![Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]](https://www.cpapilot.com/blog/wp-content/uploads/2026/05/Washington-BO-Tax-.png)

Cryptocurrency Tax Reporting for CPAs: Forms, Rules & Client Strategies [2026]

![Cryptocurrency Tax Reporting for CPAs: Forms, Rules & Client Strategies [2026]](https://www.cpapilot.com/blog/wp-content/uploads/2026/04/Cryptocurrency-Tax-Reporting.png)

[Last Updated on 2 months ago]

Cryptocurrency tax reporting requires CPAs and EAs to file digital asset transactions like sales, swaps, staking, DeFi activity, and NFTs on Form 8949, Schedule D, and Schedule 1.

Starting with the 2025 tax year transactions (filed in 2026), broker platforms must issue Form 1099-DA for proceeds from sales, swaps, and certain redemptions, though cost basis reporting remains limited.

The IRS Notice 2014-21 classifies virtual currency as property, heightening matching risks for unreported crypto as broker data flows to the IRS.

TL;DR – Cryptocurrency Tax Reporting

- Cryptocurrency tax reporting is now a core compliance issue for CPAs, not a niche service.

- For 2025 transactions filed in 2026, many broker platforms must issue Form 1099-DA for crypto sales, swaps, and certain redemptions.

- Most 2025 Forms 1099-DA will likely report gross proceeds only, with little or no cost basis information.

- CPAs must still report crypto dispositions on Form 8949 and Schedule D.

- Staking rewards are generally taxed as ordinary income when received and usually reported on Schedule 1 or Schedule C.

- Most crypto-to-crypto swaps are taxable dispositions.

- DeFi transactions remain complex, and some areas still lack direct IRS guidance, but tax reporting obligations still apply.

- NFTs generally follow property tax rules, though some may be treated as collectibles.

- Reconstructing cost basis across wallets, exchanges, and transfers is now a major part of crypto tax prep.

- CPAs that build repeatable crypto workflows now can reduce client IRS exposure and turn crypto tax work into a high-value advisory service.

This guide dives into practitioner workflows: required forms, cost basis methods across multiple exchanges, DeFi/staking income rules, and NFT reporting, skipping crypto basics for busy CPAs and EAs facing their first digital asset clients.

The crypto question has appeared on Form 1040 since 2019, and with Form 1099-DA now live, compliance gaps are closing fast.

Table of Contents

- Form 1099-DA for CPAs: What to Know for 2025 Tax Returns

- How to Report Cryptocurrency on Form 8949 and Schedule D

- Crypto Cost Basis Methods for CPAs: FIFO vs. Specific Identification

- How Staking Rewards are Taxed: Rev. Rul. 2023-14 and Jarrett

- How DeFi Transactions are Taxed: Swaps, Liquidity Pools, and Wrapped Tokens

- How NFTs Are Taxed: Collectibles Rules Under IRC Section 408(m)

- State Tax Treatment of Cryptocurrency for CPAs

- How to Reconstruct Crypto Cost Basis When Client Records are Incomplete

- DeFi Broker Reporting in 2026 – The Current State

- Turn Crypto Tax Complexity Into Advisory Value

- Common Queries About Cryptocurrency Tax Reporting

Form 1099-DA for CPAs: What to Know for 2025 Tax Returns

The Infrastructure Investment and Jobs Act (P.L. 117-58, §80603) mandated crypto broker reporting on Form 1099-DA starting in 2025. See the IRS digital assets page and Form 1099-DA instructions. Coinbase, Kraken, and Gemini began issuing these for 2025 transactions.

The form includes these fields:

- Box 1a: Digital asset code (DTIF identifier; e.g., the code for BTC)

- Box 1b: Description of digital asset (e.g., “Bitcoin”)

- Box 1c: Number of units sold

- Box 1d: Date acquired

- Box 1e: Date sold or disposed

- Box 1f: Gross proceeds

- Box 1g: Cost or other basis (voluntary for 2025; mandatory for covered securities from 2026)

- Box 9: Checkbox indicating the digital asset is a non-covered security

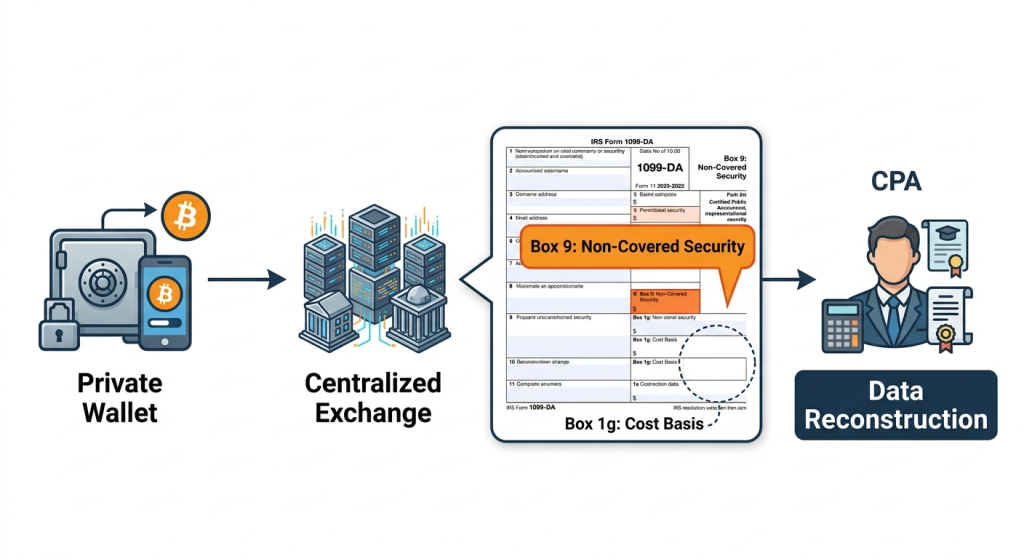

The non-covered checkbox (Box 9) will cause headaches. If a client transferred Bitcoin from a personal wallet to Coinbase and then sold it, the exchange doesn’t know the original cost basis. Box 1g is blank, and Box 9 is checked. You’ll need to reconstruct the basis from blockchain history and historical price data.

Important for 2025 returns: Per the 2025 Form 1099-DA instructions, brokers are not required to report basis information for any sales effected in 2025 — basis reporting is entirely voluntary this year. Expect the vast majority of 1099-DAs received for 2025 to show gross proceeds only, with Box 1g blank. Full basis reporting for covered securities (assets acquired and held at the same custodial broker) becomes mandatory starting January 1, 2026.

For a broader look, see our post: How IRS tax forms fit into your practice workflow

How to Report Cryptocurrency on Form 8949 and Schedule D

Nothing changes here mechanically. Crypto dispositions still go on Form 8949, which flows to Schedule D. But volume is the problem.

A client actively trading on Coinbase might have 400+ transactions in a year. You need a CSV export or a crypto tax aggregator (CoinTracker, Koinly, CoinLedger, TokenTax) that generates a Form 8949-ready report.

For a workflow-level view of how AI can help process high-volume 1040 preparation, see CPA Pilot’s guide on automating 1040 tax preparation.

Real example: A client sold 2.3 BTC at $97,000 per coin in November 2025 — proceeds of $223,100. Purchased in March 2021 at $42,000 each ($96,600 basis). Long-term capital gain: $126,500. The same client also made 87 smaller trades across three exchanges. The 8949 pulls from aggregated data.

Report each transaction on Part I (short-term) or Part II (long-term) of Form 8949. Use Code H (short-term, basis not reported to IRS) or Code Y (transaction not reported to IRS) for non-covered transactions, the majority for 2025.

Crypto Cost Basis Methods for CPAs: FIFO vs. Specific Identification

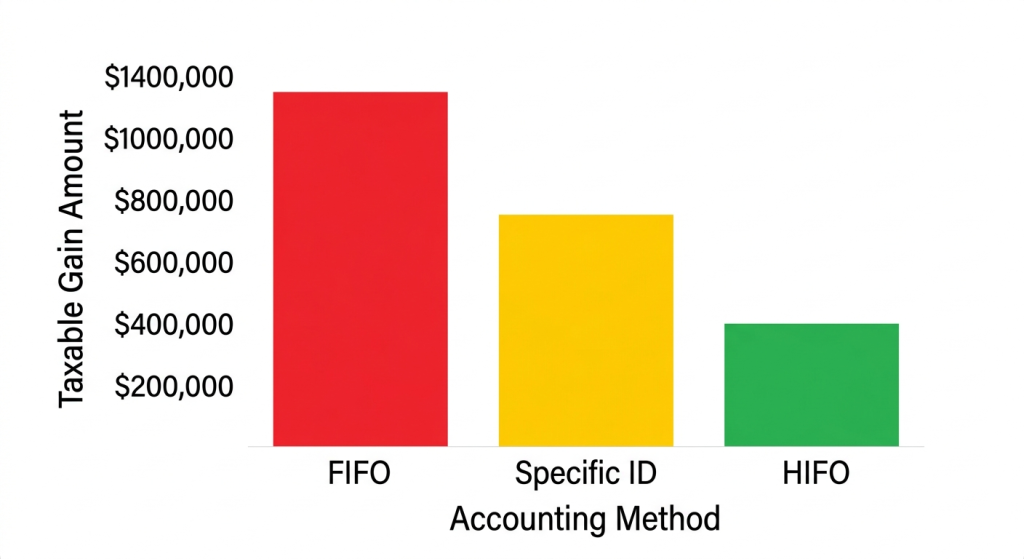

The IRS hasn’t mandated a single cost basis method for crypto. Under Notice 2014-21, virtual currency is property. General disposition rules apply. Options include:

- FIFO (First In, First Out): Default if the client hasn’t identified specific lots. Usually, the worst outcome for early buyers.

- Specific Identification: The client identifies which lots they’re selling at the time of disposition. This is how you minimize gain-sell the highest-basis lots first.

Treas. Reg. §1.1012-1(c) governs specific identification of property, and Notice 2014-21 confirms crypto is property subject to these general disposition rules.

The catch most preparers miss: To use specific identification, the taxpayer must identify the specific unit at the time of sale.

- The identification must be recorded and verifiable. “I sold the expensive ones” after the fact doesn’t satisfy Reg. §1.1012-1(c).

- The exchange must support lot selection, and Revenue Procedure 2024-28 provides transitional guidance for taxpayers allocating unused basis to digital asset wallets as of January 1, 2025.

What CPAs see in practice: most clients haven’t done lot tracking. They show up in April with 1099-DAs and a vague memory.

If they can’t substantiate specific identification, you’re stuck with FIFO. Tell them now to use an exchange that supports lot-level tracking.

| Method | Best For | Risk |

|---|---|---|

| FIFO | Simple cases, few transactions | Often produces the highest gain |

| Specific ID | Active traders with good records | Must be documented at the time of sale |

| HIFO (Highest In, First Out) | Minimizing current-year gain | Subset of specific ID; same documentation rules |

HIFO isn’t a separate method. It’s just specific identification where you always pick the highest-cost lot. Some aggregator tools apply it automatically, which is fine as long as you can show the lot-level selection was made contemporaneously.

How Staking Rewards are Taxed: Rev. Rul. 2023-14 and Jarrett

IRS guidance on staking is thin but settled for now. Rev. Rul. 2023-14 clarified that staking rewards are gross income when the taxpayer “gains dominion and control.” For proof-of-stake networks, that’s when rewards are credited to the account.

The tax is ordinary income, measured at fair market value at the time of receipt. Report on Schedule 1, Line 8z (or Schedule C if the taxpayer is staking as a business).

The Jarrett case argued that staking rewards are “new property” not taxable until sold — essentially treating them like a farmer harvesting crops, not income. The IRS disagreed and issued Rev. Rul. 2023-14 specifically to reject that position. Don’t rely on Jarrett. Clients owe tax on staking rewards when received.

Practical issue: If a client received 4.2 ETH in staking rewards over the year, you need FMV on each credit date — potentially daily. Aggregator tools handle this. For research-heavy staking and DeFi scenarios, AI tax research tools can surface citable authority faster than manual searches through IRS notices.

How DeFi Transactions are Taxed: Swaps, Liquidity Pools, and Wrapped Tokens

DeFi is the hardest part of crypto tax. IRS guidance is unhelpfully vague. Here’s the current state:

- Token swaps (e.g., swapping ETH for USDC on Uniswap): each swap is a taxable disposition under IRC §1001. Gain or loss equals FMV received minus basis given up. This is settled law under Notice 2014-21. Post-TCJA, IRC §1031 applies only to real property.

- Liquidity pool deposits: Depositing ETH and USDC into a Uniswap pool in exchange for LP tokens – is that taxable? The IRS hasn’t issued direct guidance. Conservative position: it’s a disposition (taxable). LP token basis equals FMV at deposit. Most practitioners take the conservative position.

- Wrapped tokens (e.g., ETH to WETH): wrapping is arguably a non-event since WETH is 1:1 redeemable. The safe position: treat it as taxable with zero gain. Keep records either way. Note that Notice 2024-57 temporarily exempts wrapping and unwrapping from Form 1099-DA broker reporting pending further IRS guidance — but this is a reporting exception, not a tax exclusion. The underlying tax analysis remains unsettled.

- Yield farming: Interest or rewards earned through DeFi protocols are ordinary income, the same as staking. Report at FMV when received.

After knowing how DeFi Transactions are taxed, let’s explore how NFTs are taxed.

How NFTs Are Taxed: Collectibles Rules Under IRC Section 408(m)

NFT taxation follows general property rules. Buy an NFT, sell it later for more — capital gain. The twist: the IRS issued Notice 2023-27, which proposed that some NFTs may be treated as “collectibles” under IRC §408(m), subject to the 28% maximum capital gains rate instead of the standard 20%.

The proposed analysis uses a “look-through” test. If the NFT’s associated rights were collectibles (artwork, gems, antiques), the NFT would be a collectible. Digital art PFP? Probably a collectible. Concert ticket NFT? Probably not.

For most clients, NFT activity is limited. Clients minting and flipping NFTs at volume in 2021–2022 may need amended returns. Schedule C treatment may apply if the activity rises to a trade or business.

State Tax Treatment of Cryptocurrency for CPAs

Don’t assume state treatment mirrors federal. California taxes capital gains as ordinary income – see CPA Pilot’s California tax planning guide for a state-specific framework. New York similarly taxes crypto gains at ordinary rates; see the New York tax planning guide for the PTE and residency angles that often affect crypto-active clients.

States with no income tax (Texas, Florida, Wyoming) are non-issues on the gain side. For clients who moved mid-year, check the nexus and sourcing rules. CPA Pilot’s state and multistate tax planning guide covers residency changes and multi-state allocation frameworks that apply directly to these situations.

How to Reconstruct Crypto Cost Basis When Client Records are Incomplete

This happens constantly. The client has wallets on four exchanges, a hardware wallet, and a MetaMask with DeFi activity they “didn’t think was taxable.” Here’s the triage process:

- Pull transaction histories from every exchange — CSV exports from Coinbase, Kraken, etc.

- Connect on-chain wallets to an aggregator tool — Koinly and CoinTracker both support MetaMask/Ethereum address imports.

- Identify missing cost basis — any transferred-in assets where the original purchase data isn’t in the exchange records.

- Reconstruct basis from blockchain records — Etherscan or similar block explorers can show purchase dates and amounts, cross-referenced with historical price data.

- Document the assumptions — if the basis is estimated, note it. “Cost basis estimated from CoinMarketCap historical data for transaction hash 0x…” is better than nothing.

- Consider a disclosure statement — if the records are genuinely incomplete, attaching a statement to the return explaining the methodology protects the client (and the preparer) if the IRS questions the positions.

Note: Revenue Procedure 2024-28 provides transitional guidance for allocating unused basis across digital asset wallets as of January 1, 2025. Review this before reconstructing the basis for clients with assets spanning multiple wallets and pre-2025 purchase history.

For the research-heavy pieces of this work, AI Tax Assistant like CPA Pilot can save significant time – surfacing IRS notices, revenue rulings, and citable authority in minutes rather than hours.

If you receive IRS correspondence related to unreported crypto, see CPA Pilot’s IRS notice response guide for a structured response workflow.

DeFi Broker Reporting in 2026 – The Current State

The DeFi broker reporting landscape changed significantly in 2025. Here’s the accurate picture for practitioners:

In December 2024, the IRS issued final regulations (TD 10021) that would have required DeFi front-end service providers to file Form 1099-DA for transactions beginning January 1, 2027.

However, Congress acted quickly. On April 10, 2025, President Trump signed H.J. Res. 25 (Public Law 119-5), using the Congressional Review Act to repeal TD 10021 entirely. The IRS formally removed the rule from the Code of Federal Regulations effective July 11, 2025. Under the CRA, the rule is treated as if it never took effect, and the IRS cannot issue substantially similar regulations without new congressional authorization.

What this means in practice:

- DeFi front-ends such as Uniswap are not required to collect KYC data or issue Form 1099-DA.

- Centralized custodial exchanges (Coinbase, Kraken, Gemini) remain fully subject to broker reporting under TD 10000 — that rule was not affected by the repeal.

- There is currently no operative DeFi reporting framework. The IRS retains other enforcement tools — audits, John Doe summonses, and blockchain analytics.

The client advice stays the same: Keep records regardless of reporting requirements, because the underlying tax obligations on DeFi transactions haven’t changed. The repeal eliminates third-party reporting; it doesn’t eliminate the taxpayer’s own reporting duty.

Turn Crypto Tax Complexity Into Advisory Value

Cryptocurrency tax reporting is no longer a niche service; it’s a growing line item on nearly every high-income client’s return. With Form 1099-DA live for 2025, the IRS has the matching infrastructure it needs, and clients with unreported activity, missing basis, or untracked DeFi yield are exposed in ways they weren’t two years ago.

The practitioners who get ahead of this will own it as a service line. The ones who don’t will spend 2027 cleaning up amended returns.

The technical layer is manageable once you know the framework. The harder part is the client conversation – getting them to track lots before they sell, treat staking income as income, and stop treating wallet transfers as a black box. That conversation starts with you having the right answers fast.

Stop spending hours digging through IRS notices, Rev. Ruls., and fragmented guidance across TD 10000, Rev. Rul. 2023-14, and Notice 2024-57. Start delivering confident, defensible advice in minutes.

Try CPA Pilot Today and discover how AI-powered tax research is transforming crypto workflows for CPAs:

- Instant IRC and Reg citations for staking income (Rev. Rul. 2023-14), cost basis methods (Reg. §1.1012-1(c)), NFT collectibles (IRC §408(m)), and DeFi dispositions (IRC §1001)

- Pre-built research memos on crypto-specific tax provisions — no more starting from scratch on every novel fact pattern

- Smart workflows that cut research time by 50%+, so you spend less time in IRS notice archives and more time in front of clients

- Confidence at your fingertips with authoritative, up-to-date guidance that stands up to IRS scrutiny

Join thousands of forward-thinking CPAs already using CPA Pilot to navigate digital asset complexity, reconstruct missing basis, and turn crypto questions into premium advisory engagements. Book a 30-Minute Demo to see how CPA Pilot can help you.

Common Queries About Cryptocurrency Tax Reporting

Is a Crypto-to-Crypto Exchange Taxable in the United States?

Yes. Every crypto-to-crypto swap is a taxable disposition under IRC §1001. You recognize gain or loss equal to the fair market value received minus your cost basis in the asset given up, regardless of whether fiat was involved.

Do Crypto Losses Offset Capital Gains on a Tax Return?

Yes. Crypto losses offset capital gains dollar-for-dollar. Short-term losses offset short-term gains first, then long-term. Unlike stocks, crypto has no wash sale rule under current law — so loss harvesting remains available. However, this does not apply to crypto held via securities such as certain ETFs, where IRC §1091 may apply. Legislation to extend the wash sale rule to digital assets has been repeatedly proposed; monitor for changes before advising aggressive harvesting strategies.

How Does the IRS Know if You Do Not Report Cryptocurrency?

The IRS matches Form 1099-DA proceeds against filed returns, issues John Doe summonses to exchanges, and uses blockchain analytics firms to trace wallet activity. The Form 1040 digital assets question also creates a perjury exposure if answered incorrectly.

Are Crypto Gifts and Inheritance Taxable Events?

Gifting crypto is not a taxable event for the donor below the annual exclusion ($19,000 for 2025). The recipient inherits the donor’s basis. Inherited crypto receives a stepped-up basis at the date of death under IRC §1014, eliminating unrealized gain.

What Happens to Crypto Cost Basis After a Hard Fork or Airdrop?

Under Rev. Rul. 2019-24, airdropped tokens from a hard fork are ordinary income at FMV when the taxpayer gains dominion and control. That FMV becomes the taxpayer’s cost basis in the new tokens for future disposition purposes.