

Record CPA judgment on uncertain classification issues.

How CPA Pilot Supports Washington B&O Tax Research

CPA Pilot helps CPAs research, organize, and document state tax issues faster. For firms handling Washington B&O tax planning, CPAs can use CPA Pilot as a research and review layer for classification questions, service-rate checks, affiliated-group considerations, nexus triggers, credit review, and client-facing explanations.

CPA Pilot can help tax teams:

Summarize Washington DOR guidance

Compare B&O classifications

Draft issue-specific research notes

Identify client follow-up questions

Organize support for the Nexus review

Prepare plain-English client summaries

Document where human CPA judgment is still required

Don’t waste your time anymore… Book a CPA Pilot demo today and see the difference!!!

CPA Pilot does not replace the CPA’s decision-making. The CPA still decides whether the classification is supportable, whether apportionment is reasonable, whether MATC applies, whether affiliated-group rules affect the service tier, and whether a local filing obligation exists.

FAQs About Washington B&O Tax for CPAs

How does Washington B&O tax apply to online sales and e-commerce businesses?

Washington B&O tax applies to online sales if your business has economic nexus, meaning over $100,000 in gross receipts sourced to Washington. Even without a physical presence, e-commerce businesses must register, file returns, and potentially collect sales tax.

What are the specific B&O tax rates for service-based businesses in Washington?

Service businesses in Washington B&O tax are subject to rates based on annual gross income. For businesses with income under $1 million, the rate is 1.5%. It increases to 1.75% for income between $1 million to $5 million and 2.1% for over $5 million.

How does Washington’s B&O tax impact small businesses and startups?

Washington offers a small business B&O credit to businesses with taxable income under a certain threshold. It reduces tax liability, but the credit depends on revenue, the reporting frequency, and eligibility. Businesses under $100,000 in receipts may be exempt from filing.

Can Washington B&O tax affect my business if I operate as an LLC or S-corp?

Yes, Washington B&O tax affects LLCs and S-corps, as it applies to gross receipts, not net income. The tax rate depends on the business activity (e.g., retail, wholesale, service), and both LLCs and S-corps must file returns, regardless of profitability.

What is Washington’s economic nexus rule for out-of-state businesses?

Washington’s economic nexus rule mandates out-of-state businesses with over $100,000 in gross receipts sourced to Washington to register for B&O tax. Physical presence isn’t required—businesses must comply if they meet the revenue threshold, even without a local office.

Disclaimer: This article is provided by CPA Pilot for educational purposes. While we may offer tax software/services, the information here is general and may not address your specific facts and circumstances. It does not constitute individual tax, legal, or accounting advice. U.S. federal and State Tax laws change frequently; please consult a qualified tax professional before acting on any information.

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.