Restaurant Tax Planning After OBBBA [2026]- FICA Tip and R&D Credits - CPA Pilot

Industry Tax Planning

Restaurant Tax Planning After OBBBA [2026]- FICA Tip and R&D Credits

CPA Pilot

Apr 20, 2026·15 min read

Restaurant tax planning is the process of structuring a restaurant client’s payroll, depreciation, credits, and meal-related deductions to capture industry-specific tax breaks. The most important provisions for restaurants are IRC §45B (FICA tip credit), §41 (R&D credit), §168(k) (bonus depreciation), §163(j) (business interest limitation), and §274(n)(meal deductibility).

TL;DR: Key Restaurant Tax Planning Changes After OBBBA for CPAs

Restaurant tax planning in 2026 focuses on a few high-value tax strategies.

The §45B FICA tip credit remains the biggest opportunity for many restaurant clients.

OBBBA made 100% bonus depreciation permanent for qualifying property.

OBBBA also restored an EBITDA-based §163(j) calculation, which can increase deductible business interest.

Restaurants may qualify for R&D credits when they test recipes, improve cooking methods, or refine kitchen processes.

Meal deduction rules remain limited, so CPAs should update restaurant clients on current B2B catering guidance.

CPAs who apply these rules correctly can uncover larger savings and deliver stronger advisory value.

For CPAs, this matters because the real value is in year-round planning, not just year-end filing. The FICA tip credit alone can save a mid-size restaurant group $40,000 to $80,000 annually, and the 2025 One Big Beautiful Bill Act (OBBBA) adds even more opportunity through permanent 100% bonus depreciation under §168(k) and an EBITDA-based reversion for the §163(j) interest limitation.

Restaurant clients generate some of the most labor-intensive returns in any CPA’s practice. Most of the value isn’t in the return itself; it’s in the planning before year-end. If you’re filing restaurant returns without running the §45B FICA tip credit calculation on Form 8846, you’re doing compliance, not advisory.

Here’s what’s actually moving the needle for restaurant clients in 2026: the FICA tip credit, OBBBA’s permanent 100% bonus depreciation, the EBITDA reversion for §163(j), R&D credits for menu development, and updated meal deductibility rules under §274(n).

This guide walks through the mechanics of these credits and deductions, the common mistakes CPAs make, and a practical 2026 action list for your restaurant clients.

How the FICA Tip Credit Works for Restaurants

The FICA tip credit is the single largest dollar-for-dollar credit available to most restaurant operators, yet a surprising number of CPAs either skip it entirely or calculate it incorrectly.

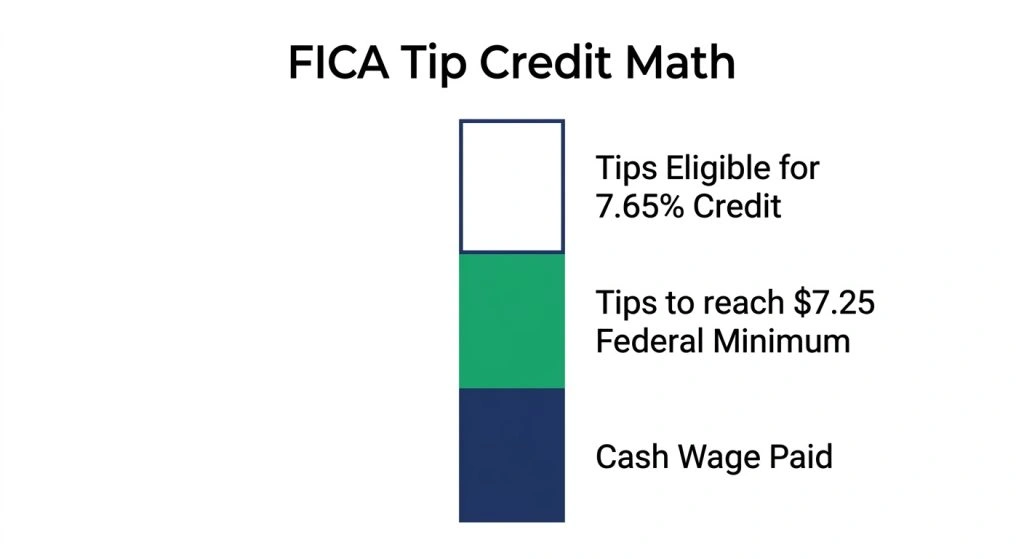

The §45B credit is calculated on tips that exceed the amount needed to reach the $7.25 federal minimum wage.

Under IRC §45B, an employer receives a general business credit equal to the employer’s share of FICA taxes (7.65%) paid on tips that exceed the amount needed to bring an employee’s cash wage to the federal minimum wage of $7.25 per hour. The credit applies only to tips received from customers for food or beverage service. Tips on delivery fees, employer-controlled service charges, or non-food/beverage items do not qualify. The credit is claimed on Form 8846 and flows to Form 3800 as a general business credit

The math isn’t complicated, but the data collection is. Here’s what it looks like for a single tipped employee:

Component

Amount

Hours worked in the year

2,000

Cash wage paid by the employer

$2.13/hr ($4,260 total)

Tips reported by the employee

$38,000

Wages needed to reach $7.25/hr

$7.25 x 2,000 = $14,500

Tips used to meet minimum wage

$14,500 – $4,260 = $10,240

Tips eligible for credit

$38,000 – $10,240 = $27,760

FICA tip credit (7.65%)

$2,124

Multiply that across 15 tipped employees, and you’re looking at a credit north of $30,000. For a restaurant group with 60 tipped servers across four locations, credits can hit $135,000.

A few things practitioners get wrong:

The minimum wage offset. You only credit FICA on tips above the amount that brings the employee to $7.25/hr. If your client pays the full minimum wage (some states require this — California, Washington, Oregon), the entire tip amount is eligible. No offset. That actually makes the credit larger in states with no tip credit against minimum wage.

State minimum wage vs. federal. The §45B calculation uses the federal minimum wage of $7.25, not the state minimum. This confuses people. Even if your client is in a state with a $16.28 minimum wage, the credit computation uses $7.25. The IRS confirmed this in the instructions to Form 8846. The “minimum wage” referenced in §45B(b)(2) is the rate under Section 6(a)(1) of the Fair Labor Standards Act.

Interaction with the payroll tax deduction. Here’s the catch: §45B(c) requires reducing the FICA deduction by the credit amount. You’re not double-dipping. The credit replaces a deduction. For a restaurant at 21% (C-Corp) or up to 37% (pass-through), the credit still beats the deduction. On a $30,000 credit, the lost deduction costs $6,300 at 21%. Net benefit: $23,700.

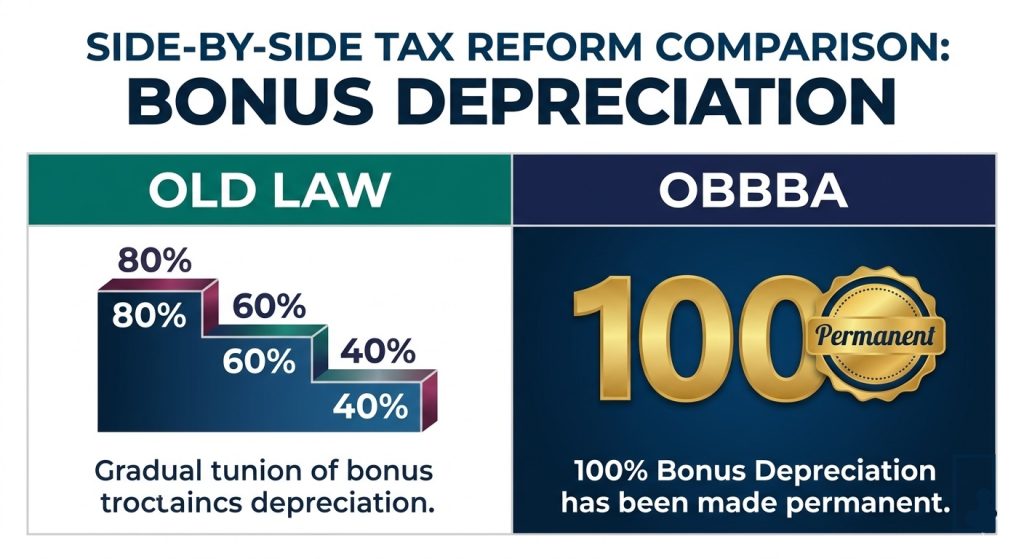

Key OBBBA Tax Changes for Restaurants: Bonus Depreciation and §163(j)

The One Big Beautiful Bill Act (OBBBA), enacted in July 2025, delivers two major tax changes that directly impact restaurant operators: permanent 100% bonus depreciation under IRC §168(k)(confirmed by IRS Notice 2026-11) and a reversion to EBITDA-based computation for the business interest limitation under IRC §163(j)

OBBBA stabilized the tax landscape by making 100% bonus depreciation permanent for qualified property.

1. Permanent 100% Bonus Depreciation

Before OBBBA, bonus depreciation was scheduled to phase down to 40% in 2026 and eventually expire. OBBBA made 100% bonus depreciation permanent for qualified property acquired after January 19, 2025, and placed in service in tax years beginning after December 31, 2024. For an industry that spends heavily on kitchen equipment, qualified improvement property (QIP), and tenant buildouts, this is transformative. A typical full-service restaurant buildout runs $400,000 to $1.2 million in qualifying improvements, all of which can now be fully expensed in Year 1 under the 100% bonus depreciation rule.

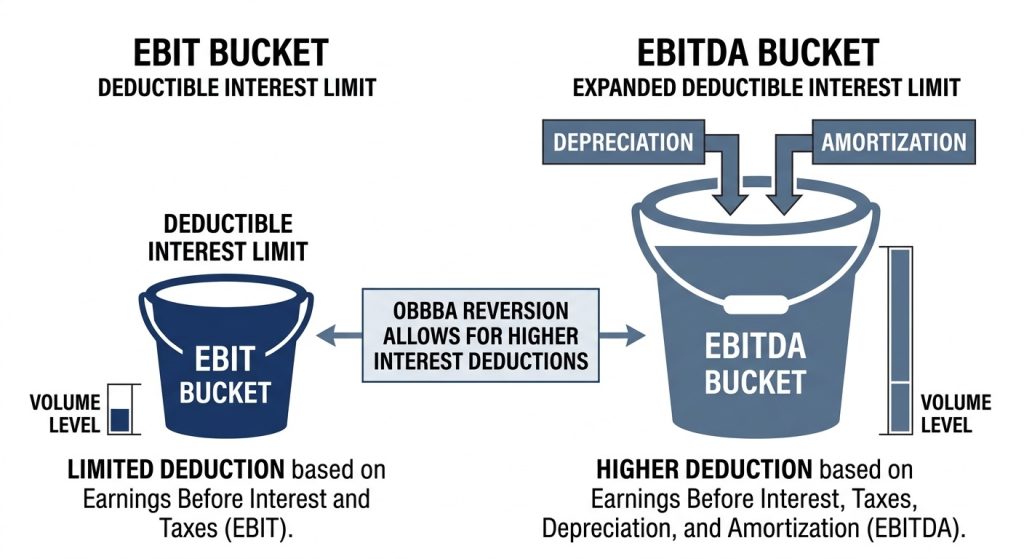

2. §163(j) Reverts to EBITDA-Based Limitation

: The reversion to EBITDA increases the ‘Adjusted Taxable Income’ bucket, allowing for more interest to be deducted currently.

The more impactful (and less obvious) change is to §163(j). OBBBA reset the Adjusted Taxable Income (ATI) computation to add back depreciation, amortization, and depletion, effectively reverting to the pre-2022 EBITDA-based calculation.

Example: One restaurant client carried $2.8 million in debt on a ground-up buildout with $196,000 in annual interest. Under the post-2021 EBIT-based §163(j) limitation, they were capped at a $140,000 deductible, with the remaining $56,000 carried forward. With OBBBA reverting to EBITDA, the full $196,000 becomes deductible in the current year. That's $56,000 more in deductions—roughly $11,760 in tax savings at 21%.

What OBBBA Did Not Change: Meal Deductibility Rules

OBBBA did not restore the 100% meal deductibility that existed under the Consolidated Appropriations Act of 2021 for 2021–2022 business meals. Business meals are back to the standard 50% deduction under IRC §274(n).

This matters for your restaurant clients who cater corporate events or sell B2B catering packages.

Their corporate customers can deduct 50% of the meal cost (unless it’s a holiday party or company-wide event), which remains 100% deductible under §274(e)(4). Don’t let clients price their corporate catering based on outdated 100% deduction assumptions, as it affects demand and pricing strategy.

R&D Tax Credits for Restaurants: What Menu and Process Work Qualifies

Bringing up R&D tax credits with restaurant clients often gets blank stares at first, but when the owner starts listing things they’ve experimented with (new recipes, cooking methods, equipment tweaks), that’s when CPAs should start taking notes.

The R&D credit under IRC §41 doesn’t care what industry you’re in. The four-part test under Reg. §1.41-4 asks whether an activity:

Develops a new or improved business component,

Is technological in nature,

Involves uncertainty, and

Involves a process of experimentation.

Food science, menu development, and kitchen process engineering can absolutely qualify.

Restaurant R&D Activities That Commonly Qualify

Proprietary cooking process: A fast-casual chain developed a consistent cooking method for uniform quality across 12 locations. They spent 8 months testing temperature profiles and equipment settings. Qualifying wages: $85,000. Credit (Alternative Simplified Credit): ~$7,400.

Allergen-free recipe reformulation: A restaurant group reformulated recipes to eliminate specific allergens without changing taste, requiring systematic testing of substitute ingredients and documentation of failed approaches. This satisfies the “process of experimentation” prong. Qualifying expenses: $42,000. Credit: ~$4,200.

Commissary HVAC redesign: A commissary kitchen designed a modified HVAC system to meet new emissions standards while maintaining output. Engineering, testing, and redesign totaled $120,000 in qualifying expenditures.

The credit typically won’t reach six figures for most single-location restaurants. But for multi-unit operators with a test kitchen, significant menu development, or commissary engineering, it can generate $15,000–$50,000+ annually.

Keep detailed records: Test logs, failed experiments, ingredient substitution data, temperature profiles, and engineering notes.

OBBBA Restored Immediate Expensing Under §174A

OBBBA fixed the §174 issue. IRC §174A (Section 70302 of P.L. 119-21) restored immediate expensing for domestic research and experimental (R&E) expenditures after December 31, 2024.

Restaurant clients can now deduct R&D expenses immediately AND claim the §41 credit separately, no need to capitalize and amortize.

For 2022–2024 amounts previously capitalized (under the TCJA amortization requirement), Rev. Proc. 2025-28 provides transition relief and guidance on how to handle prior-year capitalization. Track the credit and deduction separately on your client’s return.

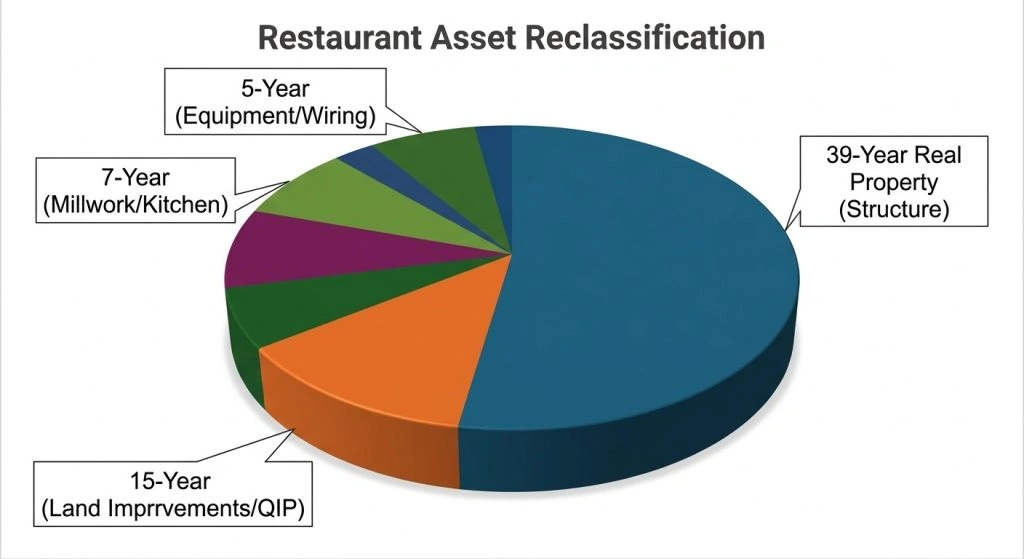

With OBBBA’s permanent 100% bonus depreciation under IRC §168(k) confirmed by IRS Notice 2026-11 for property acquired after January 19, 2025, QIP gets first-year expensing. So why bother with a cost segregation study?

For owned buildings (39-year property): Cost segregation reclassifies 20–40% (typically 35–45%) into 5-year, 7-year, and 15-year assets under IRC §168

For state decoupling: Some states don’t conform to federal bonus depreciation rules

For prior-year buildouts: File Form 3115 for catch-up via IRC §481(a) adjustment

For non-QIP components: Kitchen equipment, wiring, HVAC may be 5- or 7-year property under IRC §1245

Assets Commonly Reclassified in a Restaurant Cost Segregation Study

If your client did a buildout in a prior year without a cost segregation study, you can still claim the accelerated depreciation by filing

Form 3115 (Application for Change in Accounting Method). The catch-up depreciation comes as an IRC §481(a) adjustment in the current year—no amended returns needed.

Firms have successfully run this with catch-up deductions ranging from $90,000 to $310,000 for prior-year buildouts, capturing missed bonus depreciation and reclassified component lives.

Meal Deductibility Rules for Restaurant Clients and Their B2B Customers

Your restaurant clients will ask about meal deductibility rules; it doesn’t affect their own tax return directly (since they sell meals, not consume them as employers), but it affects their corporate catering and B2B sales.

Their corporate customers need to know what they can deduct when ordering catering or hosting client meals at your client’s restaurant.

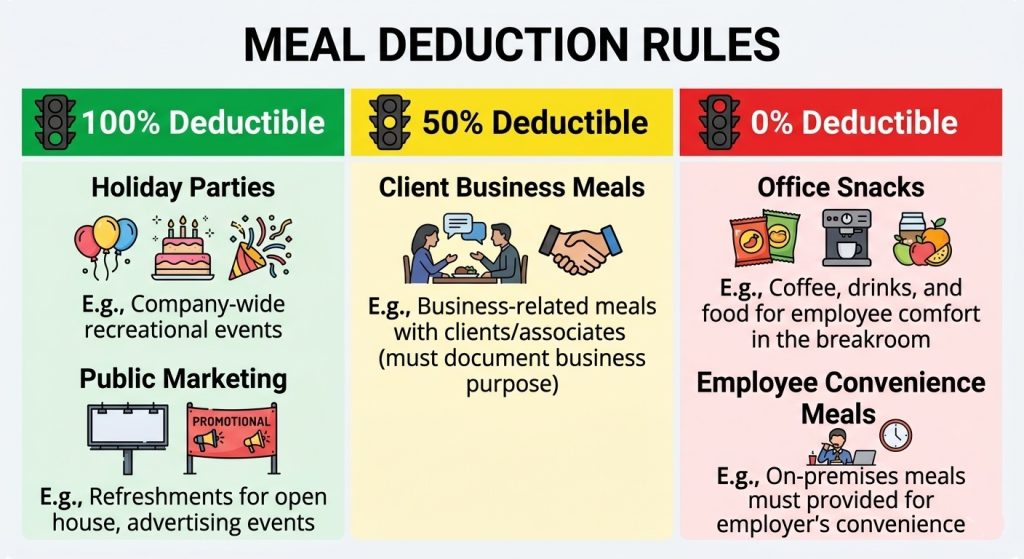

Current Meal Deductibility Rules for Corporate Customers in 2026

Understanding the shift in meal deductibility is key for advising B2B catering clients.

Under IRC §274(n) and new §274(o) (effective 2026), the deduction limits for business meal expenses are:

Type of Expense

Deductible Percentage

Requirements

Business meals with a client or associate

50% deductible

Clear business purpose required; substantiation of time, place, and business purpose needed

Office snacks and breakroom meals

0% deductible (post-2025)

Employer-provided, not taxed as compensation

Meals for employee convenience (on-premises, not taxed to employee)

Starting in 2026, OBBBA modified IRC §274(o) so employer-provided on-premises meals are no longer deductible (0%), unless taxed as compensation

Business meals remain 50% deductible under §274(n) with proper substantiation (amount, date, location, business purpose, participants).jupid+1

Why Meal Deductibility Changes Matter for Restaurant Clients

Don’t let your clients price their corporate catering packages based on outdated 100% deduction assumptions. Their corporate B2B customers can now only deduct:

50% of client meals and business-meeting catering (requires business purpose + documentation)

0% of office snacks or breakroom catering (unless converted to taxable compensation)

100% of holiday parties, company-wide events, and employee recreation (Q4 season)

This affects pricing strategy, demand forecasting, and sales messaging. Corporate buyers may scale back on regular lunch catering (50% deductible) but increase Q4 holiday party spending (100% deductible).uhy-us+1

What CPAs Should Tell Restaurant Clients

Educate corporate customers on what’s deductible—don’t let them overpay for catering, expecting 100% write-offs

Promote Q4 holiday party packages—the 100% deductibility under §274(e)(4) is a strong sales driver

Reframe office snacks as “employee compensation” if they want 100% deductibility (but must be taxed as income).

Update marketing materials to reflect correct deduction rates—accuracy builds credibility with B2B customers.

Track meal types separately in their own books—§274 requires proper categorization for audits.

Restaurant Tax Planning Checklist for CPAs

For your restaurant clients, the priority list looks like this:

Pull payroll data and run the §45B FICA tip credit for every open year. If you haven’t been filing Form 8846, you can amend back three years. For a 25-server restaurant, that’s potentially $60,000-$90,000 in refunds across three years.

Revisit the §163(j) interest limitation. If your client was carrying forward a disallowed business interest, the OBBBA EBITDA reversion may free it up. Check the carry-forward schedule.

Screen for R&D credits — especially multi-unit operators and commissary kitchens. The credit is real and defensible if documented properly.

Get a cost seg study on any owned building or significant buildout. If it was done in a prior year without a study, file Form 3115 and pick up the catch-up.

Common Restaurant Tax Mistakes CPAs Should Avoid

Not filing Form 8846 at all, or calculating §45B using the state minimum wage instead of $7.25

Forgetting the §45B(c) deduction offset and overstating the net benefit

Missing the §163(j) EBITDA reversion and leaving interest carryforwards on the table

Assuming R&D credits don’t apply to food service

Defaulting restaurant buildouts to straight 15-year QIP without a cost seg study on owned buildings

Conclusion – Turn Restaurant Tax Complexity Into Advisory Value

Restaurant tax planning is no longer just about filing returns; it’s about capturing industry-specific savings that most CPAs miss. From the FICA tip credit to OBBBA’s permanent bonus depreciation, the difference between a compliant return and a transformative advisory engagement comes down to precision, speed, and the right research tools.

Stop spending hours digging through IRC sections, IRS notices, and fragmented guidance. Start delivering confident, defensible advice in minutes.

🚀 Try CPA Pilot Free Today and discover how AI-powered tax research is transforming CPA workflows:

Instant IRC & Reg citations for FICA tip credits (§45B), R&D qualifications (§41), and OBBBA changes (§168(k), §163(j), §174A)

Pre-built research memos on restaurant-specific tax provisions—no more starting from scratch

Smart workflows that cut research time by 50%+, letting you focus on high-value advisory instead of compliance drudgery

Confidence at your fingertips with authoritative, up-to-date guidance that stands up to audits

Join thousands of forward-thinking CPAs who are already using CPA Pilot to educate clients faster, uncover hidden savings, and grow their practice with premium advisory services. Book a 30-Minute Demo Today!!!

Your next restaurant client is waiting for advice that only you can provide. Don’t let research bottlenecks hold you back.

Restaurant Tax Planning FAQs

How is the FICA tip credit calculated under IRC §45B?

Credit = 7.65% × tips exceeding the amount to reach $7.25/hr (federal min). File Form 8846; credit flows to Form 3800. Reduce FICA deduction per §45B(c).

What did OBBBA change for restaurants?

OBBBA made 100% bonus depreciation (§168(k)) permanent for property acquired after Jan 19, 2025; reverted §163(j) to EBITDA-based ATI (more interest deductible); didn’t restore 100% meals but created §174A for immediate R&E expensing in 2025+.

Can a restaurant really claim R&D tax credits?

Yes, if activity meets Reg. §1.41-4 four-part test (new/improved component, technological, uncertainty, experimentation). Menu development, cooking processes, and commissary engineering qualify. File Form 6765; document each.

Are business meals still 50% deductible in 2026?

Yes. IRC §274(n) limits ordinary business meals to 50% (business purpose + substantiation required). 100% deduction (2021–2022) expired; not renewed by OBBBA. Holiday parties remain 100% deductible under §274(e)(4).

Is cost segregation still worth it with 100% bonus depreciation?

Yes, for owned buildings (39-year property). Reclassify 20–35% into 5/7/15-year assets for six-figure deductions. Critical in decoupled states. Use Form 3115 (§481(a) adjustment) for prior-year catch-up.

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.

![Cryptocurrency Tax Reporting for CPAs: Forms, Rules & Client Strategies [2026]](/_next/image/?url=%2Fuploads%2Fcryptocurrency-tax-reporting-90cf8385.webp&w=3840&q=75)