![Washington B&O Tax: Classification, Rates & Filing Guide [2026 Edition]](https://www.cpapilot.com/blog/wp-content/uploads/2026/05/Washington-BO-Tax-.png)

Illinois Tax Planning in 2026: PTE Elections, SALT Changes & State Tax Adjustments

[Last Updated on 2 hours ago]

In 2026, Illinois presents unique tax planning challenges for CPAs that cannot be tackled with a general understanding of federal returns. CPAs in Illinois face state‑specific adjustments that can materially impact clients’ tax liabilities, especially around bonus depreciation, pass‑through entity (PTE) elections, grocery tax changes, and replacement tax calculations.

TL;DR – 2026 Illinois Tax Planning

- Illinois tax planning in 2026 requires CPAs to model state-specific adjustments, not just federal tax results.

- Illinois bonus depreciation rules may require addbacks on Form IL-4562 and Schedule M.

- Illinois PTE elections can reduce owner-level federal taxable income, but CPAs must model the benefit under new SALT cap rules.

- The 2026 grocery tax elimination creates new sales tax compliance issues for retail clients.

- Illinois replacement tax affects S corps, C corps, partnerships, and trusts, so it should be included in effective tax rate modeling.

- Residency changes require strong documentation, especially for part-year residents and former Illinois residents.

- CPAs should review depreciation, PTE elections, sales tax setup, replacement tax, and Schedule NR issues before year-end planning.

From bonus depreciation addbacks to PTE elections, Illinois requires specialized attention well beyond a typical federal compliance workflow.

As tax professionals work to optimize tax savings, understanding these intricate state‑level adjustments is critical to maintaining compliance, maximizing after‑tax cash flow, and avoiding malpractice exposure.

This blog explores the key differences between federal and Illinois tax planning, with a focus on high‑impact adjustments that can trip up even seasoned professionals.

For more background on how federal rules intersect with state rules, you can also review our guide on federal vs state tax differences.

Table of Contents

- Illinois Bonus Depreciation Addback: How CPAs Should Plan for Schedule M

- Illinois PTE Election: Who Should Elect and How CPAs Should Model the Benefit

- Illinois Grocery Tax Elimination in 2026: CPA Planning Steps for Retail Clients

- Illinois Replacement Tax: A Hidden Cost for Illinois S‑Corps and C‑Corps

- Illinois Residency Rules: Part-Year, Nonresident, and Former Resident Tax Planning

- Illinois Tax Planning Checklist for CPAs in 2026

- How CPA Pilot Supports Illinois Tax Planning Workflows?

- Illinois Tax Planning FAQs

Illinois Bonus Depreciation Addback: How CPAs Should Plan for Schedule M

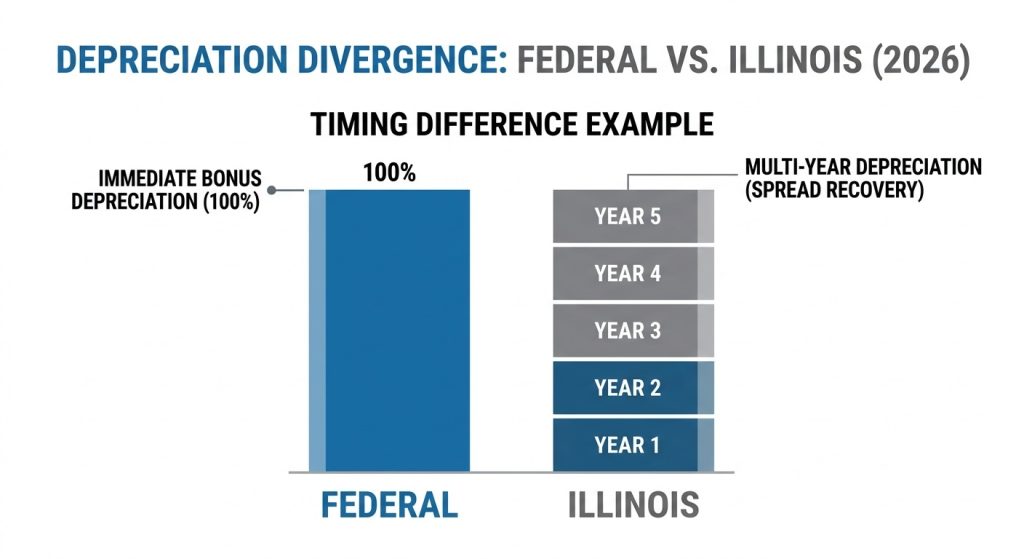

The Illinois state tax code differs significantly from federal regulations when it comes to bonus depreciation. Illinois has long decoupled from federal bonus depreciation under IRC §168(k), and that divergence becomes even more important after the One Big Beautiful Bill Act (OBBBA), which permanently restored 100% federal bonus depreciation for qualified property acquired and placed in service after January 19, 2025.

To prevent that expanded federal benefit from flowing through to Illinois, recent legislation causes Illinois to decouple not only from §168(k) but also from the new federal bonus depreciation for qualified production property under IRC §168(n) for tax years beginning on or after January 1, 2026, as detailed in IDOR’s Informational Bulletin FY 2026.

For 2026 planning, this means Illinois taxpayers often must add back bonus depreciation claimed at the federal level and instead claim a slower, Illinois‑allowed depreciation deduction over the asset’s life.

The addback is calculated on Form IL‑4562, Special Depreciation, which reverses the effects of bonus depreciation claimed under §168(k) and, prospectively, §168(n), and then flows through to Schedule M (Other Additions and Subtractions) or the applicable line on corporate and pass‑through returns.

This adjustment is a timing difference rather than a permanent disallowance: Illinois denies the immediate 100% write‑off but allows depreciation over time, affecting cash flow and estimated tax planning in the early years of an asset’s life.

CPAs should carefully reconcile federal and Illinois depreciation for each fixed asset schedule and clearly explain to clients why their Illinois taxable income may be higher even when the federal return reflects full bonus depreciation.

For more on how IRS rules tie into state planning and controversy, see our article on how IRS regulations affect tax planning and notice responses.

Understanding bonus depreciation is just the start. Another key area where Illinois tax law diverges from federal regulations is in the election of the Pass‑Through Entity (PTE) tax.

Illinois PTE Election: Who Should Elect and How CPAs Should Model the Benefit

The Illinois PTE tax was enacted on August 27, 2021, and is available for tax years ending on or after December 31, 2021. It is authorized under 35 ILCS 5/201(p) and allows eligible pass-through entities (such as S corporations and partnerships) to pay Illinois income tax at the entity level, providing a practical workaround to federal SALT deduction limitations on itemized deductions.

Originally, Illinois’ PTE tax regime was scheduled to sunset for tax years beginning on or after January 1, 2026. That changed on December 12, 2025, when Governor Pritzker signed SB 1911, which removed the sunset provision and made the Illinois PTE election permanent. This is a critical development for 2026 planning: CPAs can now model the PTE election as an ongoing tool in their Illinois SALT strategy rather than a short‑term workaround.

How OBBBA’s Higher SALT Cap Changes the Landscape

The OBBBA significantly changes the SALT cap environment. Beginning in tax year 2025, the federal SALT deduction cap increases from $10,000 to $40,000 for joint filers (from $5,000 to $20,000 for separate filers), and then rises by 1% per year from 2026 through 2029, before reverting to the original $10,000 level in 2030, as set out in the OBBBA’s SALT deduction provisions.

The enhanced deduction is also subject to a phase‑down for higher‑income taxpayers: beginning at about $250,000 of MAGI for single filers and $500,000 for joint filers in 2025, with those thresholds indexed upward by 1% annually through 2029 (roughly $252,500 / $505,000 for 2026), and a 30% reduction in the enhanced benefit for each dollar of MAGI above the threshold, as explained in Anchin’s analysis of the SALT deduction cap under OBBBA: impact on high earners and PTET.

In 2026, many clients will therefore be operating under a SALT cap of approximately $40,400 for joint filers, not $10,000.

For some owners, especially those below or only slightly above the phase‑down thresholds, the enlarged SALT deduction may reduce the incremental benefit of routing Illinois tax payments through a PTE election, because they can now deduct a much larger portion of their SALT directly on Schedule A.

However, this does not make PTE elections obsolete. For taxpayers with very high income who are fully or largely phased down, or those with substantial multi‑state SALT exposure, the effective SALT benefit can still be constrained, and a PTE election can continue to produce significant federal tax savings.

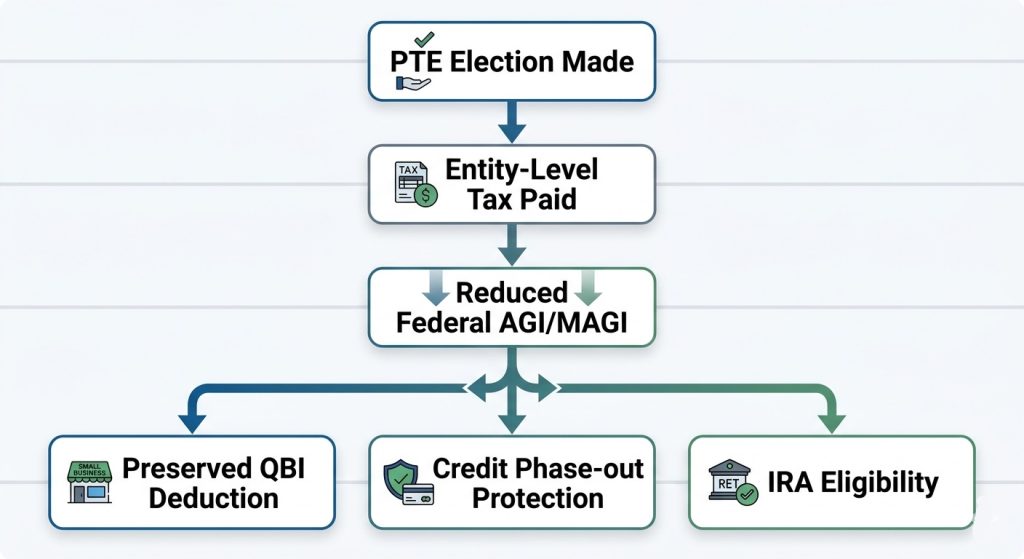

How Illinois PTE Elections Reduce AGI and MAGI

Critically, the PTE election’s benefits go beyond the SALT cap itself. Because the Illinois PTE tax is paid at the entity level and is generally deductible as a business expense, it reduces the entity’s pass‑through income and thus the owners’ AGI and MAGI. Lower AGI/MAGI can:

- Improve eligibility for or increase the QBI deduction in some fact patterns.

- Help preserve itemized deductions that phase out at higher income levels.

- Affect IRA/Roth IRA contribution eligibility, certain credit phaseouts, and limitations on medical expense deductions, miscellaneous itemized deductions, and passive loss allowances.

These AGI‑related effects persist even when a taxpayer’s SALT deduction is no longer strictly constrained by the pre‑OBBBA $10,000 cap, which is why many taxpayers who have historically benefited from Illinois’ PTE regime should still expect to benefit from elections in 2026–2029 and should generally continue modeling.

Mechanically, when a qualified entity makes the PTE election, it pays Illinois income tax on its own net income at the 4.95% PTE rate, and owners receive a corresponding refundable credit on their Illinois individual returns.

Federally, the entity‑level Illinois tax is typically deductible as an ordinary and necessary business expense, which can reduce owners’ federal taxable income beyond what would be allowed if they paid the tax personally under the OBBBA‑modified SALT cap.

Because of these OBBBA changes and AGI‑related dynamics, owner‑by‑owner modeling is more important than ever.

CPAs should test scenarios with and without the PTE election, taking into account each owner’s federal bracket, SALT cap and phase‑down position, existing SALT usage, multi‑state footprint, and the impact on AGI‑sensitive deductions and credits.

For state guidance, see the Illinois Department of Revenue’s Pass‑Through Entity Tax information.

For a deeper dive refer to our in‑depth guide on State-by-State PTE Tax Elections Guide (2026 Rules & Strategy).

Beyond PTE elections, Illinois also introduced significant changes to its grocery tax in 2026, which will affect retail and grocery clients.

Illinois Grocery Tax Elimination in 2026: CPA Planning Steps for Retail Clients

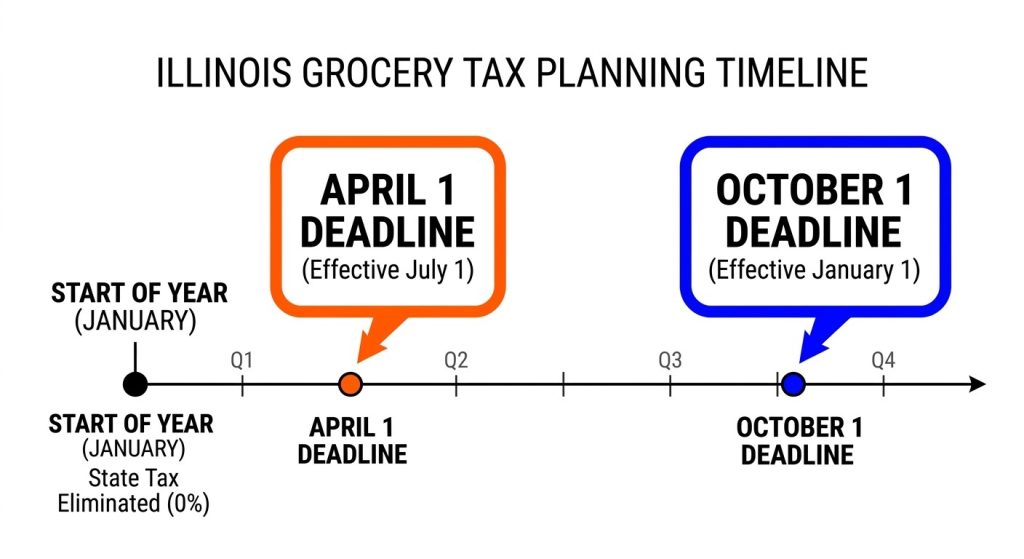

Effective January 1, 2026, Illinois eliminated the 1% state sales and use tax on grocery sales. This change, enacted under Public Act 103‑0781, repeals the state‑level grocery tax and authorizes municipalities and counties to impose their own 1% local grocery tax by ordinance, subject to IDOR filing and approval, as detailed in IDOR’s FY 2026-03 bulletin on Illinois grocery tax changes.

“Groceries” for this purpose retains Illinois’ definition: food for human consumption off the premises, excluding alcoholic beverages, soft drinks, candy, food prepared for immediate consumption, and cannabis‑infused products. Notably, existing grocery‑related taxes in certain RTA and MED locations remain in effect and are not repealed by the state’s 1% elimination.

For CPAs advising local governments or retail clients, the ordinance filing deadlines are especially important:

- Ordinances filed with IDOR by October 1 take effect on January 1 of the following year.

- Ordinances filed by April 1 take effect on July 1 of the same year.

These timing rules are spelled out in IDOR’s FY 2026-11 bulletin on municipal and county grocery occupation tax changes. for ordinances to take effect January 1, 2026, the municipality or county must have filed by October 1, 2025, and the ordinance must be approved by IDOR; after that date, ordinances filed by April 1 take effect July 1 of the same year.

For retail clients, this creates significant compliance and configuration challenges. Mixed-inventory retailers—such as convenience stores, pharmacies, and multi-department grocers—face these issues. They must ensure their POS systems and tax tables are updated.

These updates help correctly distinguish groceries from non-groceries. They also ensure the right combination of taxes is applied. This includes local grocery taxes, RTA/MED taxes, and general sales tax. These taxes may vary by jurisdiction as ordinances are adopted over time.

CPAs should coordinate with clients’ sales tax providers and technology teams to test transactions and verify that Form ST‑1 reporting reflects the new grocery‑specific lines IDOR has introduced.

For a broader sales tax strategy, including ecommerce clients who may face multiple states’ regimes, you can review our article on managing state sales tax and ecommerce tax planning with AI.

With the grocery tax changes affecting retailers, it’s equally important not to overlook the Illinois replacement tax, which can be another hidden but significant cost for business clients.

Illinois Replacement Tax: A Hidden Cost for Illinois S‑Corps and C‑Corps

The Illinois personal property replacement tax is imposed on the net income of corporations, S corporations, partnerships, and certain trusts and replaces the corporate personal property tax that was abolished in 1970. While it often appears as just another line item on a notice of assessment, for CPAs, it represents a key component of the overall state‑level effective tax rate.

As of 2026, IDOR’s Personal Property Replacement Tax guidance states that:

- Corporations pay a 2.5% replacement tax on their net Illinois income.

- Partnerships, S corporations, and trusts pay a 1.5% replacement tax on their net Illinois income.

- Public utilities pay a 0.8% tax on invested capital.

These rates are set by statute and do not fluctuate with economic conditions; what fluctuates is the total statewide replacement tax collections and distributions to local governments, which depend on taxpayer profits and the broader economy.

From a planning perspective, the replacement tax interacts with both federal and Illinois base calculations.

CPAs should ensure that income adjustments made at the federal level, such as bonus depreciation addbacks, Section 199A considerations, or PTE elections are correctly reflected in Illinois taxable income, since those same adjustments can change the replacement tax base as well.

When advising clients on entity choice (e.g., S‑Corp vs C‑Corp vs LLC taxed as a partnership), the replacement tax should be part of the total effective rate modeling rather than an afterthought.

Finally, let’s cover some key considerations regarding Illinois residency rules, which can affect your clients’ tax filings when they move or transition between states.

Illinois Residency Rules: Part-Year, Nonresident, and Former Resident Tax Planning

Illinois has specific rules and guidance for residents, part‑year residents, and nonresidents, and these classifications can have a major impact on how much income is taxed by the state.

IDOR applies a facts‑and‑circumstances approach, looking at where a taxpayer maintains their primary home, where their spouse and dependents live, voter registration, driver’s license, school enrollment, and other objective indicators of residency.

Taxpayers who move out of Illinois during the year must be prepared for closer scrutiny, especially if they continue to maintain ties such as property, business interests, or Illinois‑issued documents. If a client fails to adequately document their move, for example, by not updating their driver’s license, voter registration, or change‑of‑address records, IDOR may still treat them as an Illinois resident for tax purposes and assess additional tax, penalties, and interest.

CPAs should encourage clients to proactively assemble a “residency file” when they move. Copies of leases or closing documents, employment contracts, school registration records, and evidence of severed ties to Illinois.

This not only supports accurate filing as a part‑year resident or nonresident but also provides a strong defense if IDOR questions the taxpayer’s status in a future audit.

For technical, taxpayer‑facing guidance on part‑year and nonresident computations, CPAs should rely on the Schedule NR instructions and Publication 119, Illinois Schedule NR for Individuals, which explains how to complete Schedule NR, Nonresident and Part‑Year Resident Computation of Illinois Tax, and clarifies filing rules for part‑year and nonresident taxpayers.

In situations involving military families, IDOR’s Publication 102, Illinois Filing Requirements for Military Personnel, offers additional, specialized residency and filing guidance.

Illinois Tax Planning Checklist for CPAs in 2026

As 2026 approaches, Illinois tax planning should not be left to last‑minute return preparation. CPAs should incorporate these issues into mid‑year and year‑end planning meetings, especially for higher‑value business and individual clients.

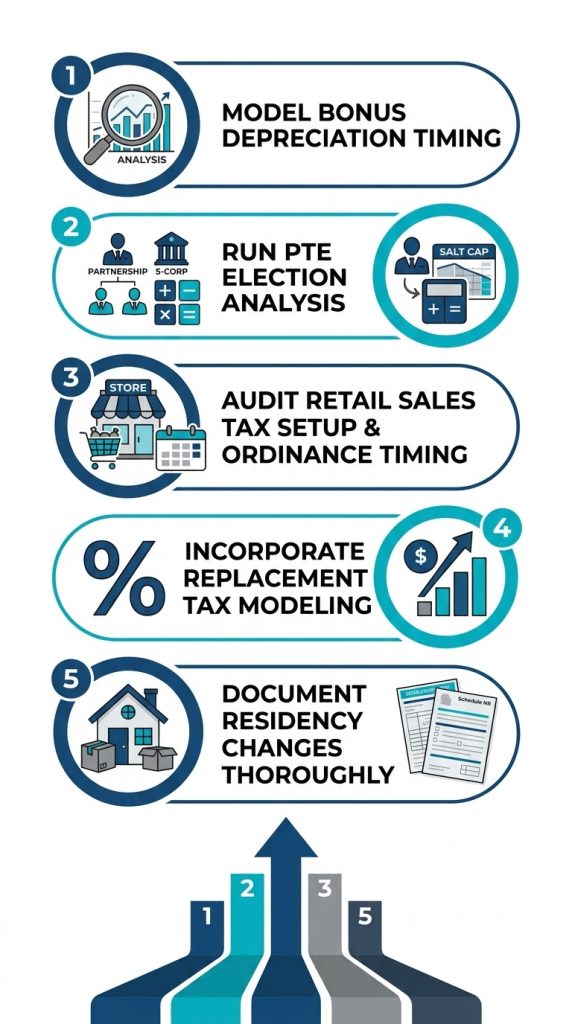

Here are the key steps to prioritize:

- Model the bonus depreciation timing impact

- Run PTE election analysis in the new SALT environment

- Audit retail clients’ sales tax setup and ordinance timing

- Incorporate replacement tax into effective rate modeling

- Document residency changes thoroughly using Schedule NR guidance

Executing all five of these steps well across multiple clients, entities, and owners means moving quickly between federal and Illinois authorities, modeling competing scenarios, and documenting your reasoning clearly. That’s where the right research workflow makes the difference.

How CPA Pilot Supports Illinois Tax Planning Workflows?

Stop spending hours moving between IDOR bulletins, IRC sections, Form IL‑4562 instructions, SB 1911 guidance, OBBBA SALT cap analysis, and Schedule NR publications. Start giving clients clearer planning memos, faster research summaries, and better-documented entity-level comparisons.

Try CPA Pilot today and see how AI‑powered tax research can support an Illinois tax planning workflow for CPAs:

- Instant IRC and IDOR guidance support for §168(k), §168(n), §199A, 35 ILCS 5/201(p), and personal property replacement tax analysis

- Research‑ready summaries that help CPAs connect bonus depreciation addbacks, PTE election mechanics, and replacement tax base interactions across one client’s Illinois return

- Client explanation drafts for PTE election decisions, SALT cap phase‑down modeling, grocery tax compliance changes, and residency documentation steps

- Planning‑note support for documenting why a PTE election, depreciation timing difference, or entity structure choice needs deeper analysis in the OBBBA environment

- Faster research workflows that help tax teams spend less time searching IDOR bulletins and more time advising clients on high‑impact Illinois-specific adjustments

CPA Pilot does not replace CPA judgment. It helps practitioners move faster, organize authority, and explain complex Illinois state tax issues with more confidence.

Book a 30-minute demo today and see the difference!!!

Illinois Tax Planning FAQs

How should CPAs choose between an Illinois PTE election and estimated tax payments?

CPAs compare the Illinois PTE election with owner-level estimated tax payments by modeling federal deductions, Illinois credits, SALT limits, and owner cash flow. The entity pays tax, and owners claim credits.

Does Illinois conform to federal Section 179 expensing in 2026?

Illinois generally allows federal Section 179 deductions but decouples from bonus depreciation. CPAs should separate Section 179 expense from bonus depreciation addbacks on the Illinois Schedule M and Form IL-4562.

How does an Illinois PTE election affect multi-state business owners?

An Illinois PTE election affects multi-state owners by changing state credit use, income sourcing, and federal deduction timing. CPAs should model resident credits, nonresident withholding, and other state PTET rules.

What records should CPAs keep for Illinois bonus depreciation addbacks?

CPAs should keep federal depreciation schedules, Illinois Form IL-4562 workpapers, acquisition dates, placed-in-service dates, and prior-year subtraction records to support addbacks and future recovery deductions.

When should Illinois tax planning start for 2026 business clients?

Illinois tax planning should start before major asset purchases, PTE election deadlines, owner distributions, and year-end estimates. CPAs should model Illinois adjustments by mid-year and update projections before Q4 payments.

Disclaimer: This article is provided by CPA Pilot for educational purposes. While we may offer tax software/services, the information here is general and may not address your specific facts and circumstances. It does not constitute individual tax, legal, or accounting advice. U.S. federal and State Tax laws change frequently; please consult a qualified tax professional before acting on any information.