New Jersey Business Tax Planning for CPAs: CBT, BAIT & Corporate Transit Fee - CPA Pilot

Multistate Tax Planning

New Jersey Business Tax Planning for CPAs: CBT, BAIT & Corporate Transit Fee

CPA Pilot

May 28, 2026·16 min read

TL;DR – New Jersey Tax Planning

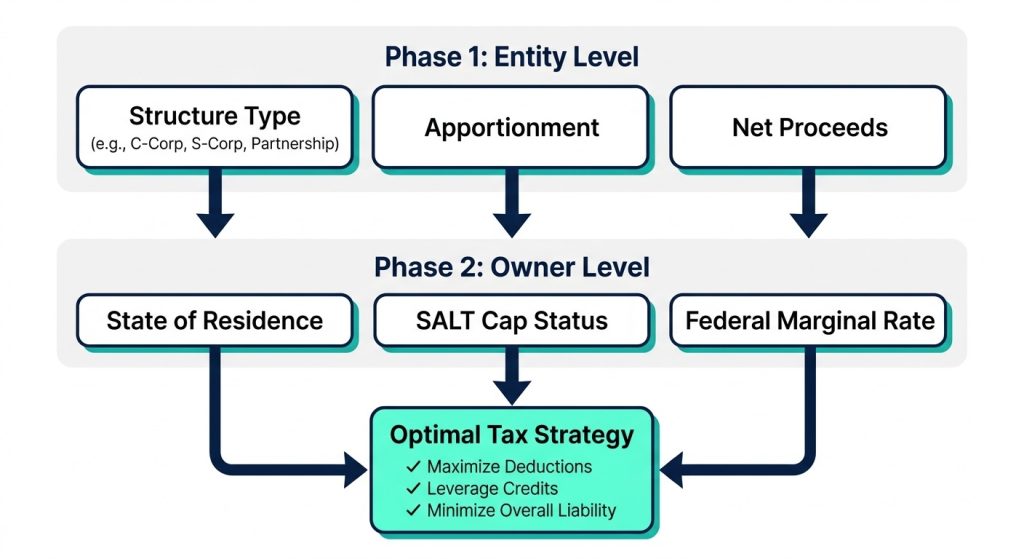

New Jersey tax planning demands a dual-layered approach, requiring concurrent analysis at both the corporate/entity level and the individual owner level to determine true tax outcomes.

A 2.5% Corporate Transit Fee (CTF) is levied on C corporations or combined groups whose allocated taxable net income exceeds $10 million, creating a peak potential rate of 11.5%.

Under combined reporting rules, related entities that fall below the $10 million CTF threshold individually can still trigger the 2.5% fee if their aggregated group income exceeds the limit.

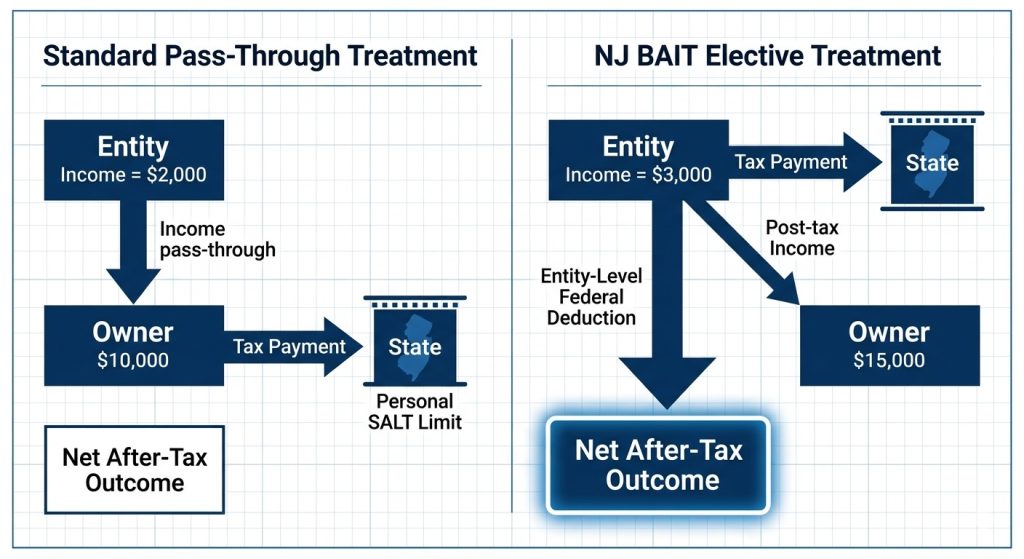

The Business Alternative Income Tax (BAIT) is an elective mechanism enabling pass-through entities to pay tax at the entity level, yielding a federal deduction and a corresponding state credit for owners.

New Jersey’s BAIT rates are graduated and top out at 10.9% for income exceeding $1 million, meaning a higher entity-level tax calculation does not automatically yield net individual savings.

Comprehensive pre-election modeling must account for unique owner variables, including state residency, federal marginal tax brackets, cash flow constraints, and individual SALT limitation positions.

Common pitfalls in BAIT implementation include failing to meet strict quarterly estimated payment timelines, credit tracing complications in multi-tier partnerships, and mismatched out-of-state resident credits.

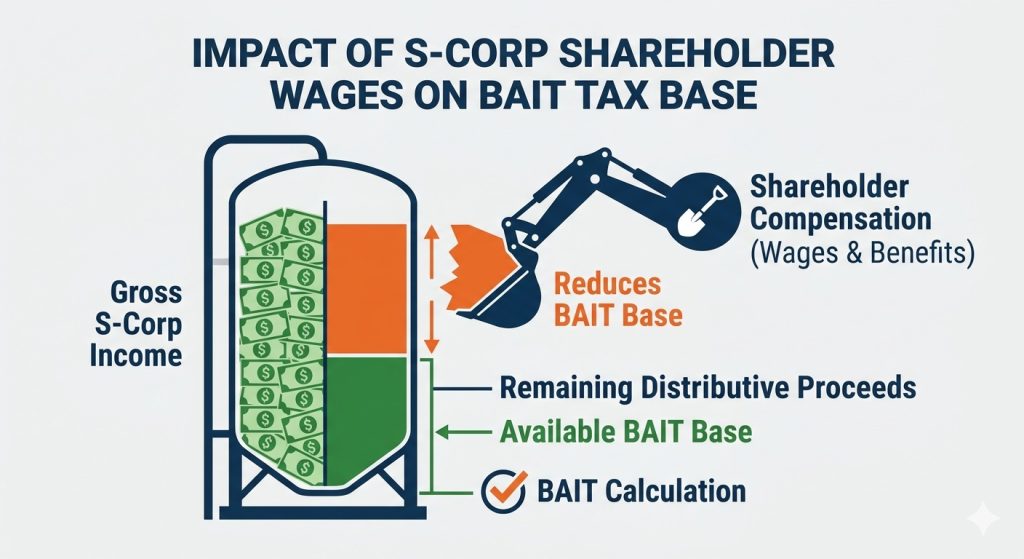

Shareholder compensation strategies must be synchronized with BAIT planning, as S corporation wages reduce the overall pass-through distributive proceeds base.

Transitioning tax planning from reactive springtime preparation to proactive third-quarter forecasting—leveraging tools like AI tax assistants—is critical for managing multi-owner state tax complexities.

New Jersey business tax planning requires more than applying federal rules and preparing the return. CPAs must review state-specific entity taxes, pass-through elections, owner residency, combined reporting, and payment timing before client choices become harder to adjust.

C corporations: New Jersey uses a graduated CBT structure: 6.5% for the entire net income up to $50,000; 7.5% for $50,001 to $100,000; and 9.0% for income over $100,000. (Source)

Larger C corporations: The 2.5% Corporate Transit Fee applies when allocated taxable net income exceeds $10 million. (Source)

Pass-through entities: BAIT may shift tax to the entity level, create a federal deduction, and give owners a New Jersey credit. (Source)

The practical point: New Jersey tax planning should not be reviewed only at the entity level or only at the owner level. The result depends on both.

Let’s discuss this in detail:

How New Jersey CBT and the Corporate Transit Fee Affect Business Clients

New Jersey’s Corporate Business Tax applies to corporations with New Jersey activity. The rate structure creates different outcomes depending on income level, apportionment, credits, and combined reporting status.

New Jersey CBT Rates for C Corporations

Entire Net Income / Allocated Taxable Net Income

CBT Rate

CTF

Potential Combined Rate

Up to $50,000

6.5%

—

6.5%

$50,001 to $100,000

7.5%

—

7.5%

Over $100,000

9.0%

—

9.0%

Over $10 million allocated taxable net income

9.0%

2.5%

11.5%

Current New Jersey CBT rates plus CTF, where applicable. (Source)

When the New Jersey Corporate Transit Fee Applies

The Corporate Transit Fee is a separate 2.5% charge imposed in addition to regular CBT. It applies when a taxpayer or combined group has New Jersey allocated taxable net income over $10 million.

For combined groups, liability is at the group level.

Credits generally cannot be used against the Corporate Transit Fee except for payment-related credits such as installment or estimated payments with extension and prior-period overpayments.

New Jersey S corporations filing CBT-100S and public utilities are not subject to the Corporate Transit Fee, although S corporations may still have other CBT filing obligations and BAIT considerations depending on the facts.

Why the $10 Million Corporate Transit Fee Threshold Matter

Clients near the $10 million threshold face a different planning conversation, because small changes can determine whether the Corporate Transit Fee applies.

Focus on legitimate, supportable items such as deferred revenue, accrued expenses, fixed asset timing, apportionment documentation, and current projections. Avoid artificial timing changes.

For C corporations and combined groups near $10 million, review income timing, apportionment, intercompany charges, credits, and combined group projections before year-end.

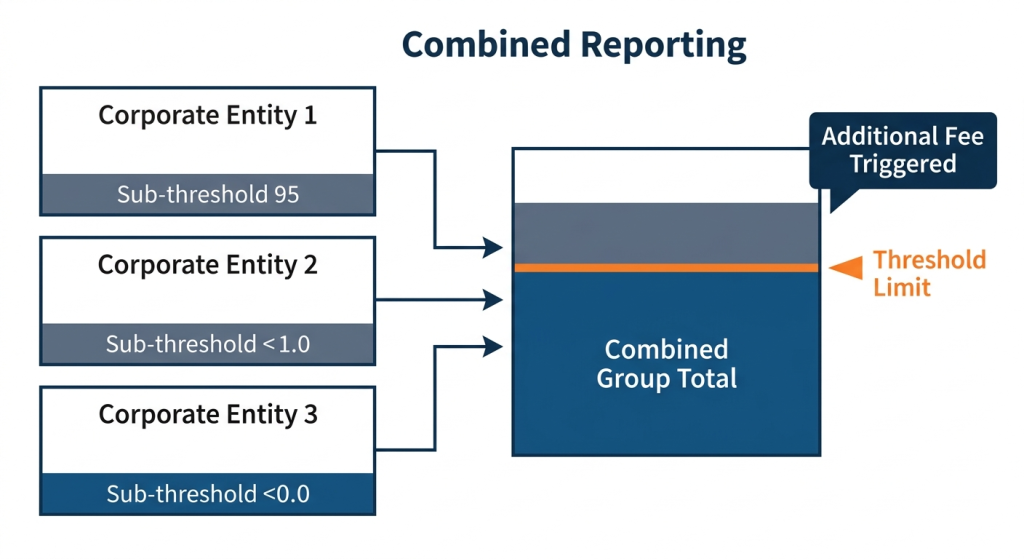

Combined Reporting and Corporate Transit Fee Exposure

Related corporations may need to be reviewed as a group. A single C corporation can appear below the $10 million CTF threshold on its own, but if it is part of a combined group whose total taxable net income exceeds $10 million, the group may be liable for the Corporate Transit Fee.

Combined reporting aggregations can inadvertently push separate low-income entities over the $10 million Corporate Transit Fee boundary.

Example: How Combined Reporting Can Trigger the Corporate Transit Fee

Combined total: $10.4 million, so the Corporate Transit Fee applies at the group level even though each entity is under $10 million.

Planning questions before year-end:

Are there related entities with New Jersey activity?

Did ownership change during the year?

Are intercompany charges documented?

Has revenue shifted between entities?

Does single sales factor apportionment change the New Jersey allocation?

Is the client close enough to $10 million to require an updated projection?

After CBT and CTF exposure is understood, move to pass-through entity planning and owner-level outcomes.

How the New Jersey BAIT Election Works for Pass-Through Entities?

BAIT is New Jersey’s elective pass-through entity tax regime. It allows eligible pass-through entities to pay tax at the entity level, and eligible owners may receive a New Jersey credit for their share of the tax paid. (Source)

The BAIT election shifts the state tax burden from the owner to the entity, potentially unlocking a larger federal deduction by bypassing individual SALT caps.

CPAs comparing entity-level elections should also review broader pass-through entity planning issues, including owner residency, deductions, credits, and payment timing.

Which New Jersey Pass-Through Entities Can Elect BAIT?

Eligible S corporations, partnerships, and LLCs classified as partnerships or S corporations for federal tax purposes, with at least one member subject to New Jersey gross income tax, may elect BAIT.

The election, payment schedule, and filing mechanics should be reviewed annually under the current PTE instructions, because the election and payment requirements are tax-year specific and can change by year.

Typical entities:

Partnerships.

Multi-member LLCs taxed as partnerships.

S corporations.

LLCs taxed as S corporations.

Multi-owner businesses with New Jersey-source income.

Single-member disregarded entities generally should not be treated as standalone electing pass-through entities.

New Jersey BAIT Tax Rates

Verify the current-year PTE instructions before filing, because the applicable rates and filing mechanics are year-specific. Under current New Jersey guidance, the BAIT tax rate is 5.675% on the first $250,000 of allocated income, 6.52% on income over $250,000 through $1 million, and 10.9% on income over $1 million.

The result still depends on distributive proceeds, owner shares, resident-state treatment, estimated payments, and credit mechanics, so a higher entity-level tax does not automatically mean a better overall outcome.

BAIT Planning for Partnerships vs. S Corporations

Shareholder compensation decisions directly reduce the net income available for the New Jersey BAIT base.

S corporations: also consider shareholder wages, reasonable compensation, and pass-through income affecting the BAIT base. BAIT planning should not be a simple yes/no election.

Entity classification should be reviewed alongside S corp, C corp, and LLC tax differences, because structure can affect compensation, pass-through income, and state-level planning.

What CPAs Should Model Before Making a BAIT Election

A reliable state tax recommendation requires mapping high-level business entity classifications down to individual owner tax profiles.

Entity income.

New Jersey distributive proceeds.

Owner residency.

Federal marginal tax rate.

SALT limitation position.

Owner-level New Jersey credit.

Resident-state credit availability.

Estimated payment timing.

Cash flow impact.

Differences between owners.

Document the recommendation at the member level. If the election helps one owner but not another, identify this before filing.

For projection-heavy clients, CPA firms can use AI tax projection workflows to organize income assumptions, owner credits, payment timing, and state-level outcomes before recommending BAIT.

How BAIT Affects the Federal Entity-Level Deduction

BAIT can help because the entity pays the tax at the business level, and IRS Notice 2020-75 confirms that state and local income taxes imposed on and paid by a partnership or S corporation on its income may be deductible by the entity. That can change the timing and character of the federal deduction compared with an owner-level state tax payment.

IRS Notice 2020-75 is the key federal authority supporting entity-level deduction treatment for specified state and local income taxes paid by a partnership or S corporation. Whether BAIT produces a meaningful benefit still depends on the owner’s federal tax profile, the New Jersey credit, resident-state credit rules, payment timing, and how it compares with broader SALT deduction planning.

For some high-income New Jersey owners, BAIT can still matter, but the benefit should be modeled at the owner level. Compare federal deduction benefits, state credit treatment, owner residency, and cash-flow impact before recommending it.

When the New Jersey BAIT Election May Not Create Tax Savings

The owner is not constrained by the federal SALT limitation.

The owner lives in a state that does not provide a matching credit.

Cash flow is tight.

Owners have different marginal rates or resident-state rules.

Estimated payments were missed.

Tiered ownership makes credit tracing difficult.

BAIT should not be recommended as a blanket strategy. Analysis must move from entity-level eligibility to owner-level outcome.

Common New Jersey BAIT Mistakes CPAs Should Avoid

BAIT planning fails when treated as a form choice instead of a workflow, which is why firms need time-saving tax workflows for CPAs when multiple owners, estimates, and credit schedules must be reviewed.

Common problems: payment timing, owner residency, tiered ownership, and uneven member-level benefits.

Mistake #1 – Missed BAIT Estimated Payments

Under the current PTE instructions, estimated payments are generally due on or before April 15, June 15, September 15, and January 15 for calendar-year filers. Verify the current-year due dates before filing, because filing and payment deadlines can change by tax year.

CPA workflow should identify:

Who makes the payment?

The bank account used.

The entity’s cash availability.

The bookkeeper’s payment schedule.

Owner-level estimate adjustments.

Mistake #2 –Nonresident Owner Credit Issues

Nonresident owners can change the BAIT result. The New Jersey credit may work on the New Jersey side, but the owner’s resident state may not offer a matching credit. Review each owner’s state of residence, credit rules, and tax profile.

Mistake #3 –BAIT Credit Tracing for Tiered Partnerships

Tiered entities require additional review because the BAIT credit may flow through multiple ownership layers.

BAIT may help one member more than another due to ownership percentages, resident states, marginal rates, cash flow priorities, and SALT limitation positions. Document differences and ensure the client understands who benefits and why.

New Jersey Business Tax Forms CPAs Should Review for CBT and BAIT

Tie planning to forms that reveal exposure: corporate-level, pass-through-level, owner-level, or payment-timing related.

Review filing status, income reporting, and BAIT addback treatment.

NJ-1065

Partnership information return

BAIT does not remove all partnership filing responsibilities.

PTE-100

BAIT return

Review entity-level BAIT calculation, member shares, and payments.

Estimated payment records

CBT, BAIT, owner-level payment review

Confirm timing, amounts, and the responsible party.

Owner/member statements

Credit and allocation support

Confirm owner-level reporting and credit allocation.

BAIT addback: The PTE/BAIT deduction taken for federal purposes should be added back to partnership or S corporation income on the appropriate New Jersey return line, as directed by the current-year instructions.

Verify before filing: New Jersey rates, forms, instructions, payment rules, and BAIT guidance can change by tax year. Confirm current-year CBT, CTF, BAIT, and PTE instructions and estimated payment instructions.

New Jersey Business Tax Planning Opportunities CPAs Often Miss

These standard issues get missed when firms wait until return preparation, similar to common year-end tax research mistakes that appear when state-specific planning is delayed until filing season.

Model the $10 Million Corporate Transit Fee Threshold: Review C corporations and combined groups near $10 million before year-end. Focus on income timing, accrued expenses, fixed assets, intercompany charges, apportionment, and combined group projections. Tie planning items to business records and projection assumptions.

Review BAIT Benefits at the Owner Level: The entity may qualify, but the benefit depends on each owner’s tax profile. Ask whether the owner is above the federal SALT limitation, what the federal marginal rate is, whether the resident state allows a credit, whether BAIT affects owner-level estimates, and whether the owner has enough New Jersey tax liability or refundable credit treatment.

Coordinate S Corporation Compensation With BAIT Planning: : Reasonable compensation and BAIT planning should be reviewed together. Shareholder wages reduce pass-through income; distributions and remaining business income affect amounts flowing through. Compensation decisions can change the pass-through income base.

Identify Dormant and Low-Activity New Jersey Entities: Dormant entities create filing costs, minimum tax exposure, and missed compliance. Identify entities with no current business use, open prior-year registrations, New Jersey accounts with little activity, minimum tax exposure, and cleanup or dissolution opportunities.

What New Jersey CBT and BAIT Planning Does Not Solve

It does not eliminate the New Jersey tax. BAIT changes who pays and how the federal deduction may work, but New Jersey liability still must be paid.

It does not benefit every owner equally. Owner residency, federal tax rate, resident-state credits, cash flow, and SALT limitation position can change the result.

It does not repair a weak entity structure alone. Wrong entity type, poor records, and outdated ownership documents require separate fixes.

It does not erase estimated or missed payments. Late payments may still create penalties and interest.

It does not replace nexus and apportionment analysis. Multi-state clients need a separate review of where they do business, income sourcing, and receipt apportionment.

It does not replace CPA judgment. The election and planning steps should support the CPA’s recommendation, not substitute for it.

How CPA Firms Should Review New Jersey Business Tax Clients

Follow a consistent sequence: entity classification, corporate exposure, BAIT modeling, estimated payments, and documentation. For multi-state clients, connect to broader federal versus state tax differences.

1. Segment New Jersey Clients by Entity Type

C corporations.

S corporations.

Partnerships.

LLCs are taxed as partnerships.

LLCs taxed as S corporations.

Multi-entity groups.

Businesses with nonresident owners.

Dormant or low-activity entities.

2. Identify CBT and Corporate Transit Fee Exposure

For C corporations and combined groups: projected entire net income, New Jersey allocated taxable net income, combined reporting status, CTF threshold exposure, credits, estimated payments, and prior-year trends. Decide whether a standard CBT review is enough or whether year-end planning is needed.

3.Model BAIT at the Owner Level

For pass-through entities: eligibility, New Jersey distributive proceeds, owner residency, federal marginal rate, SALT limitation position, resident-state credits, refundable New Jersey credit treatment, payment timing, and cash flow. For projection-heavy clients, use AI tax projection workflows to structure assumptions. Explain why BAIT was elected or not.

4.Review CBT, BAIT, and Owner Estimated Payments

Check BAIT, CBT, and owner-level estimates; payment responsibility; portal access; cash availability; and penalty exposure. Assign this step to one person.

5. Document the New Jersey Tax Planning Recommendation

Document entity type, tax year reviewed, income projection date, owner residency facts, BAIT/CBT/CTF assumptions, estimated payment plan, client approval or rejection, and known limitations.

How CPA Pilot Supports New Jersey CBT and BAIT Research

CPA Pilot helps CPAs research, organize, and document state tax issues faster. As an AI tax assistant for CPA firms, it helps teams turn complex state and federal issues into organized research notes, review checklists, and client-ready explanations.

For firms handling New Jersey tax planning, CPAs can use CPA Pilot as a research and review layer for CBT rate checks, Corporate Transit Fee exposure analysis, combined reporting considerations, BAIT election modeling, SALT workaround mechanics, estimated payment timing, and client-facing explanations.

CPA Pilot can help tax teams:

Summarize New Jersey DOR guidance

Compare CBT rates and CTF thresholds

Draft issue-specific research notes

Identify client follow-up questions

Organize support for the combined reporting and Nexus review

Prepare plain-English client summaries

Document where human CPA judgment is still required

CPA Pilot does not replace the CPA’s decision-making. The CPA still decides whether the CBT/CTF exposure is supportable, whether combined reporting applies, whether the BAIT election is appropriate for each owner, whether SALT workaround modeling produces the expected benefit, and whether estimated payment timing and amounts are reasonable.

Need a faster way to review New Jersey CBT, BAIT, and Corporate Transit Fee issues? CPA Pilot helps tax teams organize state-specific research, model planning assumptions, and draft client-ready explanations with CPA judgment still in control. Book a CPA Pilot demo to see how it fits into your firm’s tax workflow.

FAQs About New Jersey Business Tax Planning

What should CPAs review first for New Jersey business tax planning?

Entity type, New Jersey filing obligations, CBT exposure, CTF risk, BAIT eligibility, estimated payments, and owner residency.

Which businesses should consider the NJ BAIT election?

Partnerships, S corporations, and qualifying LLCs with eligible owners, when the election may improve federal deduction treatment and owner-level NJ credit outcomes. Model before filing.

Does New Jersey BAIT always create tax savings?

No. The benefit depends on the owner’s federal tax profile, resident-state credits, owner residency, payment timing, and cash flow.

Why does combined reporting matter for New Jersey CBT planning?

Combined reporting can change how related corporations are reviewed for CBT and CTF exposure. Looking at each entity separately may miss group-level taxable income or apportionment issues.

What New Jersey business tax forms should CPAs review?

CBT-100, CBT-100S, NJ-1065, PTE-100, estimated payment records, BAIT schedules, owner/member statements, and documents supporting allocation or credit treatment.

When should CPAs start New Jersey year-end tax planning?

Before Q4, when possible. CBT exposure, BAIT modeling, estimated payments, and owner-level planning are harder to clean up after year-end.

Disclaimer: This article is provided by CPA Pilot for educational purposes. While we may offer tax software/services, the information here is general and may not address your specific facts and circumstances. It does not constitute individual tax, legal, or accounting advice. U.S. federal and State Tax laws change frequently; please consult a qualified tax professional before acting on any information.

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.

![Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]](/_next/image/?url=%2Fuploads%2Fwashington-bo-tax-3811057f.webp&w=3840&q=75)