![Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]](https://www.cpapilot.com/blog/wp-content/uploads/2026/05/Washington-BO-Tax-.png)

Small Business Tax Planning Strategies to Lower Your Taxes

[Last Updated on 1 month ago]

Small business tax planning strategies reduce tax liability by structuring business decisions around entity selection, deductions, tax credits, income timing, and year-round compliance. These strategies help businesses legally lower taxes, improve cash flow, and align financial decisions with long-term growth.

TL;DR: Small Business Tax Planning Strategies

- Design decisions (entity, compensation, investment timing) before transactions so tax outcomes are proactive, not reactive.

- Use 7 levers year‑round: entity choice, deduction systems, early credit planning, depreciation timing, income timing, state/PTE strategy, and retirement/compensation planning.

- Adapt strategy to business model (service, e‑commerce, asset‑intensive, startup, professional practice) and lifecycle stage (formation, growth, hiring, expansion, exit).

- Revisit tax strategy at key trigger points: revenue jumps, hiring, multi‑state expansion, big asset purchases, year‑end, and ownership or funding changes.

- Avoid common mistakes: year‑end‑only planning, outdated entity structure, weak documentation, missed credits, ignoring state nexus, and one‑size‑fits‑all advice.

- Use AI Tax tools like CPA Pilot to speed up tax research, scenario modeling, and client‑ready recommendations, while still relying on professional judgment.

According to the research, small businesses represent 99.9% of all U.S. businesses, making tax efficiency a critical factor in profitability and sustainability. (Source)

Effective tax planning is proactive, not reactive. It requires evaluating financial activities before they occur, identifying opportunities to reduce taxable income, and applying strategies based on business structure, industry, and growth stage. Tools like CPA Pilot support this process by helping CPAs and business owners analyze tax scenarios, identify relevant strategies, and generate actionable insights more efficiently.

Table of Contents

- What Small Business Tax Planning Actually Means?

- Why Most Small Businesses Overpay Taxes?

- Identify Key Small Business Tax Planning Strategies

- The 3 Core Tax Planning Interactions That Drive Most Savings

- Apply 7 Core Small Business Tax Planning Levers

- Adapt Tax Planning by Business Type

- How Tax Strategy Changes Across the Business Lifecycle?

- Use Industry-Specific Tax Planning Strategies

- Tax Planning as a Workflow, Not a Checklist

- Revisit Small Business Tax Strategy at Key Stages

- Avoid 6 Common Small Business Tax Planning Mistakes

- Use AI to Improve Small Business Tax Planning

- Build a Tax Plan That Fits Your Business Model

- Answer Small Business Tax Planning Questions

What Small Business Tax Planning Actually Means?

Tax planning for small businesses is not just about “saving taxes”—it’s about designing financial decisions in advance so taxes become predictable, optimized, and aligned with business growth.

At its core, it means structuring your income, expenses, and business setup to legally minimize tax liability while improving after-tax profitability.

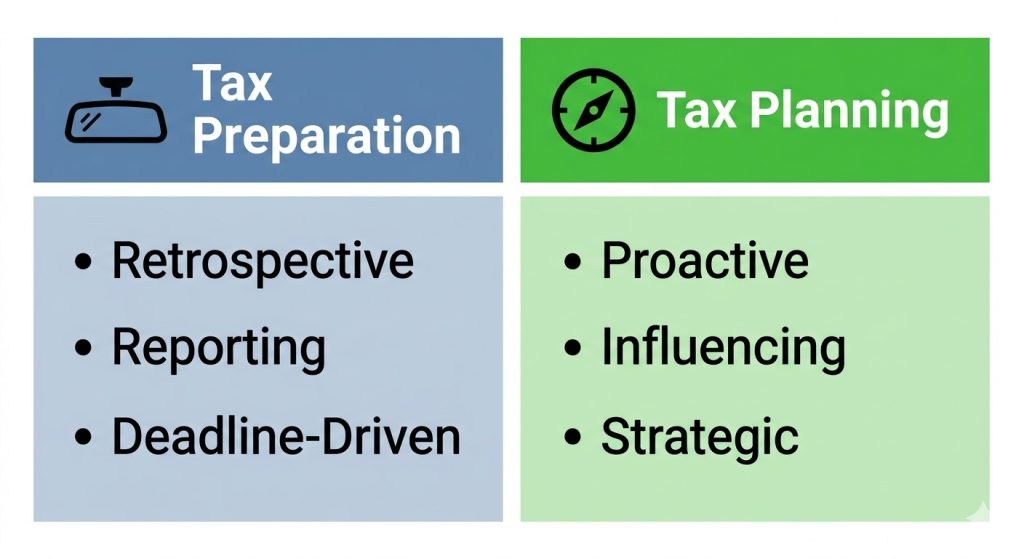

Tax Planning vs. Tax Preparation

- Tax planning = forward-looking strategyIt focuses on reducing future tax liability by making smart decisions before transactions happen.

- Tax preparation = backward-looking reportingIt deals with filing returns based on what has already happened.

👉 In simple terms: Preparation reports history. Planning shapes outcomes.

Why tax planning must happen before transactions?

Most tax outcomes are determined at the time decisions are made—not at filing time.

- Choosing an entity (LLC, S-Corp, etc.) affects how income is taxed

- Structuring compensation (salary vs distributions) changes tax exposure

- Timing purchases (equipment, investments) impacts deductions

- Deferring or accelerating income can shift tax brackets

Once a transaction is completed, your flexibility drops significantly. That’s why effective tax planning is proactive, not reactive.

Who needs structured tax planning?

Tax planning is not just for large corporations. It becomes critical as soon as financial complexity increases.

It is especially relevant for:

- Small business owners → managing profit, cash flow, and taxes together

- Entrepreneurs & founders → making early decisions on entity and compensation

- CPAs handling multiple clients → standardizing strategy and improving outcomes

- Growing firms → dealing with multi-entity structures, payroll, and expansion

Why Most Small Businesses Overpay Taxes?

Strategy does not fail; execution timing does

Most small business tax planning strategies fail due to timing misalignment, not incorrect strategy selection. Businesses often choose the right structure, deductions, or credits—but apply them after financial decisions are already locked.

A business that elects S-Corporation status after income is earned cannot retroactively optimize payroll tax exposure. A company that purchases equipment in January instead of December shifts depreciation benefits into the next tax year, delaying tax savings.

Tax outcomes depend on when decisions are made relative to financial activity, not just what decisions are made.

Real-world interaction failure: entity + timing

A business earning $400,000 elects S-Corp status mid-year:

- Salary not adjusted → excess self-employment tax

- Distributions misaligned → reduced tax efficiency

- No QBI planning → missed deduction optimization

The structure was correct. The sequence was not.

Why year-end planning limits outcomes

Year-end planning compresses decisions into a narrow window:

- Limited flexibility for income shifting

- Limited time for restructuring compensation

- Reduced ability to qualify for credits

Effective tax planning requires pre-transaction positioning, not post-transaction adjustments.

Identify Key Small Business Tax Planning Strategies

The most effective approach to strategize small business tax planning is to focus on controlling how income is taxed, how expenses are recognized, and how business decisions interact with tax rules throughout the year. Let’s discuss this in detail:

1. Choose the Right Tax Structure

The way a business is taxed depends on how profits flow to owners, whether income is subject to self-employment tax, and how distributions are handled as the business scales.

2. Maximize Tax Deductions and Credits

Tax savings increase when expenses are consistently tracked, and activities are aligned with eligibility requirements for credits tied to hiring, development, or operations.

3. Control Income and Expense Timing

Shifting when revenue is recognized, or costs are incurred, can help stabilize taxable income during periods of growth or fluctuating cash flow.

4. Plan Depreciation and Capital Purchases

Large purchases can be structured to create an immediate tax impact, especially when aligned with periods of higher earnings.

5. Reduce Taxes with Retirement and Compensation

Owner compensation and retirement contributions can be structured to balance current tax savings with long-term financial planning.

6. Manage State and Multi-State Tax Exposure

Expanding operations, hiring remotely, or selling across jurisdictions can trigger new tax obligations that must be identified early.

Understanding the key strategies provides a clear starting point, but applying them effectively requires a structured way to evaluate decisions as a business evolves.

Rather than viewing each strategy in isolation, tax planning becomes more effective when these decisions are organized into a consistent framework that can be applied across different financial situations and growth stages.

While individual strategies define what actions to take, the real tax impact emerges from how these decisions interact with each other.

In practice, tax outcomes are rarely driven by a single choice; they are shaped by the relationships between structure, timing, and financial positioning.

The 3 Core Tax Planning Interactions That Drive Most Savings

Entity structure × compensation strategy

S-Corp owners split income into salary and distributions.

- Higher salary → increases payroll tax

- Lower salary → increases audit risk

The optimal balance depends on income level, IRS thresholds, and business activity.

Income timing × QBI deduction

The Section 199A QBI deduction depends on:

- taxable income thresholds

- W-2 wages

- qualified business income

Shifting income across years can preserve eligibility or eliminate it.

Depreciation × capital investment timing

A $100,000 equipment purchase:

- December purchase → immediate deduction

- January purchase → deferred tax benefit

Timing directly impacts tax liability in the current year.

These interaction patterns explain why certain decisions produce disproportionate tax outcomes.

To apply this consistently across different business situations, these interactions can be broken down into actionable levers that guide decision-making throughout the year.

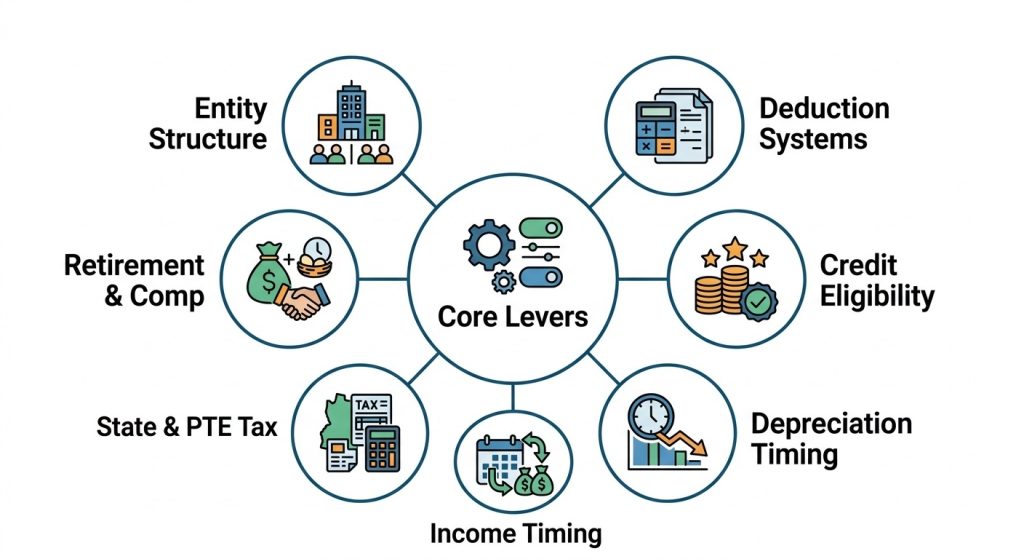

Apply 7 Core Small Business Tax Planning Levers

The 7 core tax planning levers for small businesses are:

1. Evaluate Entity Structure Decisions

This lever becomes relevant when a business reaches a point where its current structure no longer aligns with how income is generated or distributed.

Common triggers include:

- Consistent profitability,

- Onboarding investors, or

- Changes in ownership.

At this stage, evaluating different structures such as LLC, S corporation, and C corporation becomes important, especially in how profits flow to owners and how tax liability is calculated.

For a deeper comparison of structures, refer to detailed breakdowns of S Corp vs C Corp vs LLC and how pass-through entities affect taxation.

2. Structure Deduction Planning Systems

The effectiveness of deductions depends on how reliably expenses are captured and categorized during daily operations. This lever is triggered when businesses lack structured systems for tracking costs or when financial records do not support accurate classification.

Establishing processes aligned with common small business tax deductions ensures that operational expenses are consistently recorded and supported by proper documentation.

3. Plan Tax Credit Eligibility Early

This lever becomes important when a business engages in activities that may qualify for targeted incentives.

Examples include:

- Development work,

- Hiring programs, or

- Energy-related initiatives that fall under credits, such as the research and development (R&D) tax credit.

The key is identifying eligibility early enough to align operations with the documentation and compliance requirements for these credits.

4. Align Depreciation with Investment Timing

Depreciation planning is triggered when businesses make or plan significant capital investments. The decision revolves around aligning these purchases with financial cycles, particularly during periods of higher earnings, where the immediate tax impact becomes more valuable.

Methods such as Section 179 deductions and bonus depreciation influence how asset costs are recognized and can significantly affect taxable income.

5. Manage Income Timing Decisions

This lever is used when revenue patterns are uneven or when businesses anticipate shifts in financial performance.

Adjustments in billing cycles, payment timing, or recognition methods can help balance taxable income across periods.

This approach often connects with broader year-end tax planning strategies and mid-year tax adjustments to maintain better financial control.

6. Optimize State and PTE Tax Planning

This lever becomes relevant when business activity extends beyond a single jurisdiction. Growth-related events, such as hiring remote employees or expanding operations, can create a state tax nexus, triggering obligations in multiple states.

In such cases, businesses may also evaluate pass-through entity (PTE) tax elections and multi-state tax strategies to manage compliance and optimize outcomes.

These levers provide a structured way to evaluate tax decisions, but their relevance shifts depending on how a business operates.

The same strategy can produce different outcomes based on revenue model, cost structure, and operational complexity.

Adapt Tax Planning by Business Type

Business models, revenue streams, cost structure, and regulatory environment directly shape how tax strategies are applied in real-world scenarios.

Differences in operations, ownership structure, asset utilization, and market reach determine which tax planning approaches are relevant for each business type.

- Analyze Service-Based Business Tax Needs

Service-based businesses typically generate revenue through time, expertise, or client relationships rather than physical products. Because they operate with lower capital investment, tax planning decisions often revolve around income structuring, compensation models, and operational expense management.

For these businesses, variability in revenue and dependence on owner involvement are important to evaluate how income flows through the business and how expenses are aligned with service delivery.

As client volume grows or service offerings expand, tax considerations may shift toward managing profitability and maintaining consistent financial reporting.

- Analyze Product and E-commerce Tax Needs

Product and e-commerce businesses operate with inventory, logistics, and multi-channel sales, which introduce different tax considerations compared to service models.

Tax planning in this context often depends on inventory management, cost allocation, and transaction-level tracking.

As sales expand across regions or platforms, these businesses must also account for sales tax obligations and jurisdictional requirements tied to where transactions occur. Changes in fulfillment methods, supplier relationships, or pricing strategies can all influence how taxable income is calculated and reported.

- Analyze Asset-Intensive Business Tax Needs

Asset-intensive businesses – such as manufacturing, construction, or equipment-driven operations—rely heavily on physical assets to generate revenue. Tax planning here is influenced by capital investment cycles, asset utilization, and long-term cost recovery strategies.

Decisions about when to acquire, upgrade, or dispose of assets affect financial performance beyond operations. As these businesses scale, aligning investment decisions with financial periods becomes essential for maintaining predictable outcomes.

- Analyze Startup and High-Growth Tax Needs

High-growth and startup businesses operate in conditions of rapid change, where funding, hiring, and expansion decisions happen quickly.

Tax planning in this environment is shaped by scalability, funding structures, and evolving ownership models.

These businesses often move through multiple stages, from early development to revenue generation, each with different financial characteristics.

As a result, tax considerations must adapt to changing priorities, including managing growth, maintaining flexibility, and preparing for future transitions.

- Analyze Professional Practice Tax Needs

Professional practices such as healthcare providers, legal firms, and consulting businesses combine service delivery with regulatory and operational requirements.

Tax planning in these environments depends on practice structure, partner arrangements, and compensation design.

As these practices grow, additional considerations emerge around staffing models, profit-sharing structures, and compliance obligations. Aligning tax decisions with both operational workflows and professional requirements becomes a key factor in maintaining efficiency.

Business type determines how tax strategies are applied, but lifecycle stage determines when they become necessary. As a business evolves, the priority and impact of each decision change significantly.

How Tax Strategy Changes Across the Business Lifecycle?

1. Formation Stage – Set the Tax Structure Early

Focus: Entity selection and initial IRS compliance

- Choosing between sole proprietorship, partnership, LLC, or S corporation determines how income is taxed (pass-through vs corporate taxation) and what forms you must file with the IRS.

- Early elections—like S-Corp status (Form 2553)—and proper EIN setup affect self-employment taxes, liability protection, and long-term flexibility.

2. Revenue Growth Stage – Manage How Profits Are Taxed

Focus: Compensation planning and income structuring

- As profits grow, business owners can split income between salary and distributions (especially in S-Corps) to reduce self-employment tax exposure.

- Timing income and expenses—such as deferring revenue or accelerating deductions—helps control taxable income across tax years.

3. Hiring Stage – Expand Payroll and Tax Obligations

Focus: Employment taxes and benefit structuring

- Hiring employees introduces federal payroll taxes (Social Security, Medicare, FUTA) and state-level obligations, along with regular IRS filings (Forms 941, W-2).

- Structuring benefits like health insurance, retirement contributions (401(k)), and reimbursements can create tax advantages for both employer and employees.

4. Expansion Stage – Navigate Multi-State Tax Exposure

Focus: State nexus and multi-state compliance

- Expanding into new states creates “nexus,” triggering state income tax, sales tax collection, and additional filings.

- Businesses must track where they have economic or physical presence and allocate income properly across states to avoid penalties.

5. Exit Stage – Plan for Capital Gains and Transfer Strategy

Focus: Exit structuring and tax efficiency

- Selling a business involves deciding between an asset sale or stock sale, each with different federal tax implications.

- Planning helps reduce capital gains taxes through strategies like Qualified Small Business Stock (QSBS) exclusions or installment sales.

Lifecycle Insight – Timing vs. Structural Impact

- Each stage defines when tax decisions matter, but outcomes depend on how income, entities, and transactions are structured.

- This reflects a broader principle: tax results are shaped by decision frameworks and relationships, not just timing.

Industry Layer – Why Tax Strategy Varies by Sector

- Different industries trigger different tax treatments and opportunities under U.S. tax law.

- For example, real estate benefits from depreciation and 1031 exchanges, while tech startups rely more on R&D tax credits and equity compensation planning.

➡ ️ Industry context changes deductions, credits, and compliance requirements—so tax strategy must be tailored to the business model, not applied uniformly.

Use Industry-Specific Tax Planning Strategies

Different industries are influenced by specific tax variables that change how planning decisions are applied.

The following guides highlight what actually drives tax outcomes in each industry.

1. Startup tax planning strategies

Startup tax planning is driven by equity ownership, founder dilution, early-stage losses, and future exit outcomes.

Decisions around stock structure, funding rounds, and long-term capital gains treatment shape how tax strategies are evaluated from the beginning.

2. SaaS tax planning strategies

SaaS tax planning is influenced by subscription-based revenue recognition, software development cost treatment, and cross-state customer distribution.

These factors determine how revenue is reported and how operational costs are classified over time. These concepts are explored further in the SaaS tax planning strategies guide, with a focus on scaling subscription-based businesses.

3. Healthcare tax planning

Healthcare tax planning depends on provider compensation models, entity structuring for medical practices, and allocation of operational costs under regulatory constraints. These variables directly impact how income is distributed and reported

4. Real estate tax planning

Real estate tax planning is shaped by property depreciation schedules, capital gains treatment, and asset holding structures. Long-term ownership and transaction timing play a key role in determining financial outcomes. These factors are explained in more detail in this resource on real estate tax planning, particularly around asset lifecycle decisions.

5. E-commerce tax planning

E-commerce tax planning is driven by sales tax nexus, inventory movement across locations, and marketplace platform reporting requirements. These variables influence compliance obligations and transaction-level tax treatment.

A more detailed explanation is available in this guide one-commerce tax planning with AI, which addresses multi-channel operations and tax complexity.

6. Law firm tax strategy

Law firm tax strategy is influenced by partner compensation structures, profit-sharing arrangements, and entity election decisions.

These elements determine how income is allocated and taxed among partners. These topics are covered in depth in the AI tax strategy for law firms guide, where partnership structures are analyzed in context, so feel free to read that and explore the industry in detail.

7. Nonprofit tax compliance

Nonprofit tax planning focuses on maintaining tax-exempt status, Form 990 reporting requirements, and the use of restricted versus unrestricted funds. Compliance and transparency are the primary drivers of tax-related decisions. For a structured overview of these obligations, refer to this guide on nonprofit tax compliance, which breaks down reporting and governance requirements.

While industry factors shape what decisions are relevant, consistency in execution determines whether those decisions actually deliver results.

This is where tax planning shifts from isolated actions to a repeatable workflow.

Tax Planning as a Workflow, Not a Checklist

Tax planning follows a sequence, not a list

Effective tax planning operates as a workflow system:

- Identify financial activity

- Model tax scenarios

- evaluate outcomes

- apply decision before execution

Most businesses reverse this sequence.

IRS form-level interaction

Tax planning decisions flow through forms:

- Form 1120S → K-1 → Form 1040

- impacts QBI deduction

- affects estimated tax payments

Understanding how decisions appear across forms ensures accuracy and optimization.

Scenario-based planning replaces static advice

Example:

| Scenario | Outcome |

|---|---|

| High salary | higher payroll tax |

| Balanced salary | optimal QBI + compliance |

| Low salary | audit risk |

Planning requires comparing outcomes before execution.

Revisit Small Business Tax Strategy at Key Stages

Key business events, such as revenue shifts, hiring changes, multi-state expansion, capital investments, and ownership transitions, signal when tax planning decisions need to be reassessed.

Let’s look at them in detail:

1. Evaluate Tax Strategy at Business Formation

Tax planning should begin at the point where a business is legally created.

- Early decisions around

- Ownership structure,

- Registration, and

- Financial setup, establish how income will be reported and how obligations will be handled going forward.

Making informed decisions at this stage reduces the need for corrective changes later.

2. Reassess Tax Strategy When Revenue Grows

As a business moves from inconsistent earnings to predictable revenue, financial patterns become clearer.

This is where earlier assumptions should be re-evaluated, especially if profitability introduces new considerations around how income is managed and distributed.

3. Adjust Tax Strategy When Hiring Starts

Bringing on team members introduces new layers of payroll obligations, benefits considerations, and reporting requirements.

This shift changes how expenses are structured and how compensation is handled, making it an important point to reassess existing tax approaches.

4. Reevaluate Tax Strategy During Expansion

Operating beyond a single jurisdiction creates additional compliance responsibilities. Activities such as

- Hiring remotely,

- Selling in new markets, or

- Opening locations can trigger obligations that did not previously exist.

Recognizing these changes early helps avoid gaps in compliance.

5. Plan Tax Impact Before Equipment Purchases

Large purchases—such as equipment, infrastructure, or technology have implications that extend beyond operational use. These decisions influence how costs are recognized and how financial outcomes are distributed across reporting periods, making pre-planning essential.

6. Review Tax Strategy Before Year-End

The period leading up to year-end is one of the most critical checkpoints for tax planning. At this stage, businesses can still adjust financial decisions, review performance, and align outcomes before reporting is finalized. This is often the last opportunity to make meaningful adjustments within the current cycle.

7. Reassess Tax Strategy Before Major Transitions

Events such as ownership changes, restructuring, funding rounds, or preparing for a sale introduce new financial dynamics. These transitions often require a full reassessment of existing tax strategies to ensure they remain aligned with the new direction of the business.

Recognizing when to revisit tax planning helps prevent missed opportunities, but avoiding common mistakes is equally important for maintaining long-term efficiency.

Avoid 6 Common Small Business Tax Planning Mistakes

The following common small business tax planning mistakes are crucial to avoid:

Mistake #1 – Avoid Year-End-Only Tax Planning

Many businesses approach tax planning only during filing season, which limits their ability to influence outcomes.

When decisions are made too late, options become restricted, and opportunities to adjust financial direction are no longer available. Treating tax planning as an ongoing process allows businesses to respond to changes as they happen.

Mistake #2 – Choosing the wrong entity tax structure for the current stage

A structure that works in the early phase of a business may not remain effective as operations grow.

Failing to reassess this can lead to inefficiencies in how income is handled or distributed. Regular evaluation ensures that the structure continues to align with current financial patterns and business direction.

Mistake #3 Missing tax deductions due to poor documentation

Even when expenses are valid, they may not be usable if they are not properly recorded or supported.

Inconsistent tracking systems, incomplete records, or unclear categorization can lead to missed opportunities and increased risk during audits. Strong documentation practices are essential for maintaining accuracy.

Mistake #4 Overlooking eligibility for tax credits

Some businesses fail to identify activities that could qualify for targeted incentives because they are not evaluated in advance.

Without proper planning and documentation, these opportunities can be missed entirely. Early assessment ensures that eligibility criteria are met as part of regular operations.

Mistake #5– Ignoring state and multi-state tax obligations

As businesses expand, they may unknowingly trigger additional compliance requirements across jurisdictions.

Failing to recognize these changes can result in penalties or reporting gaps. Monitoring where and how business activity occurs helps maintain compliance.

Mistake #6– Applying generic tax strategies without considering the business type

Using broad, one-size-fits-all approaches can lead to ineffective outcomes.

Tax planning decisions should reflect how the business operates, including its revenue model, cost structure, and operational setup. Tailoring strategies improves accuracy and relevance.

Avoiding these common mistakes improves consistency, but effective tax planning also depends on how efficiently decisions are analyzed and implemented.

In addition to these SME tax filing blunders, we suggest reviewing Year-end Tax Research Mistakes to ensure you remain compliant.

The next section explores how modern tools are changing the way tax planning is approached.

Use AI to Improve Small Business Tax Planning

Top AI-powered tax tools empower CPAs to streamline research, scenario modeling, and client communication. By automating complex workflows, these tools enable firms to deliver faster, data-driven, and scalable tax planning outcomes

- Find Relevant Tax Strategies Faster

CPAs often work across multiple client profiles, each with different financial situations and regulatory considerations. Identifying applicable tax strategies quickly requires scanning large volumes of tax rules, prior cases, and client data.

AI-powered systems help reduce this effort by surfacing contextually relevant tax positions based on specific inputs, allowing professionals to move from research to decision-making with less manual effort.

- Organize Tax Research and Scenarios

Tax planning frequently involves comparing multiple scenarios, such as different income treatments, structural choices, or timing variations, to evaluate potential outcomes. AI tools assist by structuring research into organized outputs, making it easier to compare alternatives, track assumptions, and maintain consistency across multiple client engagements. This improves clarity in how decisions are evaluated and documented.

- Create Clear Client Tax Recommendations

Communicating tax strategies to clients requires translating technical concepts into clear, actionable guidance. AI supports this process by helping CPAs generate structured explanations, summaries, and client-ready insights based on the analysis performed.

This reduces time spent on manual drafting while improving consistency in how recommendations are presented.

- Use CPA Pilot for Tax Planning Workflows

CPA Pilot functions as an AI tax planning assistant designed specifically for CPAs, Enrolled Agents, and U.S. tax firms, helping streamline research, analysis, and communication workflows. Instead of switching between multiple tools, professionals can use CPA Pilot to:

- Analyze tax scenarios based on client inputs

- Generate strategy recommendations aligned with tax rules

- Draft client communications and advisory insights

- Support onboarding and internal knowledge sharing

This approach aligns with the broader shift toward workflow-driven tax planning, where efficiency, accuracy, and scalability become central to how tax professionals deliver value.

It also directly addresses content gaps identified in CPA Pilot’s strategy, where practical, scenario-based workflows are essential for building deeper authority and user trust.

Build a Tax Plan That Fits Your Business Model

A well-structured tax plan is not built from isolated decisions; it is created by aligning business activity, financial data, and planning workflows into a consistent system that adapts as the business evolves.

For business owners, this means moving beyond one-time adjustments and focusing on how everyday decisions impact long-term financial outcomes. For CPAs and tax professionals, it means shifting from reactive reporting to a more structured advisory approach that integrates research, analysis, and communication into a single workflow.

The most effective tax planning approach is one that:

- Adapts to changes in revenue, operations, and business structure

- Maintains consistency in financial data and documentation

- Applies relevant strategies based on business type and industry

- Incorporates scenario analysis before major decisions are made

As tax complexity increases, relying solely on manual processes can limit both speed and accuracy. This is where CPA Pilot helps bridge the gap between strategy and execution.

If you’re looking to implement small business tax planning strategies in a more structured and scalable way, integrating the right tools into your workflow can make a measurable difference.

Book a free 30-minute demo today and find out how CPA Pilot can benefit your business!!!

Answer Small Business Tax Planning Questions

How can a small business legally reduce taxes?

A small business reduces taxes by optimizing deductions, applying eligible tax credits, structuring income efficiently, and aligning expenses with IRS-compliant planning strategies.

What are the most important tax planning strategies for small businesses?

Small business tax planning strategies include selecting the right entity structure, maximizing deductions and credits, timing income and expenses, and managing multi-state tax exposure.

When should a small business start tax planning?

A small business should start tax planning at formation and continue year-round as revenue, hiring, expansion, or major financial decisions occur.

How does business structure affect taxes?

Business structure determines how income is taxed, whether profits pass through to owners, and how self-employment and corporate taxes apply.

What tax strategies matter most for growing businesses?

Growing businesses benefit from strategies focused on income management, capital investment timing, state tax planning, and scalable financial structuring.

Disclaimer: This article is provided by CPA Pilot for educational purposes. While we may offer tax software/services, the information here is general and may not address your specific facts and circumstances. It does not constitute individual tax, legal, or accounting advice. U.S. federal and State Tax laws change frequently; please consult a qualified tax professional before acting on any information.

![Restaurant Tax Planning After OBBBA [2026]- FICA Tip and R&D Credits](https://www.cpapilot.com/blog/wp-content/uploads/2026/04/Restaurant-Tax-Planning-After-OBBBA-.png)