Ohio CAT Tax Planning for CPAs – Client Review Workflow After the $6M Threshold Change - CPA Pilot

Multistate Tax Planning

Ohio CAT Tax Planning for CPAs – Client Review Workflow After the $6M Threshold Change

CPA Pilot

Jun 4, 2026·19 min read

Should CPAs still treat Ohio CAT as a routine filing task after the $6 million threshold change? No. Ohio CAT planning now requires a more careful review of Ohio taxable gross receipts, CAT account status, quarterly filing exposure, and whether a client should file, monitor, or cancel its Commercial Activity Tax account.

TL;DR – Ohio CAT Tax Planning for CPAs

Ohio CAT tax planning now requires CPAs to review current client facts instead of relying on prior-year filing habits.

The $6M threshold change makes Ohio CAT review a planning decision, not just a recurring compliance task.

CPAs should base the review on Ohio taxable gross receipts, current business activity, account records, and supportable documentation.

A strong Ohio CAT workflow separates verified facts, open assumptions, source documents, reviewer notes, and client-ready recommendations.

Account cancellation should be treated as a documented tax-position decision, not a quick administrative task.

Business changes such as new Ohio customers, new sales channels, related entities, or uneven quarterly revenue should trigger a fresh CAT review.

Clear client communication matters because clients need to understand the recommendation, the records reviewed, and when the issue should be revisited.

CPA firms can reduce rework by building Ohio CAT review into a repeatable state-tax advisory workflow.

CPA Pilot supports Ohio CAT tax planning for CPAs by helping firms organize research, document open items, draft advisory notes, and preserve human CPA judgment.

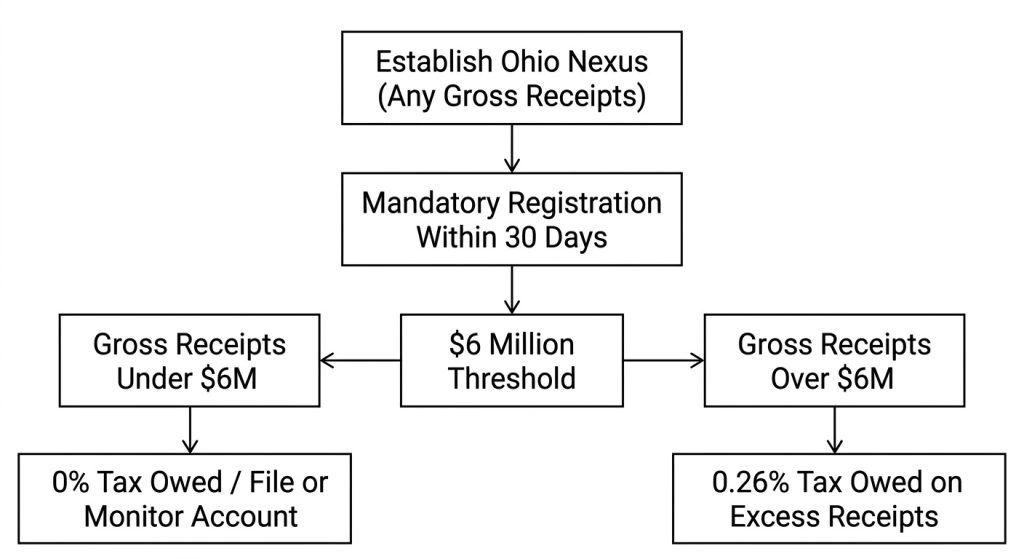

For tax years 2025 and forward, taxpayers must register with the Ohio Department of Taxation within 30 days of first having Ohio taxable gross receipts (when nexus is established). The $6 million exclusion means you only owe tax on receipts above $6 million, but registration is required once you have any Ohio gross receipts with substantial nexus.

The current Ohio CAT framework decouples the requirement to register from the requirement to pay tax, demanding an active advisory approach.

Ohio also lists the CAT rate at 0.26% of taxable gross receipts over the exclusion amount (Source).

This means a CPA should not rely only on total business revenue, net income, or last year’s filing pattern before advising a client.

Ohio CAT is a good example of why CPAs need to understand federal and state tax differences before relying on a client’s federal taxable income, total business revenue, or prior-year filing pattern. A business may look simple from a federal return perspective, but state-level gross receipts rules can require a separate review before the CPA gives a filing recommendation.

For firms using CPA Pilot, Ohio CAT tax planning for CPAs becomes easier to turn into a repeatable advisory workflow. Instead of starting from a blank research note, tax teams can review current state-tax rules, organize client facts, summarize filing exposure, and prepare a client-ready explanation around one clear decision: file, monitor, or cancel.

That decision is the starting point for this guide. Before reviewing thresholds, accounts, or cancellation steps, CPAs need to understand which Ohio CAT facts actually affect planning.

Ohio CAT Rules That Affect CPA Planning Decisions

Ohio CAT planning starts with the tax base. The Commercial Activity Tax is measured by Ohio taxable gross receipts, which means CPAs must look beyond a client’s profit, federal taxable income, or ordinary income statement totals.

Because Ohio CAT is part of a broader state and local tax planning conversation, CPAs should treat it as a separate state-level review instead of folding it into federal income-tax analysis.

Unlike small business tax deductions, Ohio CAT planning does not start with deductible expenses. It starts with whether the client’s receipts create state-level filing exposure.

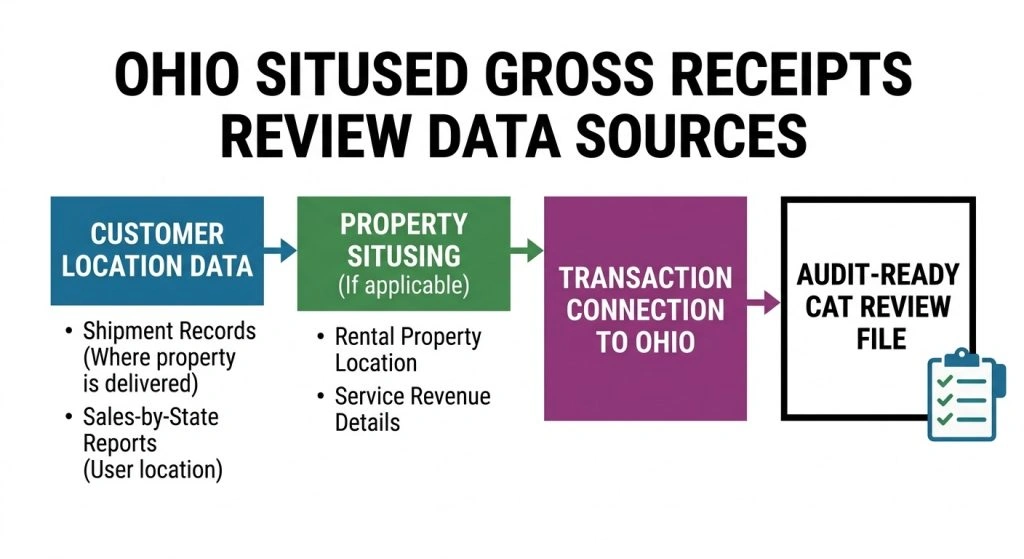

Ohio defines taxable gross receipts as gross receipts that are sitused to Ohio, making sourcing the first technical issue in a CAT review. The Ohio Department of Taxation explains this directly in its CAT taxable gross receipts guidance.

For planning purposes, the key facts are practical. A receipt may need to be reviewed based on

Where the property is delivered,

Where services are used,

Where the rental property is located, or

How the transaction connects to Ohio.

This is why a sales-by-state report, customer-location data, shipment records, and service revenue details often matter more than the client’s total revenue number.

Because Ohio CAT is based on sourced gross receipts, standard federal income tax summaries are insufficient; CPAs must audit operational data.

Entity structure also affects the review. Ohio recognizes CAT group concepts, including combined taxpayer and consolidated elected taxpayer treatment, so related businesses may need to be reviewed together rather than in isolation.

If the client has multiple businesses, the CAT review should be coordinated with the firm’s broader entity structure analysis so ownership, grouping, and filing assumptions stay consistent across the client file.

For CPAs, these facts create the foundation for a clean planning file:

Identify Ohio-sourced receipts,

Confirm how the client’s entities are treated, and support the conclusion with records.

The next issue is why older Ohio CAT review habits can create problems under the current rules.

Outdated Ohio CAT Review Habits That Create Filing Risk

Old Ohio CAT review habits can create problems when CPAs rely on last year’s workpapers without testing whether the client’s current facts still support the same conclusion. Ohio CAT changed enough that a prior filing pattern, old threshold note, or copied rollover memo may no longer be reliable for the current tax year.

1. Prior-Year Workpapers May Not Reflect the Current CAT Position

A prior-year CAT workpaper can be a useful background, but it should not be treated as the final answer. Client receipts may shift by customer location, sales channel, product mix, or service market during the year. When client revenue changes during the year, CPAs can connect the Ohio CAT review with tax projection workflows to decide whether the prior conclusion still holds. This is especially useful for clients with seasonal revenue, new Ohio customers, expanding sales channels, or one-time contracts that may shift the filing position.

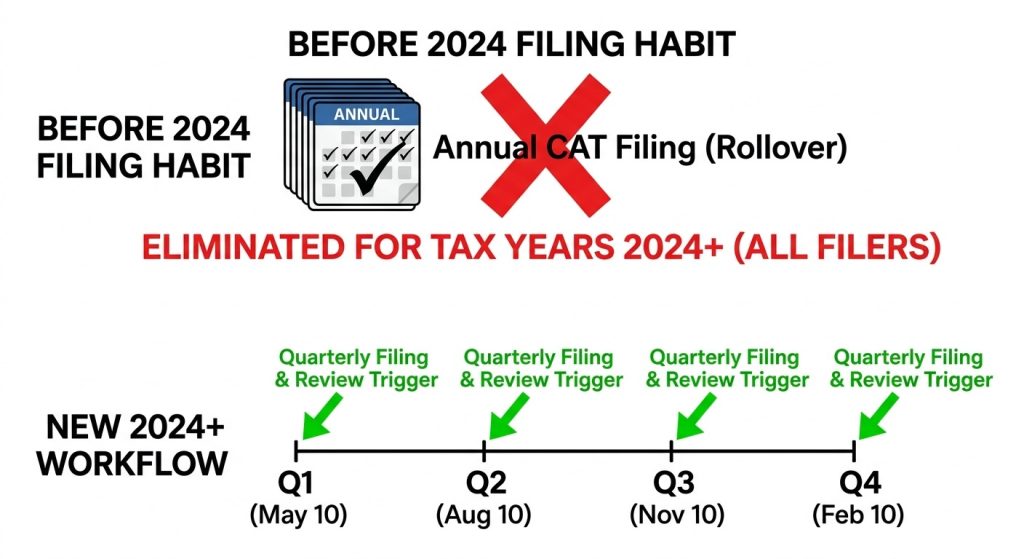

2. Rollover Filing Habits Can Create Unnecessary Admin Work

Relying on legacy annual filing workflows for 2024+ creates significant compliance risk, as all active CAT accounts must now file quarterly.

Some firms keep CAT tasks on the same calendar because the process existed in prior years. That creates avoidable work when the client no longer has the same filing need. The Ohio Department of Taxation confirms that annual filing was eliminated for tax years 2024 and forward, which means CPAs should be careful about relying on legacy annual filing workflows.

3. Missed Internal Review Points Can Lead to Client Confusion

The bigger planning problem is not only whether a return is due. It is whether the firm can explain the conclusion clearly. If the CPA does not update the client file, the client may receive mixed messages from old engagement notes, prior-year reminders, or outdated filing assumptions. A cleaner process is to refresh the CAT conclusion each year and keep the reasoning tied to current Ohio guidance, current client records, and the firm’s documented review.

That is why Ohio CAT planning should not depend on rollover notes or prior-year assumptions alone. Once the old filing pattern has been questioned, the next step is to rebuild the review from the client’s current records.

A structured workflow helps CPAs move from uncertainty to a clear, documented position on Ohio CAT exposure.

CPA Workflow for Reviewing Ohio CAT Exposure

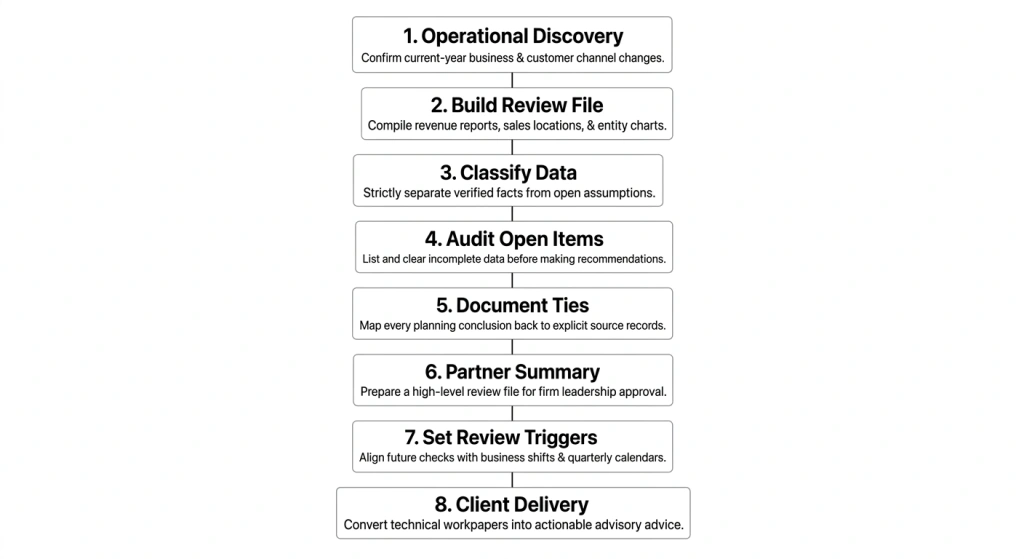

A strong Ohio CAT workflow should help the CPA move from raw client data to a defensible advisory conclusion. Instead of repeating the tax rules in every workpaper, the review should be organized around current-year facts, source documents, open questions, reviewer notes, and a client-ready recommendation.

Adopting a structured 8-step review workflow ensures that technical positions are backed by operational source documents, radically reducing risk before finalizing a client’s filing recommendation.

Step 1: Confirm Current-Year Business Changes

Start with a short client-change interview before reviewing reports.

Ask whether the client:

Added Ohio customers,

Entered new states,

Changed sales channels,

Opened or closed locations,

Added related entities,

Changed shipping patterns, or

Started using marketplace platforms.

These operational changes often explain why the current-year CAT position may differ from the prior-year file.

Step 2: Build the Ohio CAT Review File

Create a separate current-year CAT review file instead of rolling forward the prior-year memo without changes. The file should include revenue reports, sales-location data, prior CAT activity, entity charts, client notes, and any records needed to support the review.

When the workpaper cites a filing obligation or registration issue, tie it to current Ohio Department of Taxation guidance, such as the state’s official Commercial Activity Tax page.

Step 3: Separate Verified Facts From Open Assumptions

The workpaper should clearly separate what the firm knows from what still needs confirmation. Confirmed facts may include client reports, prior filings, account records, or entity documents.

Assumptions may include:

How certain receipts are classified,

Whether a new sales channel affects Ohio activity, or

Whether the client’s current reports fully capture Ohio activity.

Step 4: List Open Items Before Finalizing the CAT Position

If the records do not clearly support the conclusion, list the missing items before making a recommendation.

Common open items include:

Incomplete sales-by-state reports,

Unclear service revenue details,

Missing ownership information,

Prior CAT notices,

Unavailable online account access, or

Unanswered client questions.

This step protects the firm from turning an incomplete review into a final advisory position too early.

Step 5: Tie Each Conclusion to Source Documents

Every planning conclusion should connect back to a record. A revenue number should tie to a client report. An account-history note should tie to the client’s Ohio tax account record. A filing-position note should tie to current Ohio guidance or an internal research memo.

For electronic registration and filing activity, Ohio’s official CAT registration materials explain that taxpayers using the Gateway for registration may file a CAT return after registering, which makes online account access part of the review trail through the CAT registration form guidance.

Step 6: Prepare a Reviewer-Friendly Summary

The final internal summary should be short enough for a partner, manager, or client-service lead to understand without having to reopen every report. A useful summary includes the period reviewed, records used, unresolved items, recommended action, next review trigger, and who approved the conclusion.

Do not let the CAT review become a one-time note if the client’s Ohio activity may change. Set a specific review date or trigger, such as

The next quarter-end, a major revenue increase,

A new Ohio customer segment,

A new related entity, or

A change in sales reporting.

Ohio lists CAT quarterly due dates on its official tax due dates page, so firms can align internal review timing with the state filing calendar when needed.

For clients with changing revenue patterns, Ohio CAT review should be added to the firm’s year-end tax planning strategies, so filing exposure is reviewed before deadlines create pressure. This helps the firm address Ohio CAT as part of proactive advisory work, not as a last-minute compliance task.

Step 8: Turn the Workpaper Into a Client-Ready Message

The last step is converting the technical review into language the client can act on. Instead of saying “CAT exposure was reviewed,” the client note should explain what changed, which records were checked, which items remain open, what action is recommended, and when the issue should be reviewed again.

A clean workpaper helps the CPA reach a supportable conclusion, but the highest-risk point often comes after the review is complete: deciding whether the client’s Ohio CAT account should remain open or be canceled. That decision should be treated as a documented tax-position judgment, not a quick administrative cleanup.

Ohio CAT Account Cancellation – CPA Review Points Before Canceling

Ohio CAT account cancellation can be appropriate when a client no longer has a filing obligation, but CPAs should be careful before treating cancellation as automatic. The risk is not only canceling too late or too early. The risk is canceling without enough evidence to support why the client’s Ohio CAT position changed.

Before recommending cancellation, confirm that the client’s current-year records support the conclusion that a final quarterly CAT return has been filed, no unresolved CAT notices or open filing periods remain, and that the client understands when the issue may need to be reviewed again.

The CAT registration and filing requirements depend on taxable gross receipts, so the cancellation decision should be tied to the same records used in the CPA’s review file.

A careful cancellation review should also consider timing. If the client is close to the filing threshold, has uneven quarterly revenue, or recently changed markets, cancellation may create extra work later if the account needs to be reopened.

In those cases, the better recommendation may be to keep monitoring the position until the client’s Ohio activity is more predictable.

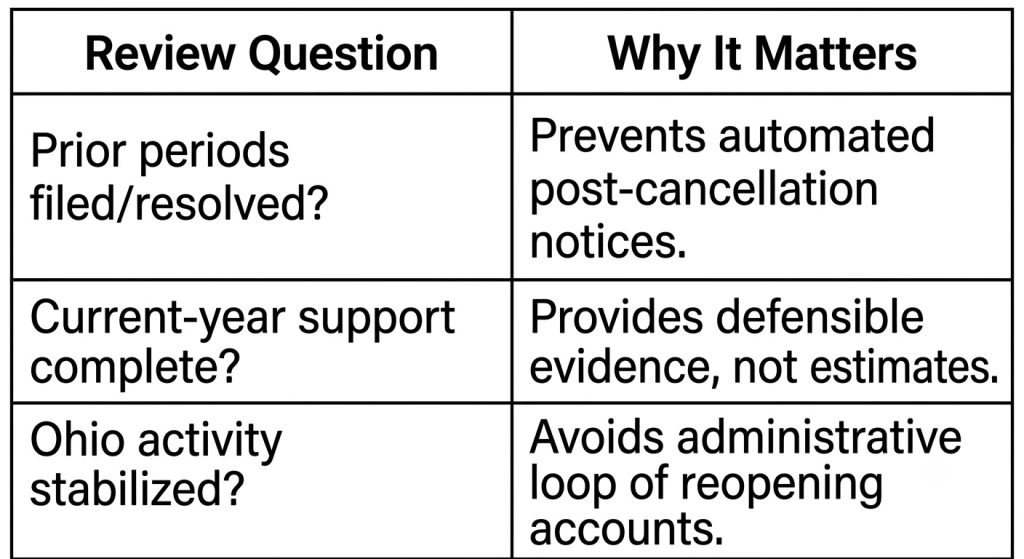

Use this decision filter before canceling:

Review Question

Why It Matters

Are all prior CAT periods filed or resolved?

Open periods can create notices after cancellation.

Does the current-year support clearly show no filing obligation?

The CPA needs evidence, not a rough estimate.

Has the client’s Ohio activity changed recently?

New customers, locations, or channels can change the conclusion. If yes, do not cancel until activity stabilizes.

Is the client close to the threshold?

A small revenue shift may require renewed review.

Has the client been told when to notify the CPA?

Future changes should trigger a new CAT review.

If cancellation is recommended, the client file should include the reason for cancellation, the records reviewed, any open items cleared, and the next trigger for review.

For account access and business tax updates, CPAs should confirm the client’s online records through the Ohio Business Gateway before the recommendation is finalized.

After the cancellation decision is documented, CPAs still need a way to know when the Ohio CAT review should be reopened. The most useful trigger is not a calendar date alone. It is a business change that could make the prior conclusion unreliable.

Business Changes That Should Trigger a New Ohio CAT Review

A fresh Ohio CAT review is usually needed when the client’s business activity changes enough to make the prior workpaper incomplete. These triggers help CPAs decide when to reopen the issue instead of waiting for year-end.

Common review triggers include:

A new Ohio customer segment

A new e-commerce or marketplace sales channel

A major contract with Ohio-based customers

A new warehouse, office, or business location

A new related entity, acquisition, or ownership change

A change in how sales reports classify customer location

A sharp increase in quarterly revenue

A prior CAT notice or unresolved Ohio tax account issue

The goal is not to repeat the full CAT analysis every month. The goal is to identify business events that could change the prior conclusion. If one of these triggers appears, the CPA should update the review file, confirm the supporting records, and decide whether the client’s Ohio CAT position has changed.

Once CPAs know which business changes can reopen an Ohio CAT review, the next priority is avoiding mistakes that make the final recommendation harder to defend.

Most CAT issues do not come from one missing number. They come from weak assumptions, unclear records, or a client file that does not show how the firm reached its conclusion.

Ohio CAT Planning Mistakes That Create CPA Rework

Ohio CAT planning mistakes usually create two problems for CPA firms:

Extra administrative cleanup and

Weaker client communication.

The goal is not just to reach the right answer. The goal is to make the answer supportable if the client asks questions, receives a notice, or changes facts later.

Mistake 1: Treating a Prior Filing Pattern as Proof

A prior filing history can show what happened before, but it does not prove the current-year position. If the firm relies only on a prior-year return, an old calendar reminder, or a copied memo, the review may miss current-year business changes. The better approach is to use prior filings as background and current records as support.

Mistake 2: Not Checking Whether the Account Still Matches the Client’s Facts

A client’s Ohio tax account may remain active even when the firm’s current review suggests a different administrative step. That mismatch can create reminders, open tasks, or avoidable client questions. Ohio states that businesses with an active CAT account are required to file quarterly returns beginning with tax year 2024 and forward, so the account status should match the current conclusion before the firm closes the review.

Mistake 3: Closing the Review With Unresolved Open Items

If sales reports are incomplete, online account access is unavailable, or client answers are still pending, the review should not be finalized as if all facts are confirmed. Open items should be listed clearly so the partner, reviewer, or client-service lead can see what still affects the conclusion.

Mistake 4: Writing a Technical Conclusion the Client Cannot Understand

A technically correct conclusion can still fail if the client does not know what action to take. Avoid internal-only wording such as “CAT reviewed, no issue noted.” A better client-facing note should explain the records reviewed, the decision reached, and the business changes that should trigger a future update.

Mistake 5: Missing the Filing Calendar After the Review

Even when the tax position is clear, the firm still needs a timing control. Ohio lists business tax due dates, which CPAs can use to align internal task lists with CAT filing periods. Missing the calendar step can turn a completed technical review into a late administrative task.

Once the firm avoids common review mistakes, the next step is making the Ohio CAT conclusion easy for the client to understand.

How CPAs Should Explain Ohio CAT Review Results to Clients

A strong Ohio CAT client explanation should be short, specific, and action-oriented. Most clients do not need a full technical discussion of CAT rules. They need to understand whether the firm reviewed the right records, whether any action is needed, and what business changes could require a future update.

A useful client message can follow this structure:

We reviewed your Ohio CAT position using your current business activity, available revenue records, and Ohio tax account information.

Based on the records reviewed, we recommend the following next step:

[file/monitor / cancel/provide more information]. If your Ohio activity, sales channels, entity structure, or customer base changes during the year, we should revisit this conclusion.

For clients who ask why this review matters, keep the explanation tied to official Ohio guidance rather than internal firm language.

The final client note should avoid vague phrases such as “CAT looks fine” or “no issue noted.” Instead, use language that states the records reviewed, the recommendation, and the next trigger for review.

This gives the client a practical answer and gives the CPA firm a communication trail that matches the workpaper.

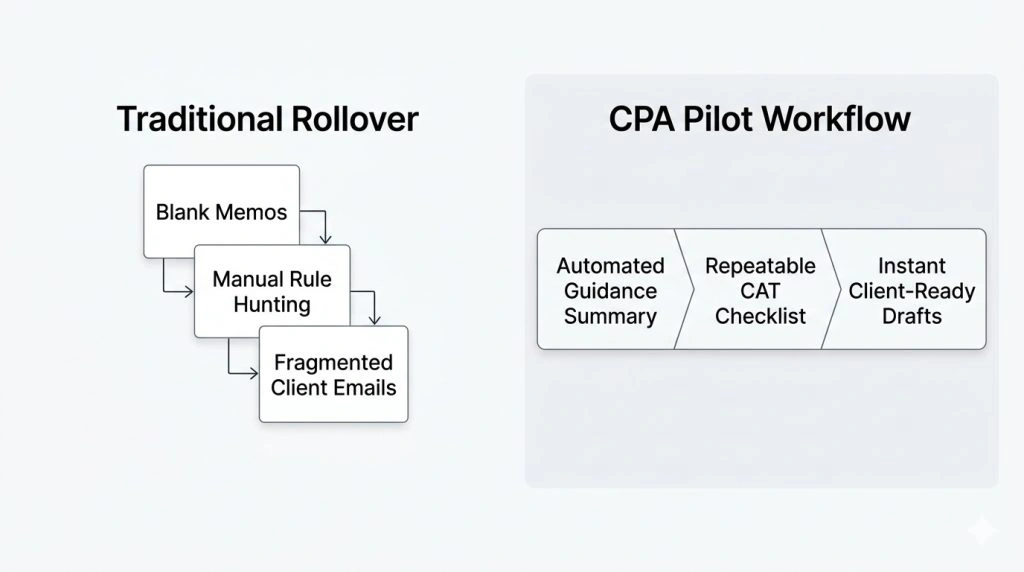

How CPA Pilot Supports a Repeatable Ohio CAT Review Workflow

A repeatable Ohio CAT workflow helps CPA firms review clients consistently, assign work clearly, store, and prepare recommendations, all without rebuilding the same process every year.

The goal is not to make every client file look identical. The goal is to make every review easy to update, easy to explain, and easy to approve.

Start by creating a standard Ohio CAT review template inside the firm’s tax planning process. The template should include fields for business changes, records received, open items, online account access, reviewer notes, and the next review trigger.

It should also include a place to link to current Ohio guidance, so staff are not relying on outdated saved notes.

Next, assign ownership for each stage of the review. A preparer may collect records, a senior may organize the research file, and a manager may approve the final recommendation.

The firm should also connect the workflow to internal tax calendars, so CAT review reminders, client follow-ups, and approvals happen before filing pressure builds.

CPA Pilot helps CPAs apply AI for tax research by organizing state-tax guidance, review notes, open items, and client-ready explanations faster. . For firms handling Ohio CAT tax planning for CPAs, CPA Pilot can act as a research and review layer for taxable gross receipts questions, account-status review, quarterly filing checks, client follow-up items, and plain-English advisory explanations.

For firms trying to standardize recurring advisory tasks, Ohio CAT review can become part of broader time-saving tax workflows for CPAs instead of a one-off research project. A consistent workflow helps staff know what to review, where to document support, and when to escalate open questions.

This is where the difference between AI vs traditional tax planning becomes practical: the CPA still makes the judgment, but AI can help organize research, summarize rules, and draft the first client-ready explanation.

CPA Pilot can help tax teams:

Summarize the Ohio Department of Taxation guidance

Organize Ohio CAT research notes

Create a repeatable CAT review checklist

Track open items before a recommendation is finalized

Draft client-ready CAT explanations

Support quarterly review workflows using Ohio filing due dates

Document where human CPA judgment is still required

CPA Pilot does not replace the CPA’s decision-making. The CPA still decides whether the client’s Ohio CAT position is supportable, whether receipts are properly reviewed, whether the account should remain active, whether cancellation is appropriate, and whether additional client records are needed before giving a final recommendation.

Don’t waste time rebuilding the same state-tax research notes again and again. Review CPA Pilot pricing plans or book a demo to see how CPA Pilot supports repeatable tax research workflows.

Ohio CAT Tax Planning FAQs for CPAs

When should a business register for Ohio CAT?

A business should register for Ohio CAT after the client first has Ohio taxable gross receipts (when nexus is established). There is no registration threshold – the $6M is the exclusion amount for owing tax, not for registering. CPAs should verify receipts, timing, and account setup before advising the client.

What records should CPAs keep for an Ohio CAT review?

CPAs should keep sales-by-state reports, customer-location data, shipment records, entity charts, prior CAT filings, account access notes, and the final written CAT conclusion.

Can Ohio CAT apply to an out-of-state business?

Yes. Ohio CAT can apply to an out-of-state business if it has taxable gross receipts sitused to Ohio and meets Ohio’s CAT filing requirements.

What should a CPA do if a client receives an Ohio CAT notice?

A CPA should review the notice, match it against the client’s CAT account history, check open filing periods, confirm records, and respond before changing the filing position.

Who should review the Ohio CAT inside a CPA firm?

The Ohio CAT review should involve the preparer, reviewer, and manager or partner when facts involve multistate sales, related entities, account cancellation, or unclear client records.

Was this article helpful?

Sorry about that. How can we improve?

Thanks for the feedback! It helps us improve.

Share

Harsh Mody

CPA & Founder of CPA Pilot

I’m Harsh Mody, CPA, founder of CPA Pilot—an AI Tax Assistant for CPAs, Enrolled Agents, and U.S. tax firms. With 18+ years in accounting, tax auditing, consulting, and product management, I’ve seen how compliance-heavy work limits true advisory impact. I built CPA Pilot to change that—by applying AI-driven tax research, deduction optimization, and IRS/state code automation to help firms unlock tax savings and scale advisory services with speed and accuracy.

![Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]](/_next/image/?url=%2Fuploads%2Fwashington-bo-tax-3811057f.webp&w=3840&q=75)