![Florida Tax Planning – Residency, IRS & Multi-State Risk [2026 Guide]](https://www.cpapilot.com/blog/wp-content/uploads/2026/02/Florida-Tax-Planning.png)

State-by-State PTE Tax Elections Guide (2026 Rules & Strategy)

[Last Updated on 12 hours ago]

Are you prepared for the complexities of Pass-Through Entity (PTE) tax elections across multiple states?

With more than 30 states implementing PTE tax elections, tax professionals must navigate an increasingly complicated landscape of state-specific rules, deadlines, and credit structures.

As the SALT deduction cap continues to affect high-income earners, PTE elections have become an essential tool for tax planning.

TL;DR: State PTE Tax Elections by State (2026 Quick Summary)

- State PTE tax elections allow S corporations, partnerships, and certain LLCs to pay state income tax at the entity level.

- The structure helps business owners bypass the $10,000 SALT deduction cap under IRS Notice 2020-75.

- Over 30 states now offer elective PTE regimes, but rules, deadlines, and credit mechanics vary by state.

- Resident owners typically receive a state tax credit, while nonresident owners face allocation and double-tax considerations.

- Multi-state businesses must evaluate nexus exposure, apportionment rules, tiered entities, and composite return interactions.

- Some states require annual elections and estimated payments, while others impose irrevocable election rules.

- PTE elections do not always produce a net benefit—credit usability, refundability, and owner residency mix determine value.

- AI-powered tools like CPA Pilot help CPAs automate state-by-state PTE research, deadline tracking, and credit modeling to reduce compliance risk and improve tax planning accuracy.

These elections allow business owners to bypass the SALT cap by electing to pay taxes at the entity level instead of at the owner level. However, each state has different rules on how and when to elect, which can create a maze of complexities for CPAs.

In 2026, understanding state-by-state PTE elections is critical for ensuring compliance and maximizing tax-saving opportunities.

AI Tax Tools like CPA Pilot simplify this process by automating tax research, monitoring deadlines, and generating state-specific reports. By leveraging AI, tax professionals can stay on top of changing regulations and ensure optimal tax outcomes for their clients.

Whether you’re managing multi-state clients or handling intricate S-corp or partnership structures, CPA Pilot helps tax professionals streamline PTE elections, saving both time and effort.

Without any further ado, let’s explore the State by State PTE tax elections in detail:

Table of Contents

- What is a Pass-Through Entity (PTE) Tax Election?

- States That Allow PTE Tax Elections in 2026 (Complete Breakdown)

- State PTE Election Deadlines and Filing Requirements

- How State PTE Tax Credits Work for Business Owners?

- Multi-State PTE Election Complications and Compliance Risks

- Strategic PTE Election Planning for CPAs and Tax Advisors

- How CPAs Can Maximize Tax Savings with State PTE Elections?

- PTE Tax Elections FAQ

What is a Pass-Through Entity (PTE) Tax Election?

A Pass-Through Entity (PTE) tax election allows certain business structures, such as S corporations and partnerships, to elect to pay taxes at the business entity level rather than pass the tax liability through to individual owners.

This provision became a vital strategy for business owners following the introduction of the SALT deduction cap, which limits the amount of state and local taxes that can be deducted on federal returns.

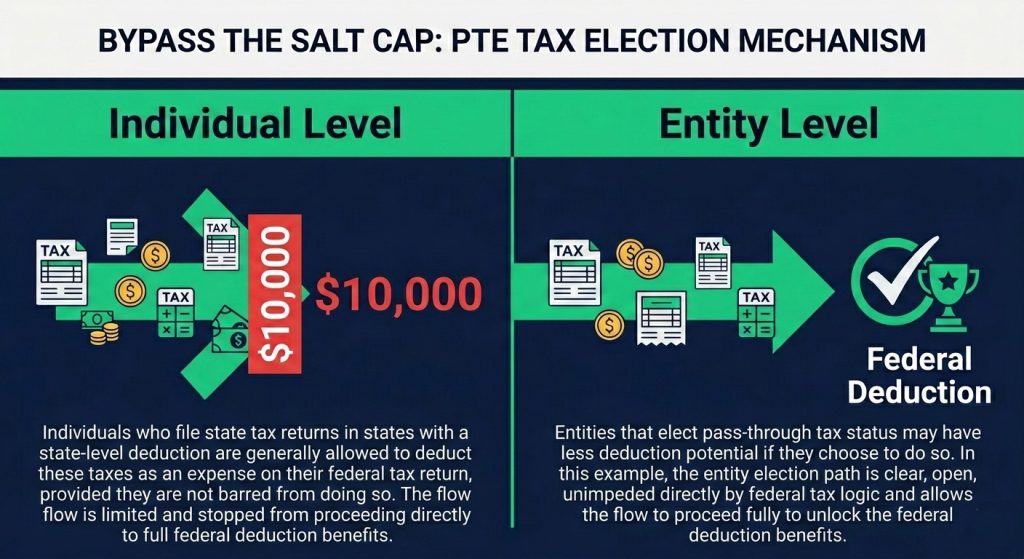

By electing PTE status, businesses pay taxes directly to the state, and the owners receive credits for these taxes on their personal returns. This allows business owners in high-tax states to effectively bypass the SALT cap and reduce their taxable income on their federal returns.

How the $10,000 SALT Cap Triggered State PTE Workarounds?

The SALT deduction cap was introduced as part of the Tax Cuts and Jobs Act (TCJA), limiting state and local tax deductions to just $10,000 for individual taxpayers.

This severely impacted residents of high-tax states, such as California, New York, and New Jersey, who traditionally relied on these deductions to lower their federal tax liability.

To counter this, states began introducing the PTE tax election as a way for businesses to make tax payments at the entity level, effectively allowing owners to bypass the SALT cap.

How does a PTE Election Change Federal Deduction and State Credit Treatment?

When a business elects to pay taxes at the entity level, the owners benefit by receiving a state tax credit on their individual tax returns.

This allows them to bypass the SALT cap and claim higher deductions than they would under normal tax rules.

The PTE election essentially shifts the tax liability from the owners to the business, benefiting both the business and the owners through federal tax savings.

Eligible Entities for State PTE Elections (S Corps, Partnerships, LLCs)

Eligible entities for the PTE election include:

- S Corporations: These entities can elect to have their taxes paid at the entity level, benefiting shareholders through the credit.

- Partnerships: Like S-corporations, partnerships can elect PTE status, providing the same benefits to their partners.

- LLCs Taxed as Partnerships: LLCs taxed as partnerships can also choose the PTE election.

- Tiered Entities: Multi-layered entities can also apply the PTE election at the top tier, allowing tax benefits to flow down to lower-level owners.

For complete information on these entities, read our guide on “S Corp vs C Corp vs LLC”

Now that we’ve clarified what a PTE tax election is and how it benefits business owners, it’s important to explore which states have implemented this provision

States That Allow PTE Tax Elections in 2026 (Complete Breakdown)

As of 2026, over 35 states plus New York City have enacted elective PTE taxes, giving pass-through owners in many jurisdictions a practical workaround to the SALT deduction cap.

While the SALT cap imposed by the Tax Cuts and Jobs Act of 2017 limits individual taxpayers’ ability to deduct state and local taxes on their federal returns, these PTE regimes allow qualifying entities to pay tax at the entity level and pass an owner‑level credit or exclusion through to the individual owners.

However, each jurisdiction has its own eligibility rules, credit mechanics, and election timing, so CPAs must evaluate PTE elections on a state‑by‑state basis.

Let’s break down which states have active PTE tax election regimes and which states have alternative strategies or do not offer PTE elections.

States With Active Elective PTE Tax Regimes

These states allow businesses to elect the PTE tax status and pay taxes at the entity level, providing significant tax benefits to owners, especially those in high-income brackets.

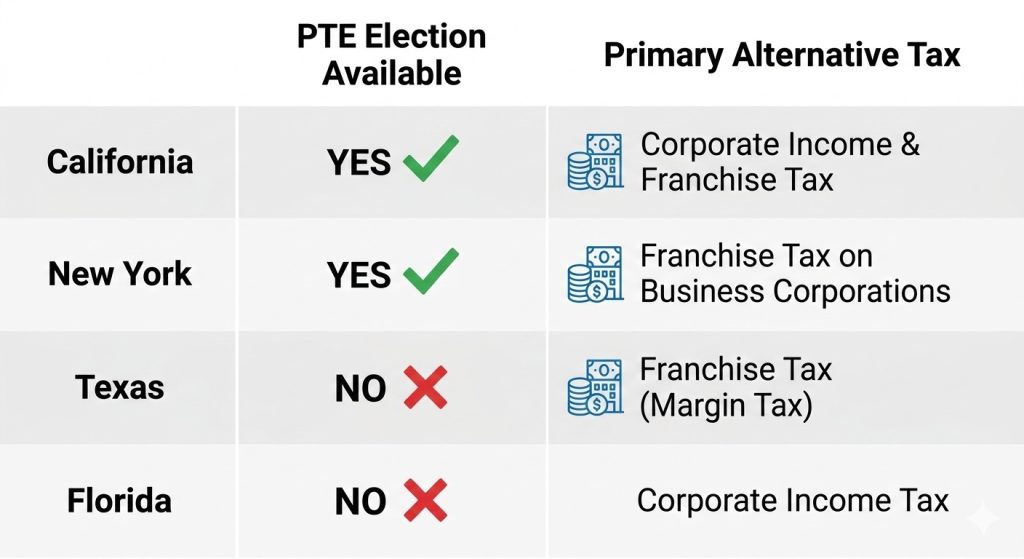

- California PTE Tax Election: California Tax Policy offers an elective PTE tax for qualifying S corporations, partnerships, and LLCs taxed as partnerships, allowing the entity to pay tax at the entity level and pass a credit through to its owners.

The election is made on a timely-filed original return (including extensions), and for years through 2025, a prepayment of at least 50% of the prior‑year PTE tax or 1,000 dollars (whichever is greater) must be made by June 15 of the election year to secure the election. - New York PTE Tax Election: New York Taxation allows certain S corporations and partnerships to elect PTE tax on eligible income, with a separate regime for New York City.

For calendar‑year taxpayers, the state election is made online between January 1 and March 15 of the tax year, and businesses must then follow the Department of Taxation and Finance procedures for estimated payments and return filing.

- New Jersey PTE Tax Election: New Jersey’s Business Alternative Income Tax (BAIT) is an elective entity‑level tax available to qualifying S corporations, partnerships, and LLCs taxed as partnerships.

For calendar‑year entities, the election is made separately on electronic Form PTE‑100 by March 15 for calendar‑year filers after the close of the tax year, and it is binding for that year but must be renewed annually.

- Illinois PTE Tax Election: Illinois allows qualifying pass-through entities to elect entity‑level tax; the election is made on a timely-filed return, including extensions, rather than by a fixed March 15 standalone election date.

For calendar‑year filers, this means the election can generally be made by the standard or extended due date of the PTE return. - Michigan PTE Tax Election: Michigan offers an elective PTE tax for eligible entities, with the election tied to a timely filed return and associated payment requirements.

Current guidance provides that an election coupled with the required payment by the applicable due date (generally in March for calendar‑year filers) remains effective for a multi‑year period unless revoked under state rules. - Georgia PTE Tax Election: Georgia permits certain S corporations and partnerships to make an annual, irrevocable election to pay income tax at the entity level for that tax year.

The election is generally made on a timely filed return (including extensions), and once made for a year, it cannot be changed for that year.

These states have well‑established PTE regimes and can offer meaningful tax savings, but the actual benefit depends on owner residency, income mix, and each state’s credit and carry-forward rules.

States Without Individual Income Tax and Alternative Business Tax Structures

Some states, like Texas, do not have a personal income tax and therefore do not offer PTE elections. Instead, these states may focus on alternative tax structures, such as franchise taxes.

- Texas: Texas does not impose a personal income tax on individuals, so there is no PTE election regime tied to personal income tax. Pass-through entities instead face the Texas franchise (margin) tax, with most calendar‑year filers’ franchise reports and payments due around May 15 each year.

- Florida: Florida Tax Compliance does not impose a broad personal income tax on individuals and therefore does not offer a SALT‑cap‑driven PTE election, although businesses may still face corporate income or other state‑level taxes depending on their structure.

- Washington: Similar to Texas and Florida, Washington does not impose a personal income tax, and as a result, does not have a PTE election available. However, certain entities may be subject to excise or business‑and‑occupation (B&O) taxes that are not addressed through PTE elections.

While these states don’t offer PTE elections, businesses operating in them must still navigate the state’s alternative tax structures.

States With SALT‑Linked or Time‑Limited PTE Elections

Some states tie their PTE regimes to the federal SALT cap or make their elections expressly annual, which creates a practical “time‑limited” environment even if no hard statutory sunset date exists.

- Connecticut: Connecticut converted its PTE tax from mandatory to elective and requires entities that choose PTE status to elect it annually with their state return and follow the Department of Revenue Services payment rules.

The elective regime can be modified by future legislation, so tax advisors should confirm current‑year rules before advising clients.

In addition, several states limit their PTE elections to tax years in which the federal SALT cap is in effect, which currently points to tax years ending on or before December 31, 2026, absent further federal changes.

Tax professionals and business owners need to stay updated with any state-specific legislation or changes that may impact the availability of these elections.

Now, let’s explore the state-wise PTE election deadlines.

State PTE Election Deadlines and Filing Requirements

Navigating PTE election deadlines across states is critical for CPAs who are managing multi-state tax clients.

The deadlines for making a PTE election and filing required documents vary by state, and failure to meet these deadlines can lead to missed tax-saving opportunities or penalties.

Each state’s rules for PTE elections can differ, with some requiring annual elections, while others may have fixed or irrevocable election deadlines.

Let’s break down the key deadlines and filing requirements for PTE elections in major states, and highlight what tax professionals need to know.

Annual vs Irrevocable Elections

Understanding whether a PTE election is annual or irrevocable is essential for planning. States with annual elections allow businesses to reevaluate their decision every year, whereas states with irrevocable elections require businesses to make a final, binding decision for the tax year.

- Annual Elections: Some states allow businesses to make PTE elections annually. This flexibility means businesses can review their eligibility and decide whether the election is beneficial for them every year. Annual elections usually have fixed deadlines, often around the start of the calendar year.

- Irrevocable Elections: In some states, once a business makes a PTE election, it cannot change that decision for the tax year. These elections are binding and should be carefully considered, as they cannot be undone or modified during the year.

Estimated Payment Requirements

For many states, making a PTE election isn’t just about filing the election form by the deadline. Some states also require estimated payments for businesses that elect PTE status. These estimated payments are typically due quarterly and are an important part of the PTE election process.

- Quarterly Estimated Payments: If the state requires estimated payments, businesses must stay on top of each quarter’s deadlines to avoid underpayment penalties.

This is especially important for businesses that may be in high-tax states with large tax liabilities.

CPA Pilot helps tax professionals stay on top of PTE election deadlines by automating the tracking of deadlines for each state. By using AI to track the various deadlines and requirements for PTE elections, CPAs can focus more on client strategy and less on administrative tasks.

Filing Forms and Administrative Mechanics

Each state has its own set of required forms and administrative procedures for making a PTE election. Businesses must submit the appropriate forms to the state’s tax authority, and may also need to provide additional documentation to verify their eligibility.

- Required Forms: Businesses must ensure they file the correct forms with the relevant state agency to make their PTE election valid.

- In California, businesses must file Form 100S to make a PTE election by March 15th.

- In New York, eligible S corporations and partnerships must make the PTE election online through the New York Department of Taxation and Finance portal during the annual election window (January 1–March 15 for calendar‑year filers), and then file the required PTE tax return and owner‑level schedules

Failure to submit the correct IRS forms or provide the required documentation results in a missed tax-saving benefit and election rejection.

Now that we have covered the essential deadlines and filing mechanics for PTE elections, the next step is understanding how PTE tax credits work for business owners.

How State PTE Tax Credits Work for Business Owners?

Once a PTE election is made, business owners can receive significant tax benefits through PTE tax credits. These credits are designed to reduce the tax burden at the individual level by allowing owners to claim credits for taxes paid at the entity level.

Here’s how these credits work for both resident and non-resident owners, and the impact on federal tax returns.

Resident Owner Credit Treatment

For resident owners, the PTE tax credit allows them to offset their state tax liability by applying the credits for taxes paid at the entity level. The credit can be used to reduce their individual state tax liability, and depending on the state’s laws, it may be refundable or nonrefundable.

- Credit Against Individual Tax: The credit helps owners reduce their state income tax liability. This is particularly beneficial in high-tax states like California or New York, where state taxes can significantly impact personal returns.

- Refundable vs Nonrefundable: Some states offer refundable credits, where the owner can receive a refund if the credit exceeds their state tax liability. Others provide nonrefundable credits, where the credit can only reduce the tax liability to zero, and any excess is lost.

- Credit Limitations: States may place limitations on the amount of credit that can be claimed, either by setting a maximum dollar amount or by limiting the credit to a percentage of the taxes paid at the entity level.

All-in-all, resident owners can apply the PTE tax credit to reduce their personal state tax liability, with variations in refundability across states.

Nonresident Owner Credit Interaction

For nonresident owners, the PTE tax credit is applied differently, as they may be subject to tax in both the state where the business is located and their state of residence.

- Other State Tax Credit Conflicts: Nonresident owners who live in another state and own a business in a state that has a PTE election may be able to claim tax credits for taxes paid to the business’s home state. However, they may face conflicts if their home state also provides similar credits.

- Double-Tax Risk: Nonresident owners risk double taxation if both the home state and the business’s state tax the income. Some states offer reciprocity agreements to avoid this, but others may require nonresident owners to pay tax in both jurisdictions.

- Allocation Distortions: Nonresident owners must ensure that their credit claims are properly allocated between their states of residence and the business’s home state. Incorrect allocations can lead to tax discrepancies or missed credits.

Nonresident owners face potential conflicts and double taxation if their home state also provides a similar credit, requiring careful allocation between states.

Credit Carryforwards and Limitations by State

Each state has its own rules for carrying forward PTE tax credits. In some states, unused credits can be carried forward to offset future tax liabilities, while others may have expiration rules.

- Carryforward Duration: States typically allow business owners to carry unused credits forward for a set number of years. For example, some states may allow credits to be carried forward for three years, while others may allow indefinite carryforwards.

- Credit Expiration Rules: States may also have rules regarding the expiration of credits. If an owner doesn’t use the credit in the allowable carry-forward period, the credit may expire, and the business owner will lose the opportunity to claim it.

- Interaction with Federal QBI Deduction: The Qualified Business Income (QBI) deduction may interact with PTE credits, potentially reducing the amount of credit available.

For instance, if the business owner is already claiming the QBI deduction on their federal tax return, it could affect the state credit calculation.

Each state has different rules for carrying forward unused PTE tax credits, with some allowing credits to be carried forward for a set period while others may expire after a certain number of years.

Now that we’ve covered the intricacies of how PTE tax credits work for both resident and nonresident owners, it’s important to explore the complications that arise when dealing with multi-state PTE elections.

Multi-State PTE Election Complications and Compliance Risks

Managing PTE elections across multiple states introduces complexities, as each state has its own PTE election rules.

Businesses operating in more than one state must navigate the differing state tax rates, credit allocations, and filing requirements to ensure compliance and tax optimization.

Understanding these complications is essential for CPAs working with multi-state businesses to ensure the PTE election is applied correctly.

Multi-State Partnerships With Nexus Exposure

When a business has nexus in multiple states, the PTE election can become more complex. Each state may have different rules for how PTE elections apply to businesses operating in more than one jurisdiction.

CPAs need to evaluate whether making a PTE election in one state will affect the tax obligations in another state.

- Nexus Challenges: Businesses must file separate PTE elections in each state where they have nexus. This can lead to additional paperwork and administrative work.

- Tax Rate Variations: Different states have different tax rates and credit structures, meaning the PTE election can affect the business’s overall tax bill unevenly.

- Apportionment Pitfalls: Businesses must allocate their income and taxes across states to ensure they’re not overpaying or underpaying taxes.

Tiered Entity PTE Elections and Credit Flow Complexity

Tiered entities are business structures that involve multiple layers of entities, such as a parent LLC that owns an S-Corp or a partnership.

Making the PTE election in such structures requires careful consideration, as the decision about which level of the entity elects PTE status affects tax credits and liabilities.

- Upper vs. Lower Tier Elections: The choice of whether to make the PTE election at the parent or lower-tier level can affect how tax credits flow through the entity structure.

The parent-level election may allow credits to pass more easily, while lower-tier elections can complicate credit allocation. - Credit Flow Issues: Businesses must ensure that PTE credits flow correctly through the tiers to the individual owners, which can be challenging in multi-layered entities.

- Filing Complexity: Tiered entities often require additional forms and calculations to ensure the PTE election is properly applied, adding complexity to the filing process.

PTE Election vs Composite Return: Strategic Comparison

Some states allow businesses to file composite returns, which combine the income of multiple owners into a single return, simplifying the filing process for nonresident owners. However, the PTE election might provide more tax-saving opportunities in certain situations.

- Composite Returns: A composite return allows businesses to file a single return on behalf of nonresident owners, simplifying tax filing. However, composite returns may not provide the same tax-saving opportunities as a PTE election.

- PTE Election Benefits: The PTE election allows businesses to claim credits for taxes paid at the entity level, potentially offering more tax savings than composite returns, which may not be as beneficial to taxpayers.

As managing multi-state PTE elections can be complex, using AI-powered tax assistants like CPA Pilot can help automate the process of analyzing state-specific rules, deadlines, and credit structures.

By automating research and tracking deadlines, CPA Pilot helps tax professionals and businesses manage multi-state clients with ease and accuracy.

Strategic PTE Election Planning for CPAs and Tax Advisors

When deciding whether to make a PTE election, CPAs must carefully evaluate various factors that can impact both the business and its individual owners.

While the PTE election offers clear tax-saving benefits, it’s not the right choice for every business.

In this section, we’ll discuss when it makes sense to elect PTE status and the factors tax professionals need to consider to optimize the election for their clients.

High-Income Owners in High-Tax States and SALT Cap Modeling

The PTE election is especially beneficial for high-income owners in high-tax states, where the SALT cap restricts individual tax deductions.

- Federal Deduction Benefit Modeling: For high-income earners, the PTE election allows state taxes paid at the entity level to be deducted on their federal returns, helping to reduce their taxable income.

- SALT Cap Bypass Impact: The PTE election allows owners to bypass the $10,000 SALT cap, ensuring they can claim state tax deductions without being limited by federal rules.

PTE election provides high-income owners in high-tax states with significant federal tax savings by bypassing the SALT cap.

When a State PTE Election Does Not Produce a Net Tax Benefit?

While the PTE election offers many advantages, it may not be the best choice in certain scenarios.

- Low State Tax Liability: If the state tax liability is relatively low, the PTE election may not provide enough benefits to justify the election.

- Multi-State Credit Limitations: For businesses operating in multiple states, some states may limit or disallow the credits, diminishing the potential tax savings of the election.

- Refundability Constraints: In some states, the credit may be nonrefundable, meaning that if the credit exceeds the state tax liability, it cannot be refunded, making it less beneficial for some owners.

The PTE election may not be advantageous for businesses with low state tax liability, multi-state credit limitations, or nonrefundable credits.

Key Variables Before Making a State PTE Election Decision

Before recommending the PTE election, Tax Advisors should assess several critical factors that influence the overall tax benefit.

- Owner Residency Mix: Consider owners’ residency, as the tax impact can vary depending on whether owners reside in high-tax or low-tax states.

- Income Level Thresholds: High-income owners benefit more from the PTE election due to the higher tax liability, while low-income owners may not see significant savings.

- Credit Usability: Evaluate the usability of credits across states, as some offer refundable credits, while others may only offer nonrefundable credits, which can affect overall savings.

- Estimated Payment Requirements: Some states require estimated payments as part of the PTE election, which must be accounted for when evaluating the total tax burden and administrative work.

Tax professionals should evaluate owner residency, income thresholds, credit usability, and estimated payments before deciding on a PTE election.

How CPAs Can Maximize Tax Savings with State PTE Elections?

PTE elections are essential for navigating the SALT cap and optimizing tax savings for business owners, especially those in high-tax states.

By understanding the ins and outs of PTE election deadlines, credit mechanics, and state-specific rules in today’s complex tax environment, CPAs can help their clients save significantly.

CPA Pilot offers a powerful AI-driven tax Platform to automate tax research, track deadlines, and ensure compliance across multiple states, helping you focus on strategic planning and client success. Start leveraging AI today to streamline your PTE election processes and unlock maximum tax savings for your clients.

Book a 30-minute demo today and see the difference!!!

PTE Tax Elections FAQ

What are the benefits of making a PTE election for high-income business owners?

A PTE election allows high-income business owners to bypass the SALT cap by paying state taxes at the entity level, enabling larger federal tax deductions. This strategy helps reduce overall tax liability and optimizes state tax credits for owners.

How do multi-state businesses handle PTE elections in different states?

Multi-state businesses must file PTE elections in each state where they have nexus. Different states may have varying rules, deadlines, and credit structures. Careful apportionment and estimated payment planning are necessary to comply across jurisdictions.

What impact does the PTE election have on federal tax returns?

The PTE election allows businesses to pay taxes at the entity level, enabling owners to claim state tax credits on their federal tax returns. This helps reduce taxable income, bypass the SALT cap, and maximize federal deductions for business owners.

Can LLCs elect PTE tax status and claim tax credits?

Yes, LLCs taxed as partnerships can elect PTE tax status, allowing owners to benefit from state tax credits. The business must file with each state’s tax authority and ensure all requirements are met for proper PTE election compliance.

How do states with no income tax handle PTE elections?

States with no income tax don’t offer PTE elections. However, these states may still require franchise taxes or other business taxes. Businesses in these states may elect PTE status in other states where they conduct operations, ensuring compliance.