How to Review Form 1065 for Schedule K-1, Capital & Basis Errors - CPA Pilot

Federal Tax Automation

How to Review Form 1065 for Schedule K-1, Capital & Basis Errors

CPA Pilot

May 8, 2026·16 min read

Form 1065 review is no longer just about preparing a partnership return. For CPA firms, the real risk is whether the Form 1065, Schedule K‑1 package, partner capital accounts, allocation schedules, basis adjustments, and reconciliation schedules all tie before filing.

TL;DR – Form 1065 Review & Errors

Review Form 1065 before filing by checking Schedule K-1s, partner capital accounts, allocations, basis adjustments, and partner-level disclosures.

Confirm the return’s filing status, Form 7004 extension status, Schedule K-1 delivery, and late-filing penalty exposure before deeper technical review.

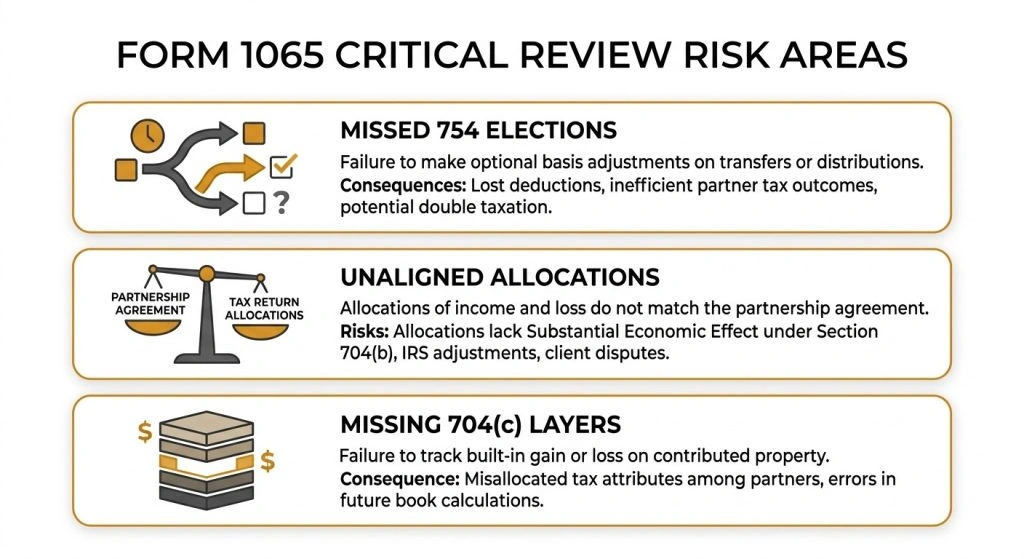

Check Schedule K-1s against the partnership agreement, ownership changes, special allocations, guaranteed payments, distributions, Box 14, Box 20, and Box L.

Review §704(b) capital accounts to confirm that special allocations have economic effect and match the partnership agreement.

Flag §704(c) issues when contributed or revalued property has book-tax differences that must stay with the contributing partner.

Review §754 election status when a partner interest transfer, partner death, or property distribution may trigger §743(b) or §734(b) basis adjustments.

Separate tax-basis capital from outside basis because Schedule K-1 Box L does not include every partner-level basis item.

Reconcile Schedule L, M-1, M-2, and M-3 to confirm that book income, taxable income, capital accounts, and K-1 totals tie.

Check foreign partner withholding under §1446 when the partnership has foreign partners or effectively connected taxable income.

Use a repeatable Form 1065 review checklist so CPA firms can catch K-1, capital, basis, election, and disclosure errors before filing.

Partnership return review is not a niche workflow.

According to the latest available IRS Statistics of Income partnership data, partnerships filed over 4.5 million returns and represented more than 30.2 million partners for tax year 2023. Limited liability companies (LLCs) made up most partnership returns, with IRS and practitioner summaries noting that roughly 72.7% of partnership returns for recent years were filed by LLCs. This reinforces why Form 1065 review remains a recurring workload for CPA firms.

This guide gives CPAs a practical review sequence for checking Schedule K‑1, §704(b) capital accounts, §754 elections, §743(b)/§734(b) basis adjustments, tax‑basis capital reporting, and partner‑level disclosures before final manager or partner sign‑off.

For a broader context on how partnership and LLC income passes through to owners, see CPA Pilot’s guide to pass‑through entity tax rules.

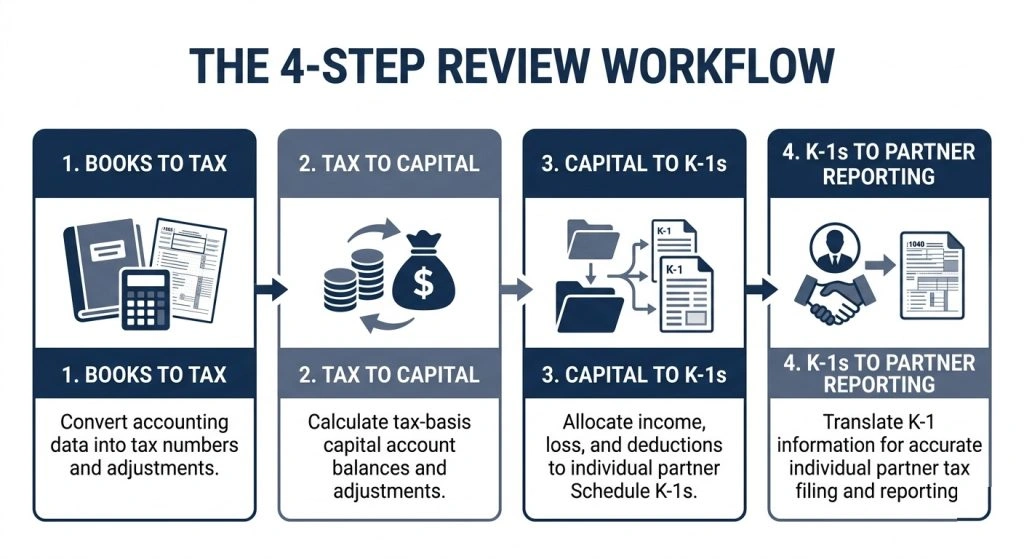

Why CPAs Need a Structured Form 1065 Review Workflow?

Form 1065 turns partnership‑level data into partner‑level tax consequences. Tax software may complete the return fields, but the reviewer must confirm that the partnership agreement, books, tax adjustments, and partner disclosures support the filing position.

A structured sequence ensures that partnership-level data correctly informs partner-level tax consequences.

A structured workflow helps CPA firms move from general return preparation to issue‑based review. Instead of checking numbers in isolation, the reviewer tests whether each schedule supports the next one:

Books to tax

Tax to capital

Capital to K‑1s

K‑1s to partner‑level reporting

This matters because a partnership return can be technically filed while still missing the context needed to support allocations, elections, basis adjustments, or partner‑specific disclosures.

That workflow begins with the simplest question: Is the return being reviewed against the correct filing deadline and extension status?

Form 1065 Deadlines CPAs Should Verify for 2026

Calendar‑year partnerships filing 2025 returns have an original Form 1065 due date of March 16, 2026, because the usual March 15 deadline falls on a Sunday.manaycpa+1

Since that deadline has passed, CPAs should now confirm whether the partnership filed on time, submitted a valid Form 7004 extension, furnished Schedule K‑1s to partners, and documented any late‑filing or penalty exposure before continuing the review.

Key 2025 Tax-Year Form 1065 Dates for Calendar-Year Partnerships

Review item

2025 Tax Year Status (Calendar‑Year)

Original Form 1065 due date

March 16, 2026 (March 15 falls on Sunday)

Form 7004 extension request due

March 16, 2026 (original due date)

Extended Form 1065 due date

September 15, 2026

Schedule K‑1 delivery to partners

Generally, by the return due date, including a valid extension

Fiscal‑year partnership deadline

15th day of the 3rd month after year‑end

An extension gives the partnership more time to file the return. It does not remove the need to review partner‑level tax effects, withholding obligations, estimated tax exposure, or K‑1 timing issues.

Once the filing or extension status is confirmed, the next step is reviewing penalty exposure so the firm can document issues before they affect the partner‑level reporting workflow.

Form 1065 Penalties CPA Firms Should Check Before Filing

Late or incomplete partnership returns can create penalty exposure. The current Form 1065 instructions should always be checked before filing because penalty amounts and filing details can change by tax year.

The key review point is not only whether the return was filed. CPAs should also confirm whether all required partner statements, K‑1s, capital account details, and disclosure schedules were furnished correctly.

A penalty review should include:

Whether Form 1065 was filed by the original or extended due date

Whether all Schedules K‑1 were issued on time

Whether information‑return penalties may apply to incomplete or incorrect partner statements

Whether the firm has reasonable cause documentation if a late filing issue exists

Whether Rev. Proc. 84‑35 or other relief may apply for a qualifying small partnership (where applicable under current IRS guidance)

Do not rely on penalty relief as a workflow substitute. The cleaner process is to calendar the return, complete the K‑1 review early, and preserve documentation before filing.

After deadline and penalty exposure are reviewed, the return should move into the K‑1 package because partner‑level reporting depends on it.

Schedule K-1 Review Checklist for CPAs Before Filing

Schedule K‑1 converts partnership‑level tax items into partner‑level reporting. The review should confirm that each partner’s K‑1 reflects the:

Partnership agreement

Ownership changes

Special allocations

Partner‑specific items

CPAs should also use the 2025 Partner’s Instructions for Schedule K‑1 to confirm how income, deductions, credits, capital details, and partner‑level disclosures are reported and interpreted.

Schedule K-1 Review Focus Areas

Schedule K‑1 area

CPA review focus

Box 1 ordinary business income/loss

Confirm allocation matches ownership and special allocation rules.

Boxes 2–3 rental income

Check whether rental activity is separated from business income.

Box 4 guaranteed payments

Confirm whether payments are for services or capital.

Box 14 self‑employment income

Review partner type and participation level.

Box 19 distributions

Tie distributions to capital and basis tracking.

Box 20 other information

Confirm required partner‑level disclosures.

Box L capital account

Confirm tax‑basis capital reporting and reconciliation.

Box 20 should be reviewed for partner‑level disclosures, but detailed QBI mechanics belong in CPA Pilot’s QBI deduction CPA guide rather than this Form 1065 workflow article.

Once the K‑1 package is mapped, the reviewer should test whether the allocations behind those K‑1 items are supported by the partnership agreement and capital records.

How CPAs Review §704(b) Capital Accounts

CPAs should review §704(b) capital accounts because special allocations must have economic substance, not just tax effect. The purpose of this review is to confirm whether the partnership agreement, capital accounts, and liquidation provisions support the allocation pattern being reported.

A practical §704(b) review should ask:

Are capital accounts maintained under the partnership agreement?

Do contributions, distributions, income, losses, and revaluations flow through capital properly?

Are liquidating distributions tied to positive capital account balances?

Does the agreement include a deficit restoration obligation or a qualified income offset where needed?

Are special allocations supported by economic effect or partner interest in the partnership?

The review goal is not to restate every §704(b) rule. It is to identify whether the return position depends on allocations that are not supported by the agreement or capital records.

When CPAs Should Flag §704(c) Built-In Gain or Loss Issues

CPAs should flag §704(c) issues when property was contributed with a fair market value that differed from its tax basis. That difference can create builtin gain or built‑in loss that must be tracked so pre‑contribution tax consequences stay with the contributing partner.

Reviewers should look for:

Contributed property with a book‑tax difference

Depreciation differences between book and tax records

Revaluations after new partner admissions or ownership changes

Reverse §704(c) layers from book‑ups or book‑downs

Software defaults that do not match the selected allocation method

Where §704(c) focuses on contributed or revalued property, §754 review focuses on ownership transfers and distributions that may require basis adjustment analysis.

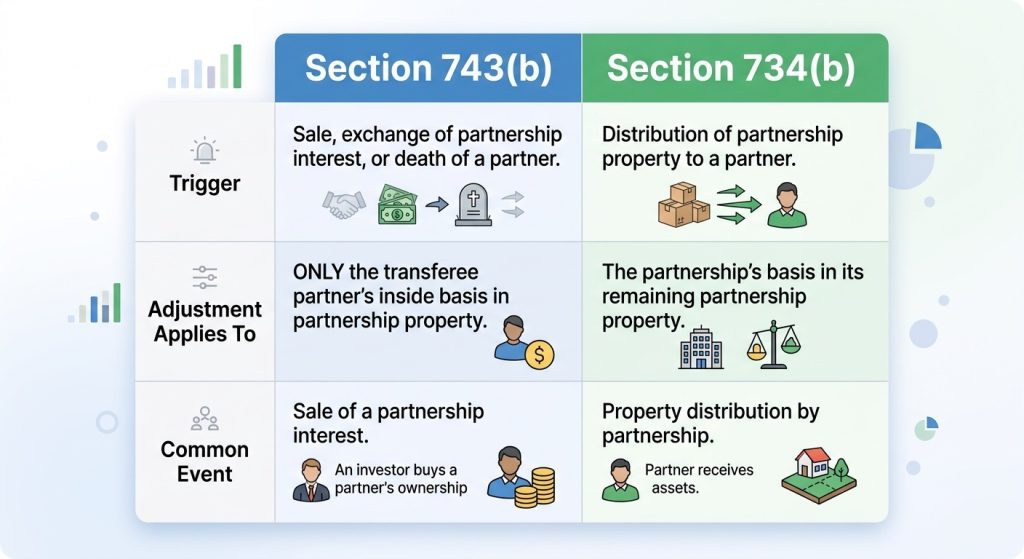

How CPAs Review §754 Elections, §743(b), and §734(b) Adjustments

A §754 election allows a partnership to adjust inside basis under §743(b) or §734(b) when certain transfers or distributions occur. The IRS §754 election FAQ explains that a §754 election can apply when there is a distribution of partnership property or certain transfers of a partnership interest.

For CPA review, the first question is whether a triggering event occurred during the year.

§754 Election Review Questions

Review question

Why it matters

Did a partner sell, exchange, or transfer an interest?

May trigger §743(b) analysis if §754 is in effect.

Did a partner die during the year?

May create a transferee basis adjustment issue.

Did the partnership distribute property?

May trigger §734(b) analysis.

Is a §754 election already in effect?

The election generally continues beyond the year it is made unless revoked with IRS consent.

Is there a substantial built‑in loss or substantial basis reduction?

Some mandatory basis adjustment rules may apply even without a voluntary election.

The Main Difference Between §743(b) and §734(b)

Distinguishing between Section 743(b) and Section 734(b) is critical for accurate inside basis adjustments.

Once basis adjustment events are reviewed, the next partner‑level issue is whether income has been classified correctly for self‑employment tax purposes.

How CPAs Review Self-Employment Income on Schedule K-1 Box 14

Self‑employment income review should focus on partner status, activity level, guaranteed payments, and whether the K‑1 treatment is consistent with the facts.

General partners often require a different review than limited partners or LLC members. LLC members need extra attention because state‑law labels do not always answer the federal self‑employment tax question.

Identify whether the partner is a general partner, limited partner, LLC member, or passive investor.

Confirm whether guaranteed payments for services are included in self‑employment income.

Review whether rental income is separated from trade or business income.

Document the reason for excluding any active partner’s distributive share from self‑employment income.

Review the current authority before relying on the limited partner exception for active LLC members.

Avoid treating every LLC member the same way. The review should be fact‑based.

That same fact‑based approach also applies to guaranteed payments, which are often misclassified when firms do not compare the payment terms to the partnership agreement.

How CPAs Review Guaranteed Payments Under §707(c)

Guaranteed payments should be reviewed because they affect both partnership deductions and partner‑level income treatment. A payment to a partner is not automatically a guaranteed payment just because it is fixed or recurring.

The review should confirm:

Whether the payment is for services, capital, or another arrangement

Whether the payment is determined without regard to partnership income

Whether the payment was correctly reported on Schedule K‑1

Whether the payment affects self‑employment income

Whether the partnership agreement supports the treatment

The common error is confusing a preferred return with a guaranteed payment. If the payment depends on partnership income, it may be an allocation rather than a guaranteed payment.

After payment classification is checked, the next review item is capital reporting, where tax‑basis capital and outside basis are often confused.

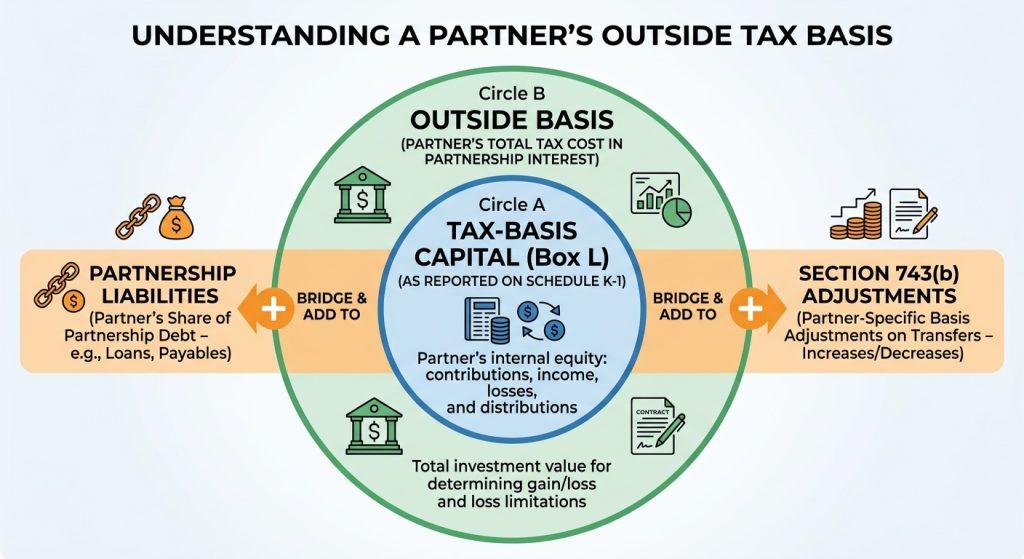

How CPAs Review Tax-Basis Capital on Schedule K-1 Box L

Box L capital reporting is only one component of a partner’s total outside basis calculation.

Tax‑basis capital reporting should be reviewed separately from outside basis. K‑1 Box L reports capital using the tax‑basis method, but it does not equal the partner’s complete outside basis.pkfod+1

The distinction matters because outside basis can include items not shown in tax‑basis capital, such as partnership liabilities and certain partner‑specific basis adjustments.

A practical review should include:

Beginning tax‑basis capital

Current‑year contributions

Allocated income and gain

Allocated deductions and losses

Distributions

Ending tax‑basis capital

Partner debt share tracked outside Box L

Partner‑specific §743(b) adjustments tracked outside Box L

The common review mistake is using Box L as the entire outside basis calculation. That can create downstream errors in loss limitations, at‑risk calculations, and partner‑level reporting.

Capital reporting should then be reconciled against the return’s book‑tax schedules, so the full filing package is internally consistent.

How CPAs Reconcile Schedule M-1, M-2, and M-3

The reconciliation schedules help confirm whether book income, tax income, capital accounts, and K‑1 totals are internally consistent. Not every partnership files every schedule, but the reviewer should confirm whether the return qualifies for any exemption.

Schedule L, M-1, M-2, and M-3 Review Overview

Schedule

Review purpose

Schedule L

Confirms balance sheet reporting where required.

Schedule M‑1

Reconciles book income to tax income for smaller partnerships not filing M‑3.

Schedule M‑2

Tracks partners’ capital account changes.

Schedule M‑3

Provides detailed book‑tax reconciliation for larger partnerships or those meeting filing thresholds.

Common reconciliation items include depreciation differences, meals limitations, nondeductible expenses, §179, guaranteed payments, and book‑tax timing differences.

If the review includes depreciation or OBBBA‑related depreciation planning, link to the CPA Pilot’s bonus depreciation rules guide.

Once domestic reconciliation is complete, the reviewer should check whether any foreign partner or cross‑border reporting issue changes the filing package.

Foreign Partner Withholding Checks for Form 1065 Review

Partnerships with foreign partners may have withholding and reporting obligations under §1446. The IRS Form 8804 overview explains that Form 8804 reports the partnership’s total §1446 withholding tax liability and acts as a transmittal form for Forms 8805.

The IRS Instructions for Forms 8804, 8805, and 8813 explain that these forms are used to pay and report §1446 withholding tax based on effectively connected taxable income allocable to foreign partners.

A Form 1065 review should confirm:

Whether any partner is foreign

Whether effectively connected taxable income is allocable to foreign partners

Whether withholding credits match partner statements

If the partnership has international reporting issues tied to partner disclosures, use CPA Pilot’s Schedules K‑2 and K‑3 filing guide as the supporting internal resource.

Form 1065 Review Errors That Cause the Most Problems

The most serious Form 1065 errors are usually workflow errors. They happen when one part of the return is technically completed but not supported by another part of the file.

Error pattern

Why it creates risk

The election review happens too late

§754 decisions can be missed after transfers, deaths, or distributions.

Allocations are reviewed without the agreement

K‑1 reporting may not match the economic deal between partners.

Book‑tax differences are not tracked

§704(c) and reverse §704(c) layers can be lost over time.

Capital is reviewed only at year‑end

Beginning balances, contributions, distributions, and allocations may not tie.

Partner status is assumed

SE income treatment can be wrong when LLC participation is not reviewed.

Payment labels are accepted without testing

Preferred returns and guaranteed payments can be misclassified.

International status is not checked early

Foreign partner withholding issues can be missed until filing.

Box 20 is treated as a software output only

Partner‑level deductions and limitations may lack required disclosure support.

No written review trail exists

The firm may struggle to explain technical decisions later.

If a filing issue later turns into correspondence, CPA teams can also use CPA Pilot’s guide on AI for IRS notice response and compliance to structure the follow‑up workflow.

These failure patterns show why firms need a repeatable review process, not just experienced reviewers working from memory.

Form 1065 Review Checklist for CPA Firms

Avoiding common workflow failure patterns is essential for maintaining firm compliance and accuracy.

Use this checklist before the final partner or manager sign‑off.

Review area

What to confirm

Filing status

Confirm original or extended due date.

Partner list

Check ownership changes, new partners, exits, deaths, and transfers.

K‑1 allocations

Match income, loss, deductions, and credits to the agreement.

Capital accounts

Tie beginning capital, contributions, allocations, distributions, and ending balances.

§704(b)

Confirm special allocations have support.

§704(c)

Identify contributed or revalued property with book‑tax differences.

§754

Confirm election status and triggering events.

§743(b)/§734(b)

Review basis adjustment needs after transfers or distributions.

Box 14

Review self‑employment income treatment.

Guaranteed payments

Confirm §707(c) treatment and K‑1 reporting.

Box 20

Confirm required partner‑level disclosures.

Foreign partners

Confirm whether withholding or international reporting applies.

M schedules

Tie the book income, taxable income, and capital account changes.

Review notes

Document unresolved technical issues before filing.

A checklist helps standardize review, but CPAs still need judgment on elections, allocations, basis, and partner‑specific reporting.

How CPA Pilot Supports Form 1065 Review Workflows

Form 1065 review is no longer just about checking partnership return fields; it’s about spotting how allocations, capital accounts, basis adjustments, elections, partner disclosures, and withholding rules interact before they create review delays, amended returns, or client questions.

Stop spending hours moving between IRC sections, IRS instructions, form pages, K‑1 instructions, partnership agreements, and fragmented guidance. Start giving reviewers clearer issue notes, faster research summaries, and better‑documented partner‑level explanations.

Try CPA Pilot today and see how AI‑powered tax research can support a Form 1065 review workflow for CPAs:

Instant IRC and regulation support for §704(b), §704(c), §754, §743(b), §734(b), §707(c), and §1446 review

Research‑ready summaries that help CPAs connect K‑1 reporting, capital accounts, allocations, and basis issues across one partnership return

Client explanation drafts for partnership elections, basis adjustments, guaranteed payments, and foreign partner withholding questions

Review‑note support for documenting why an allocation, election, disclosure, or withholding item needs deeper analysis

Faster research workflows that help tax teams spend less time searching and more time reviewing the return file

CPA Pilot does not replace CPA judgment. It helps reviewers move faster, organize authority, and explain complex partnership return issues with more confidence.

Book a CPA Pilot demo and see how AI‑supported tax research can fit into your firm’s review workflow.

Your next partnership return may already have allocation, basis, or K‑1 issues hiding in the file. Don’t let research bottlenecks slow down the review.

Before using any AI‑supported workflow, firms should still define what the article covers and where professional judgment or legal review is required.

Form 1065 Review FAQs

What Records Should CPAs Request Before Starting Form 1065 Review?

CPAs should request the partnership agreement, trial balance, general ledger, ownership changes, capital schedules, debt details, fixed asset reports, and prior‑year Form 1065 before review

How Early Should CPA Firms Start Reviewing Form 1065?

CPA firms should start Form 1065 review after year‑end books close and before K‑1 delivery. Early review gives teams time to resolve capital, allocation, ownership, and basis issues.

What Makes a Partnership Return More Complex to Review?

Ownership changes, special allocations, contributed property, partner debt, foreign partners, tiered partnerships, and property distributions make Form 1065 review more complex for CPAs.irs+1

Should CPAs Review the Partnership Agreement Before Form 1065?

Yes. The partnership agreement controls allocations, distributions, capital terms, buy‑sell rules, and special provisions. CPAs use it to test whether Form 1065 matches the economic deal.

What is the Difference Between Form 1065 Review and Schedule K-1 Review?

Form 1065 review checks the full partnership return. K‑1 review checks each partner’s reported share of income, deductions, credits, capital, distributions, and disclosures.irs+1

Disclaimer: This article is provided by CPA Pilot for educational purposes. While we may offer tax software/services, the information here is general and may not address your specific facts and circumstances. It does not constitute individual tax, legal, or accounting advice. U.S. federal and State Tax laws change frequently; please consult a qualified tax professional before acting on any information.

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.