R&D Tax Credit for CPAs – How to Qualify, Calculate & File Form 6765 - CPA Pilot

Federal Tax Automation

R&D Tax Credit for CPAs – How to Qualify, Calculate & File Form 6765

CPA Pilot

Apr 13, 2026·17 min read

How can CPAs accurately identify, calculate, and claim the R&D tax credit without spending hours on manual analysis – or risking costly compliance errors?

The R&D tax credit for CPAs is defined under Internal Revenue Code Section 41. It allows businesses to claim tax credits for qualified research activities (QRAs) and qualified research expenses (QREs), including wages, supplies, and contract research tied to innovation, product development, or process improvement.

TL;DR for CPAs on the R&D Tax Credit

The R&D tax credit helps businesses reduce tax liability when they perform qualified research activities and incur qualified research expenses under IRC Section 41.

CPAs can identify eligibility by applying the IRS 4-part test to product, process, software, and technical improvement work.

Qualified research expenses usually include employee wages, contractor costs, and supplies directly tied to eligible research.

Businesses can calculate the credit using the Regular Credit method or the Alternative Simplified Credit (ASC), depending on available data.

CPAs claim the credit through Form 6765 and must support the claim with clear documentation, expense mapping, and technical narratives.

Strong documentation reduces audit risk and helps firms defend claims during IRS review.

SaaS companies, startups, and manufacturers often qualify when their work involves technical uncertainty and experimentation.

AI-powered workflows help CPAs identify qualifying activities faster, organize QREs, improve documentation, and streamline filing.

In practice, claiming this credit requires applying the IRS-defined 4-part test, calculating eligible expenses under established methodologies, and filing through Form 6765, supported by the proper documentation aligned with IRS expectations.

For detailed audit and qualification guidance, the IRS also provides a Research Credit Audit Techniques Guide, which outlines how examiners evaluate eligibility, substantiation, and risk areas.

For CPAs, this is not just a compliance exercise; it’s a high-impact advisory opportunity.

According to the National Science Foundation, U.S. businesses spent over $892 billion on research and development in 2022, highlighting the scale of potential credits available. (Source)

Yet despite the opportunity, many firms struggle with:

Identifying qualifying activities across multiple business functions

Accurately mapping financial data to QRE categories

Maintaining audit-ready documentation under IRS scrutiny

This is where structured workflows, and increasingly, AI-powered systems, are changing how CPAs approach the R&D credit. This is especially relevant for firms already looking to build time-saving tax workflows for CPAs without adding more manual review steps.

Instead of treating it as a one-time calculation, leading firms are building repeatable processes that improve accuracy, reduce manual effort, and strengthen compliance.

In this guide, we’ll move beyond basic definitions and show exactly how CPAs can determine eligibility using the 4-part test, apply real-world examples across industries, calculate credits accurately, file using Form 6765, and build a repeatable, audit-ready workflow

Let’s break down the foundation of every R&D credit claim, but before that, let’s have a quick look at what the R&D tax credit actually is.

What is the R&D Tax Credit (Under IRC Section 41)?

The R&D tax credit is a federal incentive defined under Internal Revenue Code Section 41 that allows businesses to reduce their tax liability for qualified research activities. It applies when companies develop or improve products, processes, software, or technologies and incur eligible expenses tied to that work.

For many firms, research credit work sits at the intersection of documentation, technical analysis, and AI for tax research.

What Activities and Expenses Qualify for the R&D Tax Credit?

Qualifying activities for R&D tax credit generally involve technical uncertainty, experimentation, and an evaluation process. Common eligible expenses known as qualified research expenses (QREs) include employee wages, contractor costs, and supplies directly used in research.

Eligibility is determined using the IRS 4-part test, which we’ll break down next.

Why the R&D Tax Credit Matters for CPAs?

The R&D credit creates a direct opportunity for CPAs to deliver measurable tax savings and advisory value. Instead of treating it as a compliance task, firms can use it to uncover overlooked credits, improve client outcomes, and strengthen long-term relationships, especially for startups, SaaS, and innovation-driven businesses.

For many firms, research credit work sits at the intersection of documentation, technical analysis, and AI for tax research

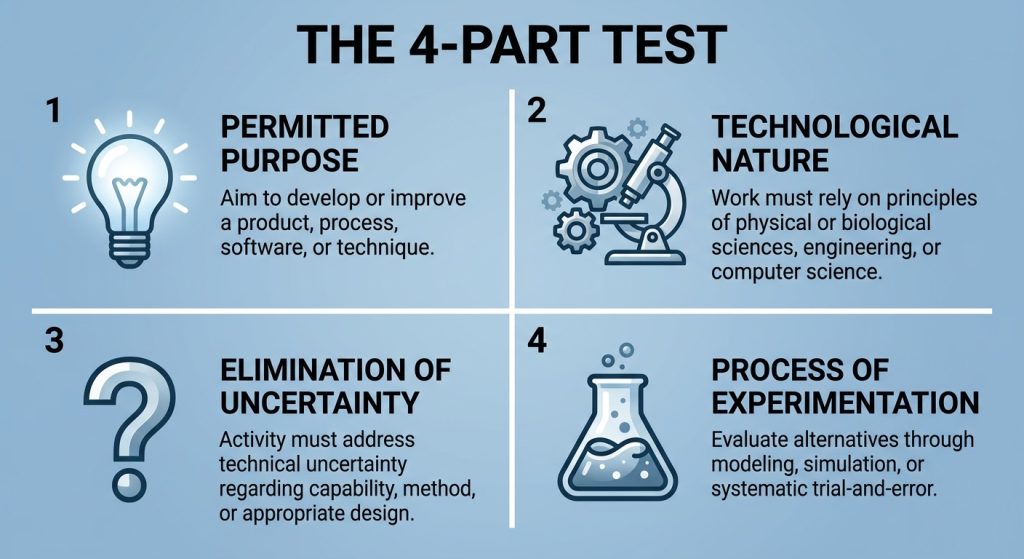

R&D Tax Credit Qualifications (4-Part Test Explained)

To determine eligibility, the Internal Revenue Service applies a structured 4-part test that evaluates whether an activity qualifies as research under tax law.

Use the IRS 4-Part Test to validate every R&D claim for compliance.

The 4-Part Test for Qualified Research Activities

Permitted Purpose: The activity must aim to create or improve a product, process, software, or technique.

Technological in Nature: It must rely on principles of engineering, physics, computer science, or similar technical fields.

Elimination of Uncertainty: The work should address uncertainty related to capability, method, or design.

Process of Experimentation: The activity must involve testing, modeling, simulation, or iterative evaluation.

All four criteria must be satisfied for the activity to qualify.

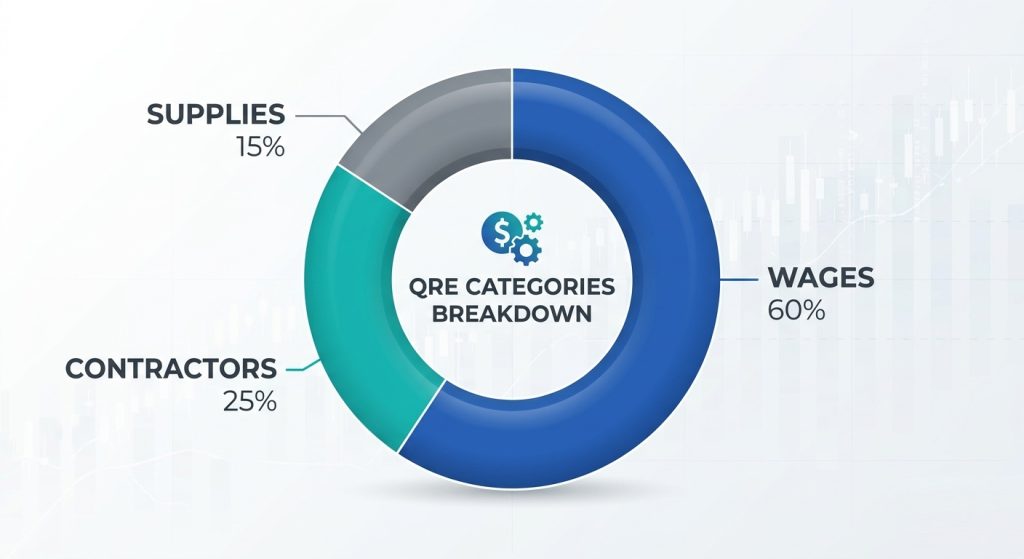

What Counts as Qualified Research Expenses (QREs)?

Accurately mapping wages, contractors, and supplies is critical for a defensible claim.

Once activities meet eligibility, CPAs must map associated costs into qualified research expenses (QREs). These typically include:

Wages for employees directly performing, supervising, or supporting research

Contract research costs are usually a percentage of third-party expenses

Supplies used in testing or development (excluding capital equipment)

Accurate classification is critical, as misallocation can materially impact the final credit calculation. The same structured review approach used to assess qualified activities also supports broader efforts to automate 1040 tax preparation using AI.

Common R&D Tax Credit Eligibility Mistakes CPAs Should Avoid

R&D tax credit eligibility errors often arise not from complexity, but from incorrect assumptions.

Common pitfalls include:

Treating routine or cosmetic changes as qualifying research

Failing to document uncertainty and experimentation

Including non-technical activities such as market research or quality control

Overlooking partial qualification within broader projects

These mistakes can weaken claims and increase exposure during IRS review.

Examples of Qualifying vs Non-Qualifying Activities for R&D Tax Credit

Qualifying R&D Activities:

Developing a new software architecture to improve system performance

Designing and testing prototypes for a new manufacturing process

Iteratively refining algorithms or technical models

Non-Qualifying R&D Activities:

Minor UI changes without technical complexity

Reverse engineering without innovation

Routine data entry or standard configuration tasks

Now that eligibility is clearly defined, the next step is understanding the calculation of the R&D tax credit.

How to Calculate the R&D Tax Credit?

CPAs can calculate the R&D tax credit using two primary methods, each with different data requirements and outcomes:

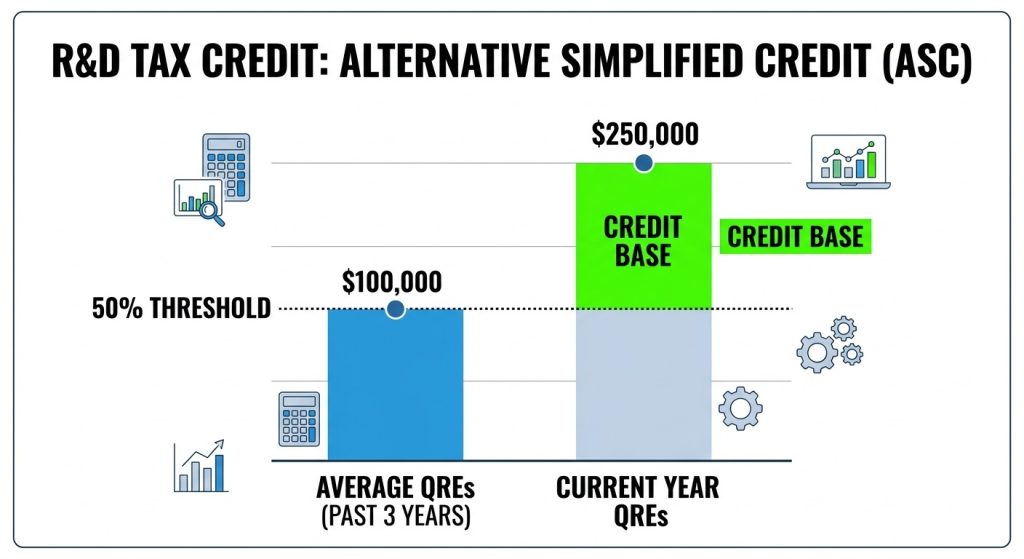

Regular Credit vs Alternative Simplified Credit (ASC)

The ASC method provides a simplified path to claiming credits based on recent spending growth.

Regular Credit Method: Based on a fixed-base percentage applied to current-year qualified research expenses (QREs). This method often requires historical data, making it more complex but sometimes more beneficial for established businesses.

Alternative Simplified Credit (ASC): Calculates the credit as a percentage of current-year QREs exceeding 50% of the average QREs from the previous three years. This method is simpler and widely used when historical base calculations are not feasible.

Selecting the appropriate method depends on data availability and which approach yields a higher credit.

Step-by-Step QRE Calculation Process

Once the method is selected, the calculation process follows a structured approach:

Aggregate all eligible QREs across wages, contractor costs, and supplies

Segregate expenses by project or activity to ensure traceability

Apply the chosen calculation method (Regular or ASC)

Adjust for exclusions or limitations based on IRS rules

Validate totals against financial records to ensure consistency

This structured breakdown ensures both accuracy and defensibility.

This simplified example illustrates how proper calculation can translate into significant tax savings for clients.

Note: If a business has no qualified research expenses in the prior three years, the ASC is calculated as 6% of current-year QREs.

Common R&D Tax Credit Calculation Errors and Adjustments

Even when R&D tax credit eligibility is correctly established, calculation errors can reduce or invalidate the credit:

Misclassifying wages or including non-qualified costs

Failing to normalize historical data for ASC calculations

Double-counting expenses across projects

Ignoring aggregation rules for controlled groups

Addressing these issues early ensures the calculated credit remains both accurate and defensible during review.

How to File the R&D Tax Credit Using Form 6765?

The R&D tax credit is formally claimed using Form 6765, available on the Internal Revenue Service website. This form is attached to the taxpayer’s income tax return and is structured to capture the calculation method, total credit amount, and relevant adjustments.

Form 6765 is divided into key sections, including:

Section A (Regular Credit)

Section B (Alternative Simplified Credit – ASC)

Section C (Current-year credit summary)

Section D (Qualified Small Business Payroll Tax Election and Payroll Tax Credit)

Each section must align with the calculation approach selected and the taxpayer’s filing position.

Step-by-Step Form 6765 Filing Process for CPAs

To ensure accurate submission, CPAs typically follow a structured filing workflow:

Finalize credit calculation using the selected method

Complete the relevant sections of Form 6765 based on eligibility and method

Transfer the calculated credit to the appropriate line in the client’s tax return (e.g., corporate or individual return)

Review aggregation rules for controlled groups or multiple entities

Validate consistency between Form 6765, financial records, and supporting schedules

Attach the form to the federal tax return before submission

This process ensures the credit is properly reported and integrated into the overall tax filing.

Beyond completing the form, the Internal Revenue Service requires detailed supporting information to substantiate the claim. This includes:

Descriptions of research activities and their technical objectives

Methodologies used to calculate qualified expenses

Identification of business components involved in the research

Documentation linking expenses directly to qualifying activities

In recent years, the IRS has increased scrutiny on R&D claims, requiring clearer disclosures to reduce ambiguity and improve transparency during review.

Common Form 6765 Errors CPAs Should Avoid

Errors in filing can delay processing or trigger additional scrutiny. Common issues include:

Incomplete or inconsistent reporting across form sections

Misalignment between the calculated credit and the reported figures

Missing or insufficient activity descriptions

Incorrect handling of payroll tax election for startups

Failure to apply aggregation rules correctly

These issues can lead to processing delays, requests for additional information, or even rejection.

👉 With filing complete, the next step is understanding how CPAs can build a repeatable, end-to-end workflow that ensures accuracy, efficiency, and audit readiness across multiple client engagements.

Step-by-Step R&D Credit Process for CPAs

Step 1: Identify Qualifying Activities Across Client Operations

Begin by mapping where technical work actually happens inside the business. This typically spans product teams, engineering, manufacturing, or process improvement units. Instead of relying only on client summaries, review project documentation, sprint logs, technical specs, and internal reports to uncover activities that involve experimentation or technical problem-solving.

At this stage, AI-assisted tax planning platforms like CPA Pilot can help scan large volumes of operational data and surface potential qualifying activities faster, reducing manual discovery time.

Step 2: Gather and Categorize Qualified Research Expenses (QREs)

Once activities are identified, the next step is aligning financial data with those activities. This requires pulling payroll records, contractor payments, and expense reports, then mapping them accurately to specific projects. The key here is traceability; every dollar claimed should connect back to a qualifying activity.

CPA Pilot can assist by organizing financial data into structured categories, helping CPAs quickly identify expense patterns linked to eligible work.

Step 3: Apply the 4-Part Test and Validate Eligibility

With activities and expenses aligned, validate each project against eligibility criteria. This step ensures consistency across engagements and prevents over- or under-claiming. It also helps standardize decision-making across teams, especially in multi-client environments.

AI-driven analysis within CPA Pilot can support this validation by highlighting gaps, inconsistencies, or borderline cases that require closer review.

Step 4: Calculate the Credit Using the Right Method

After validation, apply the selected calculation method across all qualified projects. This involves consolidating categorized expenses, ensuring proper treatment across entities, and confirming that calculations align with the client’s tax position.

CPA Pilot can streamline this step by structuring inputs and reducing manual recalculations across multiple scenarios.

Step 5: Prepare Documentation for IRS Compliance and Audit Defense

Documentation should be built alongside the workflow, not after. Create structured narratives that explain the technical challenges, experimentation process, and how expenses relate to each activity. Supporting records should be organized in a way that is easy to retrieve and defend.

CPA Pilot helps generate structured summaries and documentation drafts, improving consistency and audit readiness.

Step 6: File Form 6765 and Review for Accuracy

The final step is integrating all outputs into the filing process. Before submission, review for alignment across calculations, documentation, and reported figures. This ensures the claim is complete, consistent, and ready for submission without unnecessary back-and-forth.

👉 With a structured workflow in place, the next critical layer is ensuring that every claim is supported by strong documentation and can withstand IRS scrutiny.

R&D Tax Credit Documentation, Audit Risk, and Compliance

The Internal Revenue Service expects taxpayers to maintain contemporaneous records that clearly connect research activities to claimed expenses.

IRS Documentation Requirements for R&D Tax Credit Claims

This typically includes technical project documentation, time-tracking records, financial reports, and narratives explaining the nature of the work performed.

A well-prepared claim should demonstrate:

The business component being developed or improved

The technical uncertainty addressed

The process of experimentation undertaken

The direct link between expenses and activities

Documentation should be structured in a way that an independent reviewer can understand the claim without additional clarification.

What Triggers an R&D Tax Credit Audit

R&D claims often receive heightened attention due to their complexity and variability. Certain patterns can increase the likelihood of review, such as:

Significant year-over-year fluctuations in claimed credits

Large credits relative to company size or revenue

Claims lacking detailed technical descriptions

Inconsistencies between financial data and reported expenses

These signals do not automatically result in disallowance, but they can prompt deeper examination.

How CPAs Can Reduce R&D Tax Credit Audit Risk

Reducing exposure requires a proactive approach rather than reactive corrections. CPAs can strengthen claims by:

Maintaining clear and consistent documentation standards across all clients

Aligning technical narratives with financial records

Using standardized methodologies for expense classification

Reviewing claims for completeness before submission

A SaaS company builds a new feature to improve system scalability under high user load. The engineering team tests multiple architectures, runs performance benchmarks, and iterates based on failures.

Does not qualify: UI styling updates or routine bug fixes without technical uncertainty This scenario shows how technical problem-solving within software development often creates eligible credit opportunities.

An early-stage startup with limited revenue develops a proprietary platform while operating at a loss. Instead of applying the credit against income tax, the company elects to offset payroll taxes.

Key consideration: Meeting eligibility thresholds for payroll tax election This is a common use case where startups can realize immediate cash flow benefits.

For startups choosing between income tax benefit and payroll tax offset, forward-looking modeling becomes easier when paired with AI for tax projection

Manufacturing R&D Tax Credit Example

A manufacturing firm redesigns part of its production process to reduce material waste and improve efficiency. The team experiments with different materials, machinery settings, and production methods.

Qualifies: Process redesign, testing new configurations, iterative improvements

Does not qualify: Routine production or standard quality control checks This highlights how operational improvements – not just new products – can qualify.

Manufacturing clients often evaluate research credits alongside other capital and equipment-related items such as bonus depreciation.

R&D Tax Credit Edge Cases CPAs Should Review

Some scenarios require deeper evaluation due to mixed activities:

Partial qualification: Only the experimental portion of a project qualifies

Third-party involvement: Contractor work may qualify at a reduced percentage

Internal-use software: Additional scrutiny applies depending on purpose and complexity

These edge cases emphasize the importance of careful analysis when applying eligibility rules in practice.

Entity structure can also affect how advisors think about compliance, filings, and planning strategy, which is why many firms compare S corp vs C corp vs LLC rules alongside incentive planning.

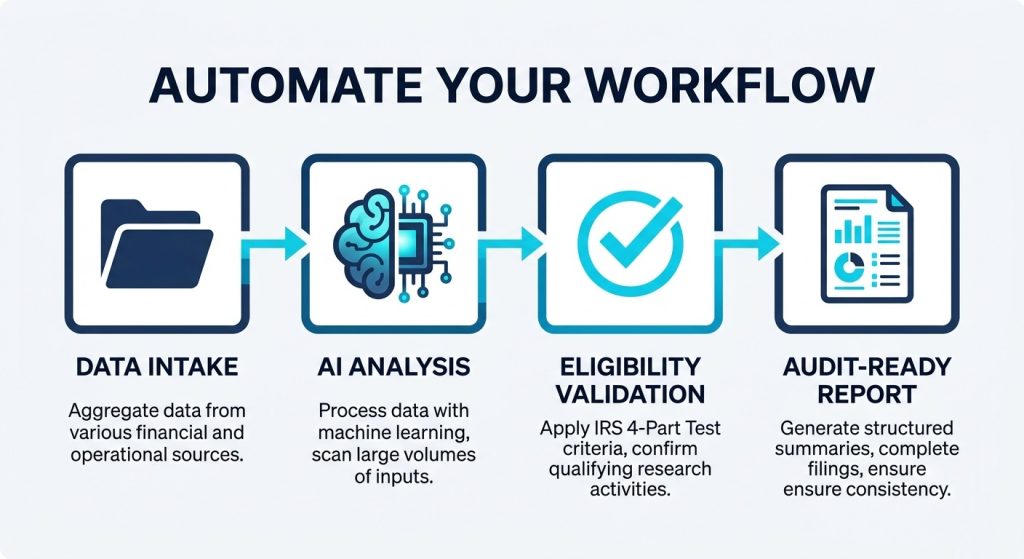

How AI Helps CPAs Automate R&D Tax Credit Workflows

Even with a defined process, scaling R&D credit work across multiple clients introduces friction. CPAs often deal with fragmented data sources, inconsistent project descriptions, and time-intensive reconciliation between operational and financial records. As client complexity grows, maintaining speed without compromising accuracy becomes increasingly difficult.

AI-powered platforms like CPA Pilot transform manual analysis into a repeatable, audit-ready process.

Challenges in Manual R&D Tax Credit Analysis:

Manual R&D tax credit analysis often involves reviewing fragmented financial and project data across teams, which increases time, inconsistency, and the risk of missed qualifying activities.

It also makes documentation, expense mapping, and audit readiness harder to manage, especially when handling multiple clients or complex engagements.

How AI Identifies Qualified Activities and Expenses

AI systems can analyze large volumes of structured and unstructured data, such as project notes, financial records, and internal documentation, to detect patterns that indicate eligible work.

This reduces reliance on manual review and helps surface opportunities that might otherwise be missed, especially in businesses with multiple departments or evolving projects.

How AI Automates Documentation and Audit Readiness

Instead of building documentation manually for each engagement, AI can generate structured summaries that align activities, expenses, and technical narratives in a consistent format.

This ensures that every claim is supported by clear, well-organized records, improving readiness for review and reducing last-minute preparation effort.

How CPA Pilot Supports End-to-end R&D Tax Credit Workflows?

CPA Pilot brings these capabilities into a single workflow designed specifically for CPAs and tax firms. It helps teams move from data collection to final output faster by:

Structuring client data into actionable insights

Highlighting potential qualifying activities across operations

Organizing expense categories for accurate credit calculations

Generating consistent, audit-ready documentation

By integrating these steps into one system, CPAs can handle more complex engagements with greater confidence and efficiency—without increasing manual workload.

So, stop leaving valuable tax credits on the table. Start identifying, calculating, and documenting R&D claims confidently. If your team wants a faster way to identify, calculate, and document research credits, you can book a CPA Pilot demo to see the workflow in practice. Teams comparing tools can also review CPA Pilot’s pricing plans before choosing a workflow for R&D credit analysis

R&D Tax Credit FAQs for CPAs

Who Qualifies for the R&D Tax Credit?

Businesses qualify for the R&D tax credit when they perform activities that meet the IRS 4-part test and incur qualified research expenses such as wages, supplies, or contractor costs tied to product, process, software, or technical improvement.

Can Startups Claim the R&D Tax Credit?

Startups can claim the R&D tax credit if they have qualified research expenses and meet IRS requirements. Qualified small businesses can also apply up to $500,000 of the credit against payroll tax, subject to current eligibility rules.

What is Form 6765 Used For?

Form 6765 is used to calculate and claim the federal R&D tax credit. Taxpayers use it to report the regular credit or ASC method, current-year credit, and payroll tax election when eligible.

How Much Can Businesses Save With the R&D Tax Credit?

Businesses can save thousands to millions of dollars with the R&D tax credit, depending on qualified research expenses, calculation method, entity structure, and payroll tax eligibility. Savings increase when documentation and expense mapping are accurate.

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.